Capital allocators are only as good as the information they depend on. The more robust the information, the better the decision-making. Meet Ledge…

Are your capital allocation decisions driven by days or weeks-old data?

Ledge automates cash reconciliation and journal entry creation, ensuring you have real-time visibility into your cash position, cash flow analysis, and forecasts.

Ledge automates workflows across your banks, payment processors, data warehouses, and other sources – without R&D or IT – and syncs it back to your ERP.

Whether it's for R&D, operations, or liquidity management, make smart capital deployment decisions based on always-updated data with Ledge.

From top-floor strategy to shop-floor reality

“What do you mean, ‘no’?”

It always makes me laugh when people say that. Not sure how I could have made it any clearer.

I gave it a go anyway…

“It means, I won’t be approving this capex project.”

But Nathan (a divisional VP of Operations) wasn’t going to give up on his project easily: “You can’t do that.”

“Ummm, I definitely can do that.”

“Well, Sandy would have approved this. It’s net present value positive, and all of the metrics are green.”

“Sandy’s gone, I’m the CFO now. And the rules for unlocking investment are going to have to change. Your business unit has had over $100m of investment capex over the last three years. All of it was NPV positive on the capex appraisal. Yet, your EBITDA hasn’t moved an inch. Meanwhile, the total business has seen its debt grow and watched its free cash flow evaporate. That might have been green metric performance before I arrived. But it won’t be going forward. We have a crisis, so you are going to have to work much harder in the future to prove your capex projects aren’t total sh*t.”

No response. But he did lose a little color from his face, as he realized the free ride on capex was over.

It’s not generally my style to throw my weight around like this. But I needed this tale to become folklore in the business. I needed to hear the sound of operations teams scampering around the business to properly test their investment cases.

The truth is this wasn’t just a message to the operations team. It wasn’t really their fault.

They were just gaming inside the rules set by finance.

The finance team had completely failed to connect.

Sandy’s strategy had been one of debt reduction, just like mine would be. But that hadn’t made its way into the investment criteria of the business. The operational reality was severed from the strategic intention. As a result, the business has made some really poor capital allocation choices.

While many of the decisions made sense on an individual basis, when you added them up, it was a disaster. Breaching leverage targets, with the business now on the brink of death.

The business had been allowed to bury sins inside NPV assumptions - not least a cost of capital that was criminally low given the current reality.

It was clear what job 1 was going to be: set a new, tighter framework for how this business allocated capital.

And make sure that this was connected from top-floor strategy to shop-floor reality.

And all of the Nathan’s in-between…

Side hustle opportunity: finance advisors wanted

Are you a fractional CFO, or a finance professional interested in picking up part-time advisory work? We're launching a platform to help match you with SMBs looking for exceptional talent.

Apply for our Beta by filling out this short questionnaire.

This is the first week of our series on capital allocation.

Allocating Capital Like a Boss

This is the series you’ve been waiting for: capital allocation.

Capital allocation = what choices a business makes with the cash it has. The first duty of an effective CFO.

This will be a 4 parter running throughout June. But first, let me take you back to the cashflow series.

In week 1 of that series, we defined Maintainable Free Cashflow (MFCF) as cash generated from existing operations. All other cashflows are allocations of capital.

The distinction is important because they merit very different decision-making processes.

MFCF is delivered by sales, operations, and product teams. The people who make and sell real things. It’s typically decentralized.

Starbucks generates $2bn to $3bn of MFCF one $4 cup of coffee at a time. By 400,000 baristas all over the world.

But cashflows ‘below the MFCF line’ are capital allocations. These decisions are made centrally.

The allocation of the $3-$6bn of cash sitting on Starbuck's balance sheet is managed by a handful of execs in Seattle.

The piece on MFCF may be a good primer.

Once you’re caught up on MFCF, let’s talk about l about how you allocate capital. It’s one of the fundamental duties of the CFO.

Capital allocation is about trade-offs::

Buy back shares or buy a competitor?

Invest in capex projects or R&D?

Reduce debt or pay a dividend?

When to play offense and when to play defense?

And an infinite number of other combinations

The CFO must set the rules for those trade-offs. And then must put the controls in place to ensure those rules are followed.

But great CFOs also know when it’s time to break those rules. It’s both art and science.

Capital allocation is classically taught as having five options:

Organic Growth

M&A

Debt Reduction

Dividend Payments

Share Buybacks

There are a bunch of calculations that help you solve for the right answer. That math is important, and we will cover some of it in this series. But corporate capital allocation is not the same as pure investing.

It’s not just math. Corporate capital allocation is a framework that talks to your strategy. And a control and execution system that talks to your framework.

When the math is given precedent over a great framework, things go wrong. As happened in the opening anecdote.

But what about when it is done well?

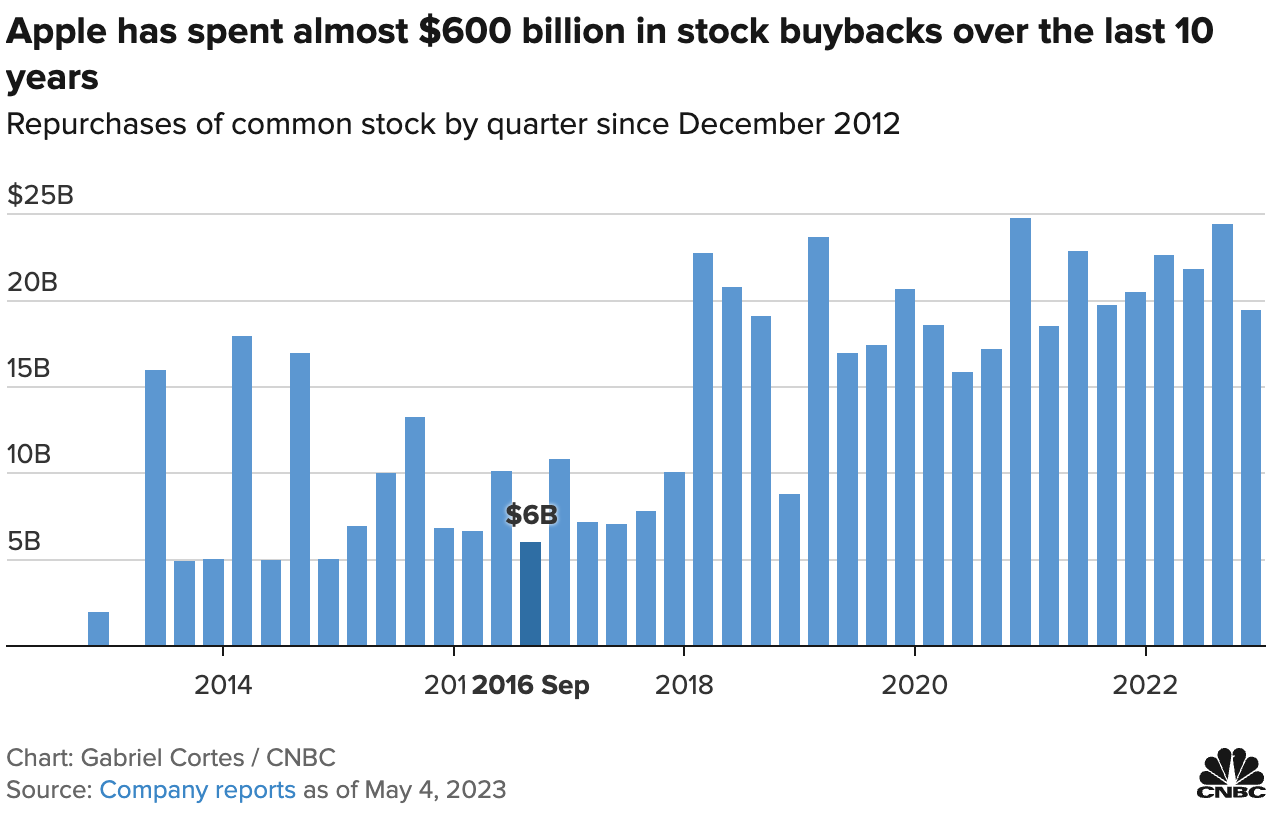

For a masterclass in matching capital allocation to business strategy, look at Apple.

In the early 2000s, Apple spent 8% of revenue on R&D. It aggressively invested in breakthrough technology, doubling down to own the consumer shift towards portable computing.

As a capital allocation decision, this was a punt on improving future MFCF per share.

It worked. The development of the iPod, iPhone & iPad led to an explosion in revenue. And eventually profits and cashflow.

By 2012 R&D spend had diluted to 2% of revenue. By this time, Apple was producing more MFCF than it knew what to do with.

In the absence of anything better, the only option was to return that cash to shareholders. Cue the biggest share repurchase program in corporate history:

Source: CNBC

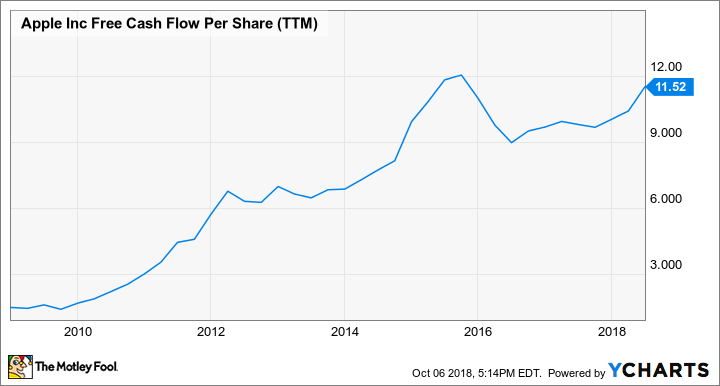

It knew that the most valuable way to use its enormous cash pile for shareholders was to reduce share count. That increased future MFCF per share.

Source: The Motley Fool

Life-changing products and breathtaking marketing are the reasons Apple became the world's first $3tn company.

But, it was supported by a bold capital allocation strategy that matched its business strategy. Hand in glove.

Imagine if Apple hadn’t been bold enough to increase R&D investment in the early 2000s. Maybe they wouldn’t exist today.

Likewise, imagine if Apple had plowed $600b into overpriced acquisitions.

Apple has an interesting challenge ahead. Critics say its buyback program is actually a function of a lack of real innovation. Which is now starting to cost shareholders.

It will be fascinating to watch.

So, how do we connect capital allocation to strategy? Well, we need to get abstract (don’t worry, we’ve got plenty of time to get tactical in this series too).

Why do we allocate capital? What is the objective of effective capital allocation? To maximize the long-term MFCF per share.

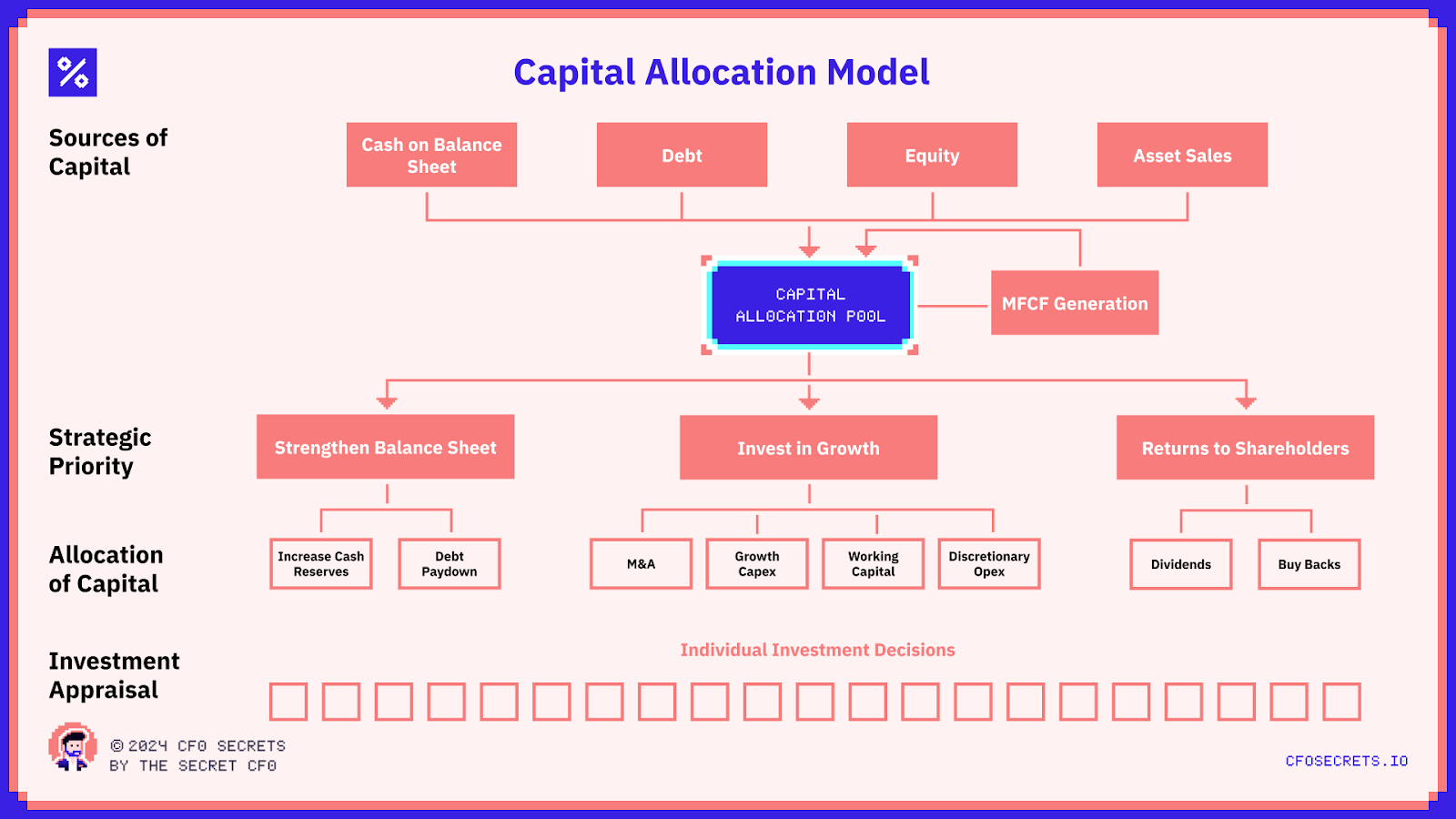

What are the real options for a business to allocate capital?

Despite what the textbooks say, there really are only 3:

Strengthen the balance sheet

Invest in growing the business

Return money to shareholders

The importance of each of these will depend on:

Business strategy

Market conditions

Balance sheet

Risk appetite

The individual capital allocation options sit underneath those strategic objectives as follows:

Capital allocation goes wrong when individual investments are appraised in isolation. There must be a connection to a strategic objective.

Capital allocation is all about relative options. And decisions become 7-dimensional pretty quickly. You need guardrails. Some golden rules to live by, set by the board.

These golden rules sit in something called the Financial Policy.

The Financial Policy is the rule book that governs how you fund your business. And treat your shareholders.

It’s especially valuable in businesses where there are multiple, complex stakeholders.

It provides the framework for making capital structure and balance sheet decisions. Ensuring everyone is working on the same plan.

If you are a Board, you need to have one.

If you are a Shareholder, you should demand your Company has one.

If you are a CFO or CEO, having one will make your job easier.

By setting clear guardrails you can take the emotion out of finance decision-making.

It’s the first vital step in an effective capital allocation framework.

A Financial Policy has 5 Sections:

1. Overall Objective

2. Debt

3. Liquidity

4. Distributions

5. Capital Allocation

1. Overall Objective

Start with what the overall financial objective for the business is.

This will depend on the stage of business and should speak to the financial risk and return appetite.

Some examples for (illustrative purposes only):

Dividend Stock: Deliver total shareholder return of at least a 6% premium to the base rate, with a minimum of 50% of after-tax profits distributed to shareholders.

Turnaround: Reduce debt levels to below $1.2bn and Net Debt Leverage to below 3x EBITDA. Then recommence dividends.

Startup: Maintain a minimum 12-month runway, and grow valuation by min 2x each funding round

PE-Backed: Minimum Net Debt: EBITDA of 4x upon entry, maximizing equity value accretion over 5 years

Prudent Balance Sheet: We never have more than 1.5x EBITDA of debt, and ensure we always have $100m of cash on the balance sheet as a minimum.

2. Debt

This should set the rules around how and when you use debt. And set some limits on how much.

Example Policies:

Long Term Leverage Target is 3x. Maximum leverage tolerance in the short term is 5x, reducing to 4x by 2025.

Refinance debt a minimum of 18 months before its maturity.

Prefer fixed rate debt, but use interest rate swaps to manage rate risk on floating rate debt where there is arbitrage.

For internal metric purposes, treat all off-balance sheet debt as debt.

Metrics that you could include:

Net Debt : EBITDA Leverage (Target, and Limit)

Total Balance Sheet Debt $ Limit

Total Debt (Off & On Balance Sheet)

% of Floating vs Fixed Rate Debt

Average Duration of Debt

Shortest Duration of Debt

Clearer parameters in a financial policy would have prevented some of the heinous capital investment decisions made in the opening anecdote.

3. Liquidity

The rules you set to make sure you don’t run out of money.

Example Policies:

Never hold less than $100m of cash on balance sheet

Set internal liquidity headroom limit at $200m, with a warning level set at $250m

If a 12-month look forward suggests a breach, raise new liquidity from the following sources, in this order: additional working capital facilities, equity, term debt

Metrics:

Cash on Balance Sheet

Total Liquidity Headroom (Cash + Committed Undrawn Facilities)

Forecast Minimum Headroom (12 Months Rolling)

Runway (for Cash Burning Businesses)

Armageddon Survival Buffer: Liquidity Headroom/Avg Daily Sales

4. Distributions

How and when you return money to shareholders.

Some examples:

Distribute a minimum of 50% of after-tax profits

Buyback shares before dividends if the P/E ratio is below X

Metrics:

Dividend % of Earnings

Dividend % of Free Cash Flow

Buyback: Dividend Ratio

5. Capital Allocation

How do you make decisions about where and how to allocate surplus capital? How do you prioritize?

Some examples:

Prioritize capital allocation based on NPV Per $ Capital At Risk ranking by project/options

First exhaust surplus capital on all growth projects with an IRR of greater than X%

Appetite for M&A?

Allocate capital to debt repurchase until Net Debt is below X.

Metrics to use:

Internal Rate of Return (IRR) %

NPV Per $ Capital At Risk

Payback Period

Weighted Average Cost of Capital (WACC)

At its simplest, a financial policy could be just one sentence.

For example, an SMB owner-operator might distribute 100% of after-tax profits as dividends. And never buy any business or take any debt. That's enough.

At its most complex (an F500) it could run to several pages or chapters.

The more diverse the stakeholders, the more complex the Financial Policy will be.

The important thing is to be deliberate about your financial policy.

Agreeing a framework bespoke to your business with all stakeholders.

Then documenting it.

And then living it.

Across the rest of this series we will get into how you do that:

Part 1 (This Week) - Introducing Capital Allocation

Part 2 (Next Week) Investing In Growth

Organic vs M&A

Organic Investment

Capex Investment

Discretionary Opex & R&D

Working Capital

Making Choices

Part 3 - Capital Structure Management

Strengthening Balance Sheet

Cash Holding

Debt Levels

Returns to Shareholders

Dividend Policy

Share Buybacks

Sources of Capital

Part 4 - Putting It Into Practice

Connecting Capital Allocation Decisions to FP&A

Investment Appraisal

Governing Returns

Investment Committee

Keeping Financial Policy Live

But if you can’t wait until next week, and want a little more, here is an interesting piece from BCG on the role finance plays in capital allocation.

See you next week for part 2 in this series on capital allocation.

Investment Appraisal in isolation is useless. Corporate capital allocators must consistently connect strategy to investment decisions

Great capital allocation starts with a robust, board-approved, financial policy.

The business strategy should help prioritize between a) strengthening the balance sheet, b) investing in the business, and c) returning to shareholders

MA from Nairobi, Kenya asked:

As CFO for a billion-dollar company, how do you find the time to produce content with such depth and high level of detail? I’m incredibly curious about the time management system you use (if any), and if that’s something you’d be willing to share for others to learn from.

Lol, I get this question a lot. Some people play golf. Some people dance. Some go fishing. Everyone has their thing.

I write. It’s a hobby. I also travel a lot too. This gives me an opportunity to write when I travel.

Because I am writing purely from experience, it doesn’t require any/much research. So I can write 3,000 words in 4-5 hours.

I now also have a small team to help me tidy it up and make it look and sound beautiful (I’m not so efficient at that). And knowing I have such a loyal and awesome audience gives me all the motivation I need to keep going.

With regards to how I manage my time more broadly. I like prioritized to-do lists. If there is one thing I consider a superpower, it would be my ability to focus on one thing at a time. I don’t believe in multi-tasking, it certainly doesn’t work for me. I’m really good at concentrating all of my energy on the most important thing on my pad at that moment. And I find that focus leads me to better results.

I’m not sure if this helps you or not, but thank you for the question. It’s cool to see my content has made its way to Kenya.

If you would like to submit a question, please fill out this form.

Work with Secret CFO

And Finally

Next week, we are diving into investing in growth.

If you enjoyed today’s content, don’t forget to check out this week’s sponsor Ledge.

Stay crispy,

The Secret CFO

Disclaimer: I am not your accountant, tax advisor, lawyer, CFO, director, or friend. Well, maybe I’m your friend, but I am not any of those other things. Everything I publish represents my opinions only, not advice. Running the finances for a company is serious business, and you should take the proper advice you need.

What did you think of this week’s edition?