- CFO Secrets

- Posts

- 👀 Year One Update On My Small Business Acquisition

Accountants, what’s your love language?

For us, it’s acts of service. Helpful actions that save you time and make your life easier.

❄️ Like when your thermostat automatically adjusts before you get home.

🚽 Or when the public toilet automatically flushes itself (preferably after you’ve finished).

Now imagine if your monthly journal entries could be prepared and posted automatically. All that messy transaction data from your PSPs, transformed into beautiful, balanced, accurate journal entries. And automatically posted to your ERP.

Are we speaking your love language yet?

See how Leapfin helps you create reliable journal entries automatically.

The playbook

“You need to meet Lucas.”

“OK, but who’s Lucas?” I asked.

Gerry (a retired finance recruiter and long-time friend) responded: “He’s like you, but he’s not like you. You guys talk in the same way, about the same things. Except he’s older and owns a ton of businesses, and you don’t. So he must know something you don’t.”

Interesting. But it was what he said next that really got my attention:

“He’s bought businesses with $500m of annual revenue, but he’s never put a single penny of his own capital at risk. He’s a master acquisition entrepreneur.”

I Googled Lucas. But found nothing except a LinkedIn profile. He had started in one of the big accountancy practices 25 years before. Then he fell off the map. For the last twenty years, he’d described himself as the ‘director’ of an equally mysterious company. No website, nothing. Now I was intrigued.

I met him a few months later, and it was worth the wait.

He’d told me he’d set himself a challenge twenty years ago: build a portfolio of businesses with $1bn+ of revenue without putting a single dime of his money at risk. So far, he’d reached just over $500m (about 20 deals), and hadn’t yet put any money in. One deal was for a business of $150m in revenue. It blew my mind he could do something of this size without his own capital.

He estimated he would hit $1bn in less than 3 years.

I asked him why, even now, he was still buying businesses with zero money down. When he could clearly afford to make some bigger bets and grow more quickly.

His answer made me laugh: “It started out of necessity. I didn’t have any capital. But soon it became a challenge. Just because I can use my money, doesn’t mean I should.”

It reminded me of the Dr. Malcolm quote from Jurassic Park…

Source: Giphy

It was then I realized I’d asked the wrong question. I corrected my error:

“How are you buying such large businesses with no money down?”

“I don’t need money, I have mastered the art of deal structuring. Nearly every deal I look at would require my capital. I pass on those and wait for those that don’t. Sometimes I wait years for one.”

He went on to explain how he would use his relationships with banks (particularly the work out teams), to identify opportunities.

He was looking for:

An owner of the business who wanted out. So much so that they would wait a long time for their money, or even hand over the keys for nothing.

Businesses with unencumbered assets (plant, equipment, or accounts receivable in particular)

Turnaround situations. Either declining cashflow or a cash burn that he could arrest quickly

He would then build a deal structure where he would create a bunch of cash from the balance sheet:

Using asset-backed lending to leverage plant and equipment, receivables, and inventory

Renegotiate terms with lenders, often resulting in a haircut.

Make day 1 ‘subtraction’ style turnaround changes to the business to improve cashflow immediately (we covered these in the recent M&A series)

He’d then offer some of that ‘day one’ cash to the owner, plus a seller note over a long period of time. Sometimes 5-10 years. In exchange, he’d take some cash and 70-100% of the shares of the business.

So think hyper-aggressive LBO combined with balance sheet restructuring and seller note.

“Don’t the owners just tell you to f*ck off?”

Lucas smiled: “Yes of course. Nearly every time. But every now and then they don’t. Or they even pick up the phone years later. One deal came 8 years after I first pitched it. It’s a numbers game. I think of it like a sales job.”

This guy was buying net assets for cents on the dollar, on deferred payment terms, and renegotiating the whole balance sheet so aggressively that the business was paying HIM to take it.

He must have built at least $100m of net worth using this playbook.

No wonder he was smiling.

Get your brand in front of 30,000+ finance leaders

Advertise in the CFO Secrets newsletter to get in front of tens of thousands of finance leaders and business decision-makers.

This is a special edition update on my small business acquisition one year on.

Year One Update On My Small Business Acquisition

Meeting Lucas was an eye-opener.

It was at that moment I discovered the term ‘acquisition entrepreneur.’

I had to try some of these $0 down deals for myself. Just as a side project.

My friend and I have done a couple of acquisitions together since. Small deals to start with, to test the model. And if we could buy profitable businesses with $0, buying them with our capital would only make it easier.

One of these ‘tester’ deals closed last March, and I broke it down in one of my first newsletters a few days later.

That was my most popular post ever. People went mad for it. I have had hundreds of emails, and even more DMs, since asking for an update. The hard work is always post-deal after all.

Well, today I’ll share that update…

First a recap:

We acquired a niche printing business with $1.5m of revenue and $358k of annual net income.

We paid the owners entirely on a seller note. $20k per month over 30 months (with a six-month payment holiday at the start).

Whilst the income was solid and recurring, sales were in decline. The owners lost all motivation to win new business.

For the full breakdown on the acquisition, read last year’s post first.

The Handover

So, after a four month closing process, we finally had the keys.

The first job was to get control of the business without breaking it.

This was a business that was cash-generative on day one. It was cashflow optimized for its current activity levels, so there were no low hanging fruit quick cashflow wins.

In the short term, there was much more risk than upside:

The owners had been omnipresent for the last 20 years. Ensuring the business didn’t stutter as they moved out would be crucial.

Equally, we had no appetite or time to operate this business ourselves. It would be a terrible use of our time. We had to fill the management gaps on day 1.

We knew we’d find some skeletons in the closet. There are always skeletons. We just didn’t know how much, or what the impact would be.

Our job was to hand it over to new management without getting sucked in ourselves. While also ensuring performance didn’t slip. Balancing act.

This is how we did it.

While the previous owners had been around for 20 years, they were no longer doing much real work.

90% of the day-to-day business was being run by the operations manager, Bobby. An affable young guy that my partner and I had grown to like quickly.

The 10% Bobby didn’t control, was the accounting, pricing and invoicing. That was in the hands of the owners. They didn’t want Bobby to know how much money the business was making.

All of the price and customer admin was run on a horrible network of 20-year-old Excel files and manual pricing cards. It was something only they could navigate. They had refused all of Bobby’s drive to modernize it.

Unhandoverable!

That’s where we came in. We could liberate the owners by digitizing the customer and price master data. Despite it being a small business, it had thousands of products and hundreds of customers. Every combination of product and customer had unique pricing. This was a big task.

In the owner’s mind, they had a life sentence of managing the master data monster they’d created. For us, it was just one big project for some offshored VAs to collapse hundreds of different Excel files into one flat file. But we didn’t tell them that …

Here’s what we did::

Promote Bobby to General Manager - responsible for running the business

Pay increase of 50% - he was ecstatic. Immediate loyalty.

Implement a bonus scheme paid for performance (phantom equity style). He had an incentive to behave like an owner.

Provide coaching and mentoring to Bobby

Put weekly dashboard reporting in place so we could keep a check on performance

Outsource all bookkeeping to a trusted bookkeeper

Implement monthly P&L, balance sheet, and cashflow reporting. Formalize time to review financial performance each month.

Digitize the pricing and product data nightmare, using offshore VAs. And hire a sales administrator to respond to customer orders, raise invoices, etc.

Agree to a deal with one of the previous owners to play an account management role with a couple of key customers

We’d focus on bedding that down for six months, with zero new sales efforts. Minimize the moving parts.

This was our ‘Do No Harm’ phase.

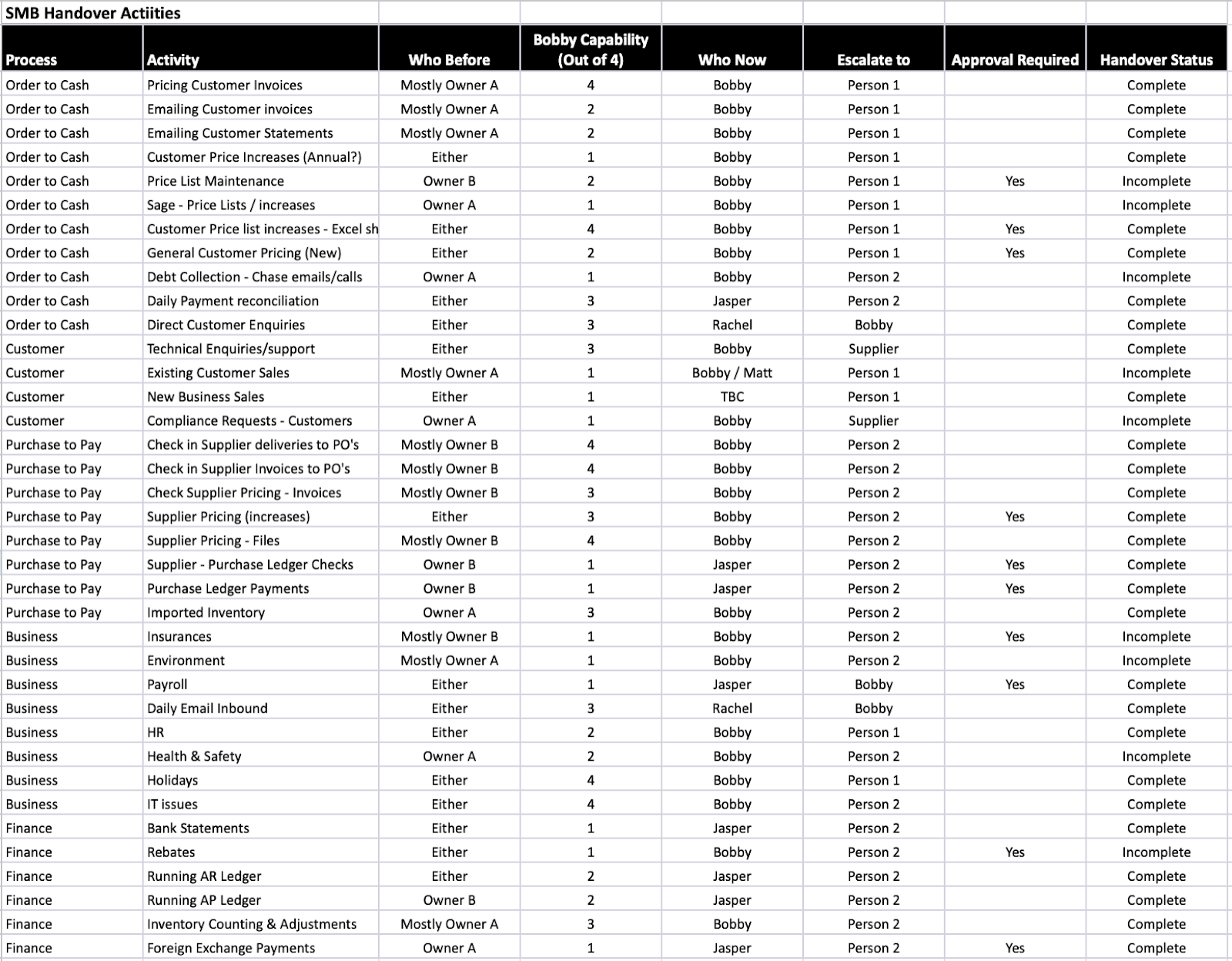

To ensure we didn’t miss anything in the handover we asked the previous owners to make a table that listed:

Every task they undertook

It’s frequency

Which of the two of them undertook the task

Their assessment of Bobby’s current capability at that task (i.e. could he pick it up)

We then mapped each task to a future owner. Most of it was to Bobby, some was to the outsourced bookkeeper, Jasper.

Here is a copy of the actual table we built with the outgoing shareholders (with names changed). This was the status 1 month after closing:

It became the most important document in the business to begin with. As we ensured all handover items were closed off before the owners left permanently 3 months after closing.

First 12 Months Results

Did it work?

We think so.

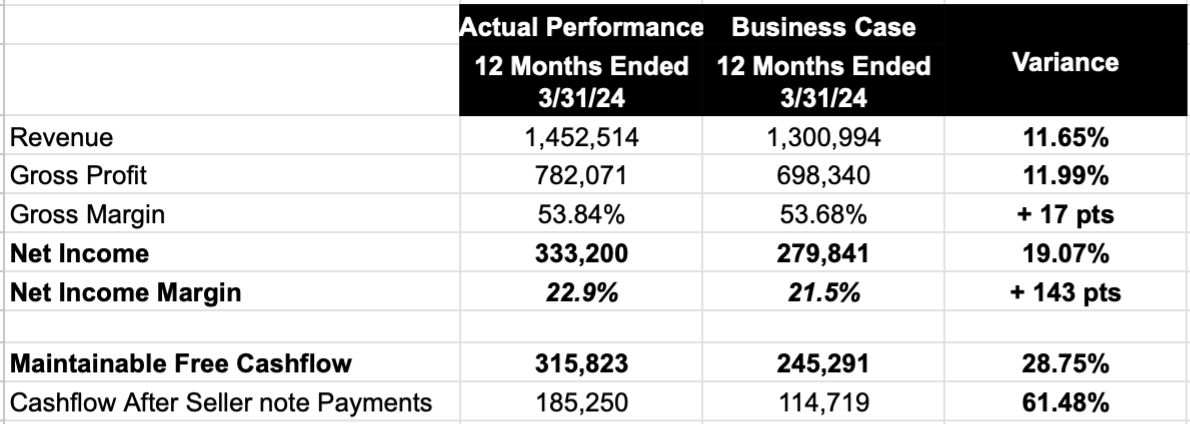

The business delivered $53k more net income than we’d assumed in our business case for the first 12 months:

We generated $316k of cash (vs our expectation of $245k). After we’d paid the seller note we were left with $185k of distributable cashflow.

Not a bad return on a $0 investment.

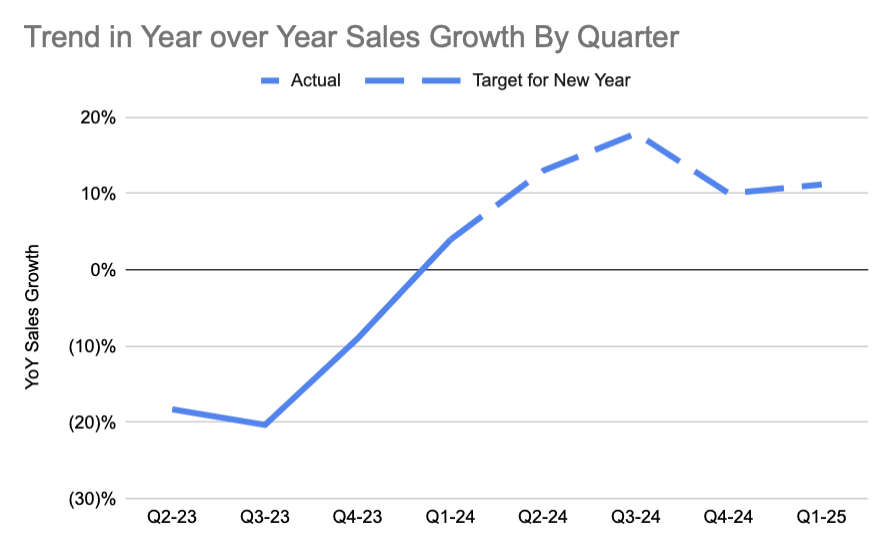

While we beat our sales target by over 11%, this was against a soft target. We had budgeted for a 20% decline. We’d assumed a number of headwinds in year one:

The ‘do no harm’ phase would mean a short-term acceleration of the sales decline in the first six months.

The exiting owners would likely have ‘crammed’ sales into the final few months. This would maximize the cash value of their exit. And it would have a negative rebound effect on sales in our early period. (One of the ‘skeletons’ I mentioned earlier).

We would not actively reduce sales prices to grow sales, until we were confident underlying gross margins were stable.

Our assumptions turned out to be right:

You can see for the first six months sales fell by 20% year over year as we expected. But once we’d come through the handover, we were able to get the business back to growth by 2024 Q1. This sales recovery came sooner than we thought, and is the driver of the extra profit and cashflow.

We are budgeting sales growth of 13% for the next twelve months. But should smash that target. We have just landed a new customer that will grow the business by 30% by the end of the year. Plus many more in the pipeline.

Reflections on the First 12 Months

Here are some things I’ve learned about owning an SMB vs running a corporate:

1) HR diligence is vital

We struck gold with Bobby. Our hunch was right. He was a diamond in the rough. But we could have been wrong, and that would have been a nightmare. He has proven far more indispensable than the previous owners. In the future, we’ll do more HR diligence. More thorough profiling and interviewing of key management before we sign.

2) Small doesn’t mean simple

The admin and master data behind this business was surprisingly complex. Simplifying and digitizing this was a massive unlock. But it was hard work and took a long time. 2x VAs working for nearly 3 months.

3) TBV businesses are my favorite

This business has the quality I call ‘Tiny But Vital’ (TBV). To our customers our products are a very small part of their COGs. Operationally vital, and very tightly specified. It’s a great place to be. A small but critical cog in someone else’s COGS.

4) The basics will always be the basics

For businesses that are not doing weekly KPIs, monthly financials, basic operational control. It’s amazing how much value these processes can add quickly.

What next?

Now for much bigger deals.

My business partner is a friend of mine. He’s great at making friends, and sales. I’m good at operations, finances, and deal structuring.

I’m a long way from the restructuring savage of Lucas, but that’s not where we want to be either.

We want to be putting our capital into deals, but still aggressively structured. The best model for us is in combining the seller note structuring, with our own capital (and banks where appropriate).

Either way, we’ve got the bug and plan to do more, much bigger, deals in the future. We are sector agnostic but will be looking for these qualities in a business:

A hyper-motivated seller who doesn’t mind waiting for their money

A solvable succession issue

Tiny But Vital (TBV) to its customers

Can’t be quickly disrupted by AI or copied by Google for free

Boring businesses we can explain to our kids

Just small enough to be off the radar of mid-market PE, but big enough to be interesting (EBIT $1-5m)

And we are prepared to wait an age - and say no to 1,000 unsuitable deals - to find the right one.

Maybe we’ll even raise a fund one day…

If you are interested in jumping out of corporate life and into SMB ownership, let me know. If you’d like more content on this, please respond to this message and tell me. If you want it, I’ll write it!

|

|

Thomas Jefferson from Virginia, USA asked:

First-time caller, long-time listener.

Currently in b-school without any experience in finance (military background). Seems that every single person has different advice with respect to the best industry to get the strongest foundations of finance to later run a company, be CEO, CFO, etc.

What is your take? Consulting? Investment Banking? ETA?

TJ... You are right. Everyone has a different opinion. And they are all right. And also wrong at the same time. (Including myself). There is no right or wrong, only what is right for you, so take this with a pinch of salt…

If your goal is to ‘run’ a company, then the key is to get into a ‘real’ business in possession of valuable skills as soon as possible.

Professional services are a great place to build finely tuned generalist skills.

So, I would suggest you spend 3 years on a rotation of high repute somewhere in IB, Consulting, Big 4, etc. Precisely where? It doesn’t really matter. These are all fantastic programs. So whatever role and culture suits you best.

It won’t take long (a few years) to build high-class generalist experience working with brilliant people.

Then you need to get yourself into a great company. A real business. In the corp dev, strategy, FP&A, or reporting teams. Go apply those skills you learned, and build business leadership expertise. Make sure you are working in a great team, getting a feel for what good looks like in the real world.

Get those first steps right, and you’ll be rolling downhill from there on.

If you would like to submit a question, please fill out this form.

Work with Secret CFO

And Finally

If you asked for a copy of my turnaround checklist, following last week’s post, look out for an email over the next few days for how you can access that.

Next week we get into our May series; Building a winning finance team.

If you enjoyed today’s content, don’t forget to check out this week’s sponsor Leapfin.

Stay crispy,

The Secret CFO

Disclaimer: I am not your accountant, tax advisor, lawyer, CFO, director, or friend. Well, maybe I’m your friend, but I am not any of those other things. Everything I publish represents my opinions only, not advice. Running the finances for a company is serious business, and you should take the proper advice you need.

What did you think of this week’s edition? |

Join the conversation