Year-end reconciliation does not need to be a nightmare

Ledge automates your cash reconciliation in real-time, offering 24/7 continuous close with multi-way matching. Scale complex, high-volume reconciliation without engineering support – just powerful automation that dramatically cuts time spent on bank reconciliation. Join forward-thinking finance teams that are already using Ledge.

Back to basics

By now, I was furious.

This was my fifth balance sheet review in 48 hours, and the fifth dumpster fire.

What had I inherited?!

I’d been in the CFO seat for a couple of months and still hadn’t been able to get a grip on how the business was performing. Or more importantly… where it was heading.

The cashflow forecast was more than 10% off target most weeks, making it unreliable and unpredictable. The last twelve-month earnings had been so volatile it was impossible to read where the business was.

This wasn't just bad luck. It was clear there was a serious issue with the business's reporting integrity.

When the history tells a clear story, but your forecasts do not, you look at your FP&A team. But when you don’t even understand the recent historical performance, you look at your accounting function.

So that’s what I did. I told the board and CEO that I was suspending all forecasting until I understood the base. The board and exec were making decisions based on forecasts built on sand. It wasn't going to end well.

Budgeting, forecasting, analysis, strategic insight. None of it matters one bit if the sand is shifting beneath your feet.

The board was unhappy and took some convincing, but they came around. I laid out the pattern of missed forecasts, highlighted the risks of decision-making blind spots, and made it clear: I wouldn’t put my name to any forward-looking information until the foundation was solid.

This gave me the breathing room to go where I knew I needed to head for the next few months… the balance sheet.

I decided to review the entire balance sheet (and the reconciliations) myself. It was the only way I could get a handle on the situation.

And five balance sheet reviews in, I was shocked at what I saw. The balance sheet reconciliations were a train wreck. And there was no excuse.

Accrued expenses were huge… 3x bigger than they should be. Why? Slow purchase invoice processing.

Disputed invoice values were enormous. Why? The business didn’t know how to resolve the disputes and clear them down.

Accrued income was building for certain services that had not been invoiced. Why? I can't even answer that one. Just laziness, I guess.

It was a MESS. The list went on.

It was going to be a long road. But I knew exactly where to start: transactional processing.

This business had a disgracefully poor attitude to accounting basics. I needed to get this complex organization back to processing transactions correctly and quickly. And resolving discrepancies properly. Reconciling the balance sheet.

This would mean reducing the number of manual postings, accelerating the close, and improving the reporting (and cash forecasting accuracy).

Time to get to work…

Happy New Year (End)

“Next year, all our troubles will be miles away.” — Frank Sinatra

Most CFOs and their finance teams are running into year-end closing with the taste of gingerbread and peppermint still fresh in their mouths. Trading holiday cheer for the stress of preparing the year-end numbers. That means a few intense weeks of reconciling balance sheets and being audited. But soon enough, it’ll be over.

And when it is, you’ll make promises to yourself (again) that there MUST be an easier way to handle reconciliations. Or prepare the impairment paper. Or finalize the inventory reserve. Or whatever your personal year-end hell is.

Here are 7 New Year-End Resolutions to make closing less stressful:

1) Year-end is just a 'bigger' month-end

The better the month-end close, the easier the year-end.

You should be closing the books to a high standard monthly. It’s amazing how many controllers let issues sit on the balance sheet for 11 months of the year before a December panic to clear it in time for year-end. This is surprisingly common but unacceptable.

Think of every month-end as a mini year-end. Build the habit of transactional precision now, and you'll thank yourself when December rolls around.

If you have 11 great-quality month-end closes, you’re keeping things clean and getting reps in.

The first 70% of your year-end will just feel like another monthly close.

For some industries additional complexities like inventory adjustments or seasonality might require extra attention at the year-end itself. But even then, starting earlier will pay off.

Ask yourself: Are your month-end closes good enough?

2) Start early and plan well

Even for those things that aren’t part of your monthly routine, you don’t have to wait until after the year is through to start working.

Early in Q4 is a great time to agree on the key assumptions behind the riskiest parts of your balance sheet. Like a warranty reserve, a difficult impairment judgment, or a volatile inventory reserve. These all contain sensitive assumptions that shouldn’t wait until year-end to agree on.

This is especially true if you have multiple stakeholders (audit committees, auditors, boards, etc.). Same with the narrative parts of your financial statements (MD&A, significant risks, business overview, etc.)

The tightest closes I’ve seen have all been meticulously planned. A detailed day-by-day plan with actions, and owners, clearly communicated.

Line up that plan with your team and auditors (if applicable), pre-schedule review calls, and close meetings. All of this should happen early in Q4 at the latest, with enough time to shift your plan if you need to.

3) Solve the 3 statements in the right order

Accurate financial reporting depends on prioritizing the three financial statements in the correct sequence.

Focusing solely on the income statement during the close process, and then reconciling balance sheets afterward, often leads to messy balance sheets. This is alarmingly common, especially in fast paced high-pressure, performance-driven environments.

How do you think something like this happens …

On the other hand, focusing exclusively on balance sheet accuracy can result in an income statement that lacks clarity and fails to inform the business. Both approaches are flawed.

You need to solve for and understand all three statements as part of the close itself. And to do so in the right order.

So, what’s the correct order?

Balance Sheet: Prioritize accuracy and resolve issues promptly

Income Statement: Understand performance and variances

Cashflow Statement: Extend your understanding of performance to cashflow

Remember: an income statement is simply a function of the difference between the balance sheet on two dates. And a cashflow statement is a product of the income statement and balance sheet movements.

In short, an accurate balance sheet is the foundation of the close. Your P&L and cashflow have no credibility without it.

4) Be relentless in reconciling better

We saw in the opening anecdote what happens when an accounting team starts to trust its manual accruals more than its transactional accuracy.

Everything breaks down.

There was a time when reconciling in batch was the order, and an over-reliance on manual adjustments was par for the course. But that was when the technology and computing power didn’t exist to handle automating recs with thousands or even millions of lines. Those days are long gone, and you cannot afford to lag behind best practices in reconciliation technology.

This is especially critical if you operate in a business with high volumes of cash transactions, like retail, fintech, e-commerce, or banking. For these industries, even small discrepancies can snowball into major issues, so early identification and resolution of reconciling items is essential.

Even if your business doesn’t deal with high volumes, reconciling items can still reveal valuable insights. Usually, a reconciliation is a sign of something not captured properly at the source. Whether it’s misallocated payments, timing issues, or operational inefficiencies. Treat these exceptions as opportunities to strengthen your processes and reduce recurring issues.

When discrepancies arise, ask yourself: What can I change now to make that reconciliation cleaner next month? Can you accelerate the speed of passing invoices? Or improve the process for resolving discrepancies.

And AI-powered tools are taking this to the next level using LLMs to match transactions, clean data, and resolve discrepancies. And this can be done in real time, taking the load off of the month/year-end.

This is cutting edge right now, but soon it will be table stakes. Get ahead.

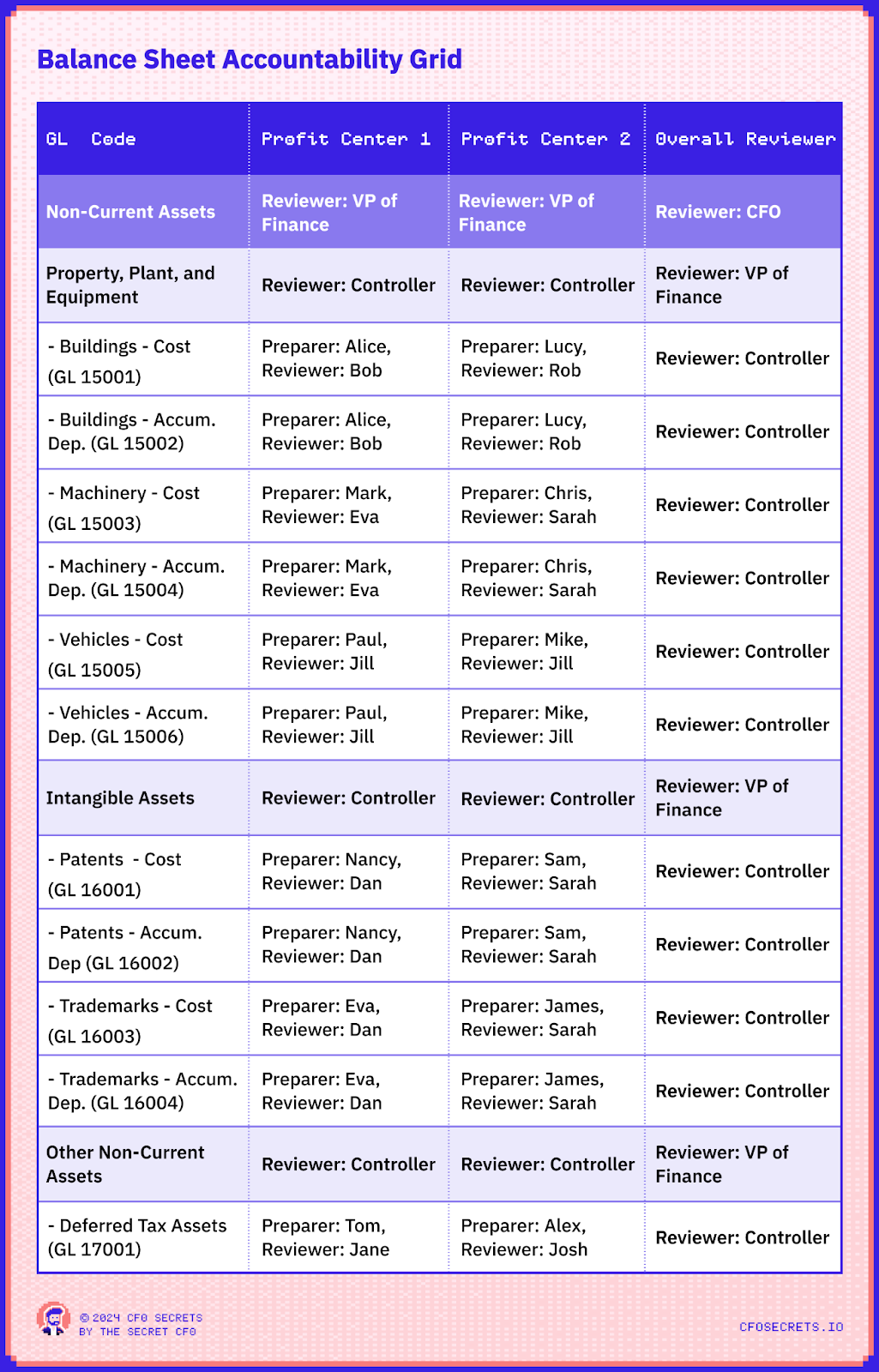

5) Balance sheet accountability grid

It stuns me how often these simple principles are not followed.

Every balance sheet should have ‘four eyes’ assigned to it:

A person responsible for preparing

A person responsible for reviewing

If your business uses the same balance sheet codes across multiple cost centers or locations, you must assign the ‘four eyes’ for every combination of cost center and general ledger code. And ensure it aggregates logically.

Think of it as a grid, where each cell represents a combination, and every cell has two names. One for preparation and one for review. No gaps allowed.

Here is an example extract of the format for keeping track of who has eyes on which part of the balance sheet (in a complex example):

While this would be overkill for a ‘one-man band’ finance team, if you’ve got more than one pair of hands on balance sheet reconciliations, you should prepare one of these grids. It leaves nowhere to hide. Everyone knows their role on the balance sheet.

If this grid is clearly documented, with capable pros in the preparation and review roles, good things will happen in your close process.

It sounds simple, but many don’t do this (often because everyone thinks someone else is doing it).

From my experience, it’s in the space between different people and teams where most balance sheet issues grow. They grow in the dark. Like mold.

6) Build P&L and cashflow bridging into the close process

The numbers mean nothing without context. And the starting point for context is variance analysis.

“Revenue was $x” is not useful.

“Revenue was 5% up on last year but 10% down on budget” is more useful, but still not great.

The value comes from getting to why. What were the drivers of the variances?

Most finance teams don’t get into the variance analysis until after the books are closed. It’s understandable, oftentimes it’s hard enough getting the actuals finalized by the close deadline.

But if you can, at least starting the variance analysis before the books are closed has a ton of benefits:

Brings the accounting and finance teams closer together

Gives the opportunity to identify and tidy up any P&L coding issues

Helps the accounting team better understand the business

Creates a healthy tension in the acceleration of the early part of the close

Accelerates getting quality reporting and analysis out to the business after the month-end

We have a series coming early next year on performance reporting which will get deeper into bridging performance.

7) Make closing cool

Ok, hear me out… actually forget it. Closing will never be cool. BUT, it is important. Everything good in finance is downstream from a great close.

And closes don’t improve by accident. It takes a lot of work to engineer a day out of the timeline. Or to improve automation.

A good controlling team is worth their weight in gold and you, as CFO, need to make sure they get their share of the credit.

Celebrate small steps in the right direction, and build a culture of relentless process improvement. Momentum builds quickly, and the downstream ripple effects of faster, cleaner closing are huge.

Review what went well, and what can improve in scheduled debrief sessions.

Net-net

The foundation of a great close is early preparation, clear ownership, automated reconciliations, and a continuous improvement culture.

By making small improvements each month, you can make enormous progress in twelve months.

Good luck with your 2024 close, but make next year’s even better.

Focus on transaction-level reconciliation and integrity to get the foundation strong

Ensure your whole accounting team is engaged in continuous improvement

Enforce a ‘balance sheet first’ mindset for the close. But build P&L and cashflow variance analysis into the close too if you can

Thirsty for Knowledge from London asked:

I’ve been playing catch-up on your content since discovering you by lucky accident this year, absolutely mind-blowing, eye-opening & overall just damn helpful so my profuse thanks to you for this.

I’d be really interested to understand, given that you’ve opted to nail the turnaround CFO niche, what your trigger(s) is/are that tell you that it’s time to move from one role to the next.

Is it job completed at point X and your motivation for other areas of corporate challenges pales in comparison to the crisis stage of a turnaround cycle for example?

No problem, my thirsty friend, I’m glad you are finding it helpful.

It’s a great question. It’s not easy to know when it’s time to move on from a turnaround. Turnarounds go through multiple phases.

There is the initial CPR phase - that is the stage of deep cuts and debt renegotiation in a fight for survival

Second comes intensive care - this is where the business is brought back to sustainable cash generation

The final stage of turnaround is rehab - this is where the business seeks a return to growth but from a sustainable base

But even once rehab is over, there is another part of the business life cycle to run into. Often the priority shifts to transformation or investment.

Different stages suit different pros. I think I am best used seeing through three stages of turnaround and the early part of the next part of the life cycle.

Likewise, some people really thrive in the chaos of that CPR stage. They tend to work as Chief Restructuring Officers, Interim CFOs, or restructuring pros in the big 4. They know that they are Jedis at restructuring the balance sheet, but probably aren’t the right people to get the business back to growth.

And there are some, that once they’ve been through the turnaround phase become so attached to the story that they want to see it through more parts of the business life cycle.

The truth is, I can feel it in my bones when it’s time to leave. The point at which I will be better doing something else and the business will be better with a fresh CFO.

Thanks for the question.

If you would like to submit a question, please fill out this form.

Work with Secret CFO

If you’re looking to sponsor CFO Secrets Newsletter fill out this form and we’ll be in touch.

Get your side hustle on. We're launching a platform to help match you with SMBs looking for exceptional fractional advisory talent. Apply now

Find amazing accounting talent in places like the Philippines and Latin America in partnership with OnlyExperts (20% off for CFO Secrets readers)

And Finally

Next week we’ll start a new series on financial due diligence.

If you enjoyed today’s content, don’t forget to check out this week’s sponsor Ledge.

Thank you for all of your support in 2024. Big things are coming in 2025 for CFO Secrets (I’ll send you an email on new years eve with more detail).

Stay crispy,

The Secret CFO

Was this email forwarded to you? You can subscribe by clicking the button below:

Disclaimer: I am not your accountant, investment advisor, tax advisor, lawyer, CFO, director, or friend. Well, maybe I’m your friend, but I am not any of those other things. Everything I publish represents my opinions only, not advice. And certainly is not investment advice. Running the finances for a company is serious business, and you should take the proper advice you need.

What did you think of this week’s edition?