Ambitious growth meets smart spending

How do you accelerate growth without losing your grip on spending? The CFO playbook delivers battle-tested strategies to optimize cash flow, assess risk vs. ROI, and scale intelligently in any economic climate. Check it out and discover why smart spending doesn’t have to slow business growth.

Everyone loves a good comeback story

"And now that the reset button has been pushed, the challenge ahead of us is this… do we squander the opportunity in front of us or do we engineer the great comeback story of the post-COVID era? I am here for the comeback story."

It would take something extraordinary to pull Barry McCarthy out of retirement. The legendary tech CFO, who’d taken both Netflix and Spotify public, was now 68. He had earned his right to a quieter ‘portfolio’ life.

But McCarthy was a member of the ‘cult of Peloton’. Hopping on his Peloton bike for a daily Power Zone endurance ride.

And now Peloton was in trouble. The combination of a brand he loved, and a turnaround in his sweet spot (subscription businesses) was enough to lure McCarthy back.

Source: Giphy

Peloton had a meteoric rise under founder John Foley, leading to an IPO in the Fall of 2019.

And that’s when things got crazy…

Along came the pandemic. For many, Peloton’s connected fitness offering became the distraction and gym alternative people were looking for.

Subscriber numbers grew by 5x to 3 million in two years. Analysts upweighted their forecasts. many were expecting subscriber numbers of 10m+ before too long.

Peloton had caught lightning in a bottle, and the stock ripped. From $25 in September 2019 to $160 by Christmas 2020.

There was one problem.

Well… there were a ton of problems. But one really big, obvious one.

Peloton’s supply chain couldn’t cope. With demand for thousands of new bikes and treads each day, the supply chain was not designed for this level of demand. And to twist the knife, global container transport had ground to a halt. This was a serious problem.

By September 2020 they had a major backlog of orders. At first, this was a “good problem.” With the scarcity only fuelling demand further. The market loved it.

But soon customers lost patience, especially during the holiday season. It wasn’t long before Peloton were paying to airfreight bikes over the Pacific Ocean as a damage limitation exercise.

What followed was a desperate grab for extra manufacturing and supply chain capacity. New supplier commitments, new outsourcing relationships, and plans to build a dedicated manufacturing facility in Ohio.

I’ve experienced major supply chain crises myself, many times. There is nothing quite like it.

You can imagine the phone calls… “I don’t care what it costs, just get the f-ing bikes here as quickly as possible!”

By the time the supply chain had unclogged, the gyms were open again, and customers had moved on.

Soon they had a lot more bikes than demand.

A LOT.

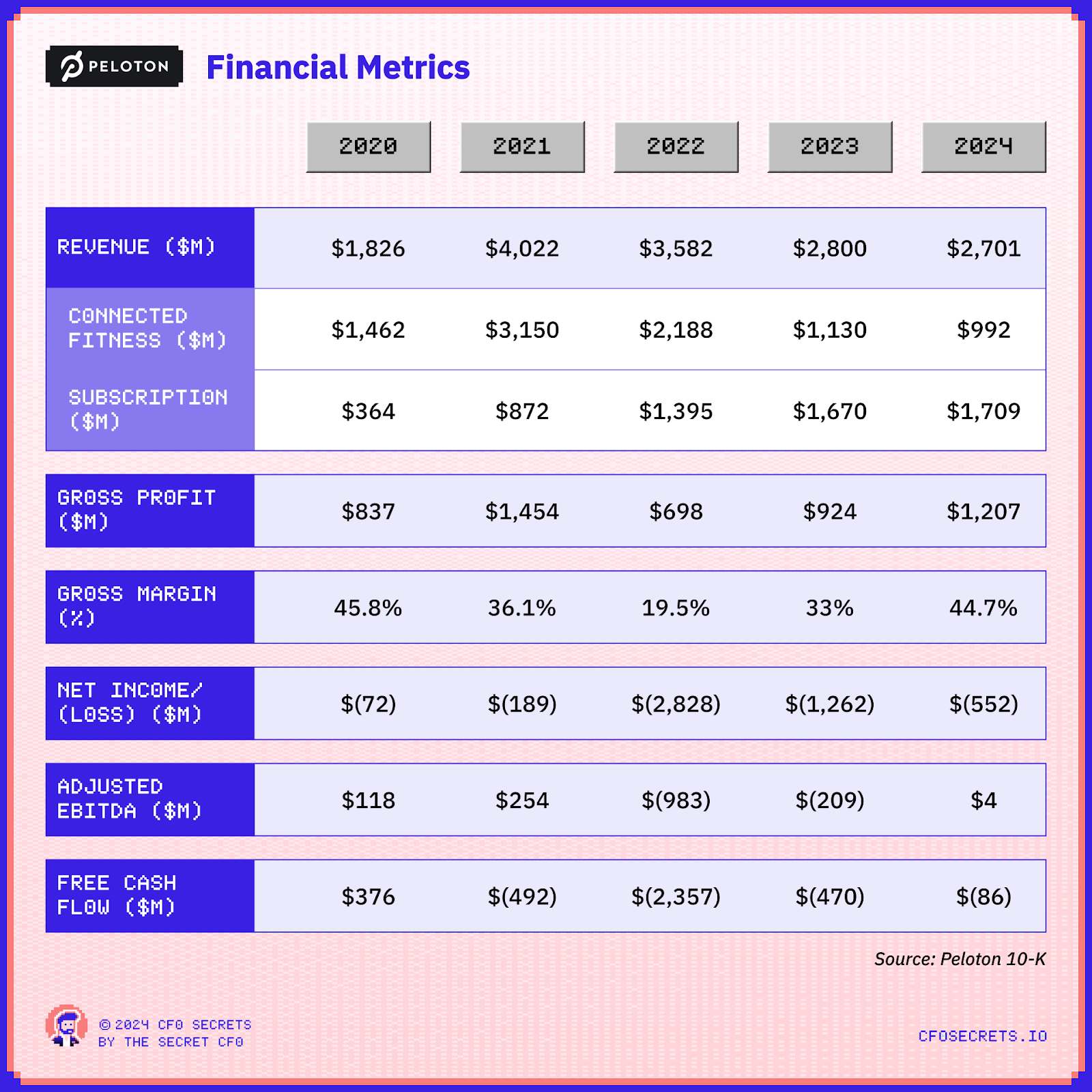

So, after the rocket ship growth of 2020 and early 2021, Peloton soon found itself with falling sales, gross margins collapsing from 40% to 20% (thanks to the supply chain issues), and exploding inventory levels.

That’s a recipe for a cash crisis.

The stock collapsed back to $25 by early 2022 and Foley was soon under pressure from investors. He decided it was time to ‘move up’ to executive chair, and appoint a CEO.

Enter Barry McCarthy…

Dissecting the 10K

This month we are going to cover how to interrogate financial statements like a CFO.

And we are going to use a single case study company throughout the series.

As you might have guessed from the opening story, that company is Peloton.

And why Peloton?

Well, it’s just so damn interesting.

Any company with a stock chart that looks like this…

And 5-year financials that look like this …

Source: Peloton 10-K. Data presented for Financial Year Ended June 30th.

… has a story to tell.

It’s got everything. Volatile margins, a turnaround plan, refinancing, control issues, a spicy definition of adjusted EBITDA.

Not to mention the CEO revolving door. As I was preparing this piece, Peloton named a new CEO after 6 months with interim co-CEOs.

The goal of this series is to share the process of interrogating company financials.

And sticking with a single subject company throughout this month will give us a chance to go seriously deep. The devil is always in the detail, especially in an earnings release.

So here is how we’ll tackle it:

Week 1 (Today) - Background & understanding the history and Peloton business

Week 2 - Unit economics & income statement

Week 3 - Capital structure & balance sheet

Week 4 - Maintainable free cash flow

But before we start, let me make this clear. This is not investment advice. I may have investments in Peloton or other companies that are discussed in this post. This post is for information and entertainment purposes only.

So, without further ado, let’s dive in…

The first step in any financial analysis is to make sure you have an elementary understanding of how the business makes money (or not). Let’s do that for Peloton.

Side note: if you are not familiar with the Peloton product. Watch this primer.

The Peloton business model

Is Peloton a content business, a fitness business, or a technology business?

It’s all 3. And it’s the integration of the three, that has led to such a fanatical community.

Without the content, it’s just a highly spec’d (and quite expensive) cardio machine.

And without the machines, it’s just a fitness content business (which could just as easily be a YouTube channel).

The core model should be simple.

They sell exercise machines, like bikes and treadmills, for an upfront price (at roughly breakeven) to customers. To make the most of those machines, customers subscribe to the monthly ‘Connected Fitness’ package for $44.

Peloton claims in their 10-K that subscriber revenue has a contribution margin of 72%. This means that ~$31 from each monthly subscription drops to the bottom line to cover fixed costs, customer acquisition costs, and returns to investors.

So the more subscription customers they can sell, and the longer they can keep them, the more profitable they will be.

It’s a higher-stakes version of the razor and blade model.

But clearly, life hasn’t been that simple…

Every finance professional worth their salt knows that it's the numbers that tell the story of a company. Not necessarily the rosy narrative spun up by management. Which is why once you understand the basics, the next stop should be the 10-K. Audited financials make it harder (but not impossible) to hide the bullsh*t.

Peloton has a June year-end, so conveniently their latest annual filing is only a couple of months old.

This 10-K deep dive will focus on the historical reported financials of the business. But the goal is to find the nuggets that indicate where the business is heading, and how quickly…

Viewing the financials through this lens gives us a list of issues and areas we can dive into further. Those topics are below. They will help guide our analysis over the next few weeks.

Here’s a link to the FY2024 10-K if you want to follow along.

1) How quickly can Peloton get back into growth?

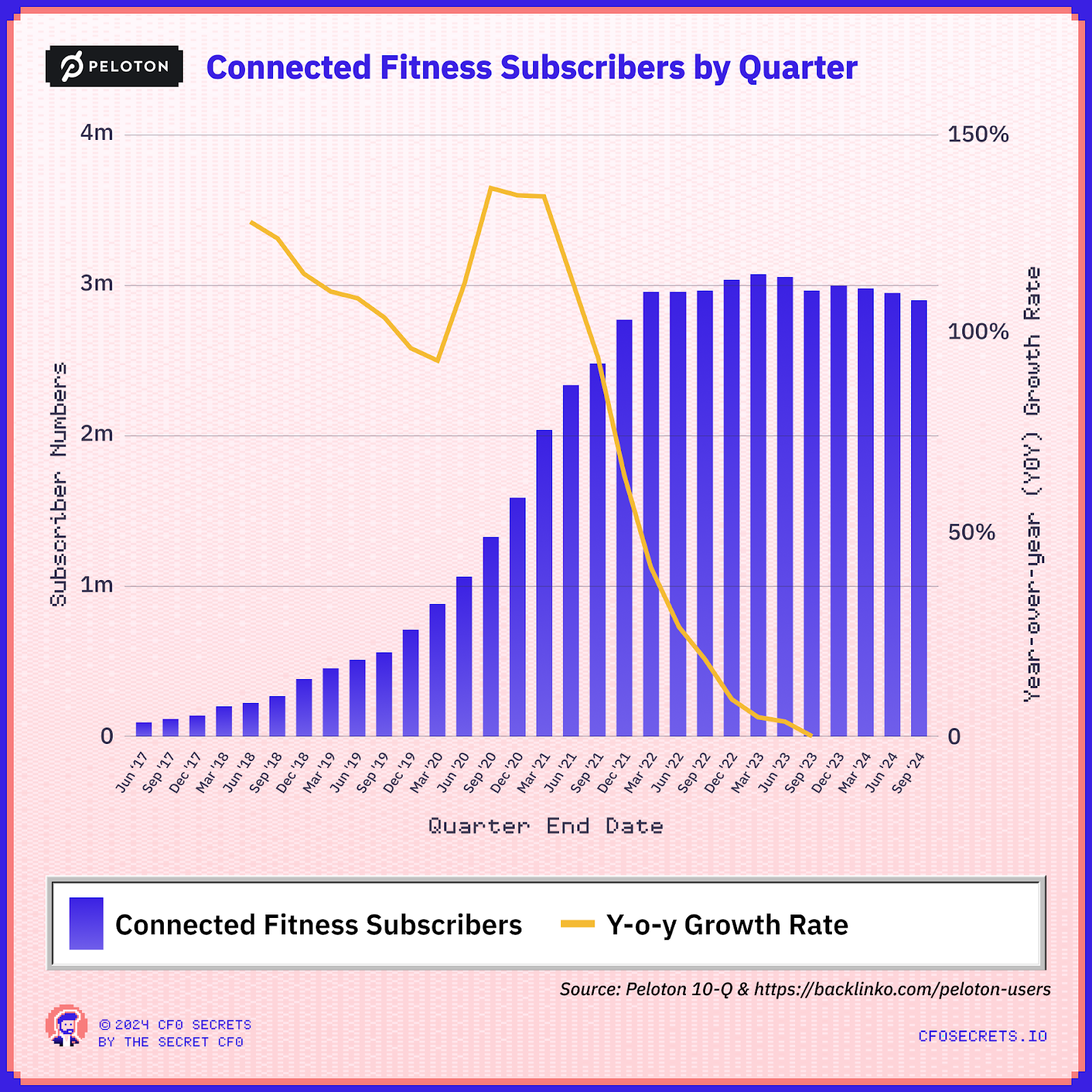

The growth curve for Peloton is very unusual. With subscriber numbers growing at venture scale, and then accelerating further post IPO before hitting a brick wall eighteen months later:

Sources: Peloton-10Q, S1, backlinko.com/peloton-users

At their IPO in 2019, Peloton was growing connected fitness subscribers consistently at a rate of ~100% year-on-year.

That shot up by another 40 points or so through the pandemic.

An accelerating growth rate on a growing base. It took the business from 0.5m subscribers to 3m in two and a half years.

Since 2021 Peloton has been stubbornly stuck at 3m subscribers and even moved into 2-4% decline over recent quarters.

They are now churning faster than they are selling new subscribers.

And that churn is accelerating (albeit from an impressively low base):

Source: Peloton 10-K. Data presented for Financial Year Ended June 30th.

Note: ‘Members’ includes free app users, paid app subscribers and connected fitness subscribers. It’s the connected fitness subscribers that drive the economics.

Average monthly churn has grown from 0.6% in FY2020 to 1.4% in FY2024. In recent quarters, monthly churn has grown further to 1.9%.

In 2020, they would have to sell roughly 4-5k new members per month to offset churn. Today that number is nearer 55k.

The core challenge for Peloton has been to right-size its cost base, capital structure, and supply chain to accommodate both its current business and ambitions.

But at some point, it will need to grow. Where will that growth come from? And can the restructured cost base and new channel strategy accommodate that growth?

Understanding where and when Peloton will grow is fundamental to the foundation of the unit economics.

2) What does the unit economic equation look like today?

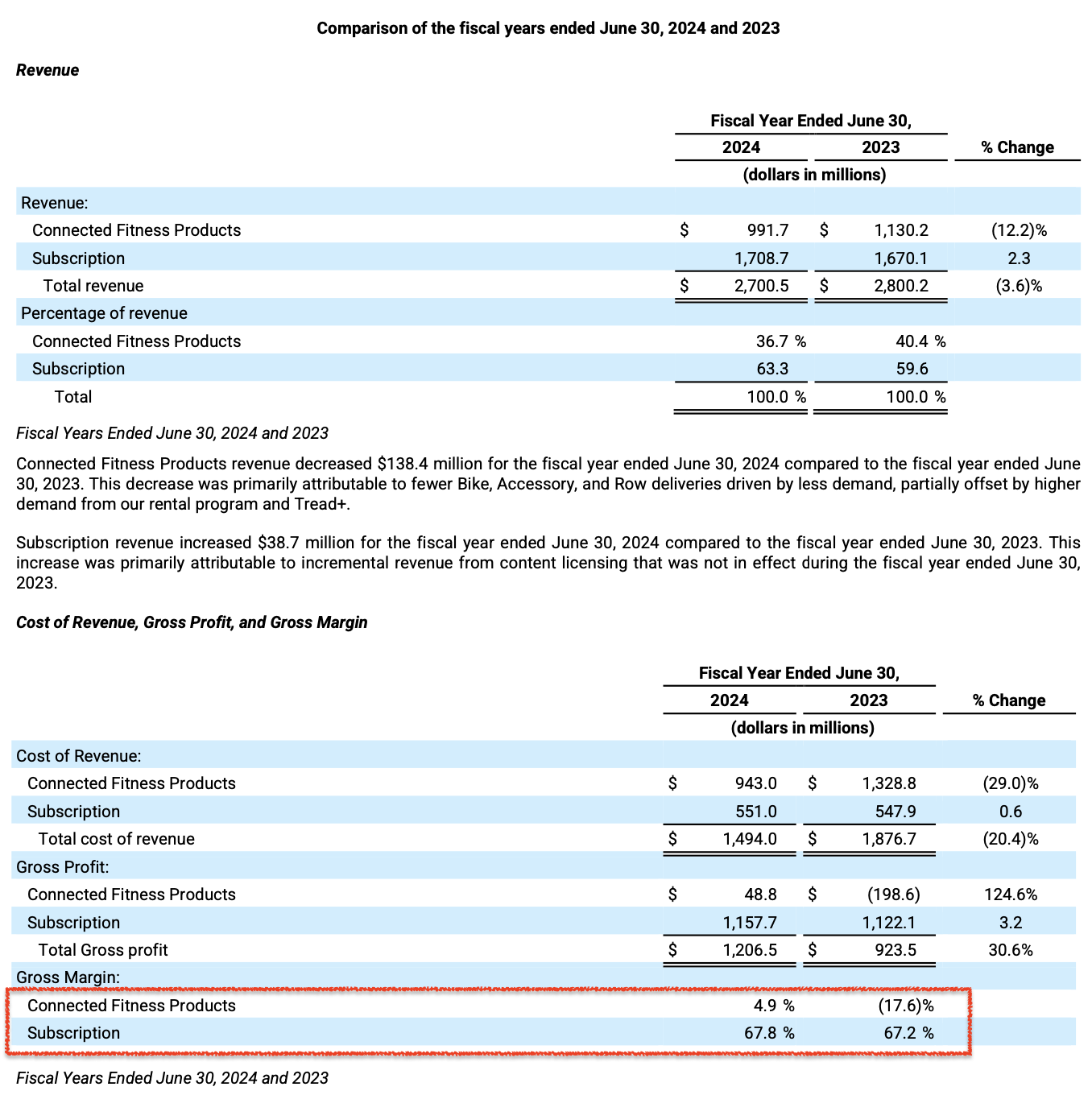

Subscription gross margin has been pretty resilient at 67%, and Peloton claims a 72% contribution margin. That’s pretty healthy.

Extract from Peloton 10-K

We need to ensure that the contribution margin assumption is robust, as it’s critical for the unit economics.

And margins on equipment sales have increased to 4.9% from (17.6)% in the previous year. After a period of volatility, can we now assume that Peloton will break even on equipment again?

And then there’s a new partnership with Costco at reduced prices. What effect will that have on the unit economic equation?

And how does the change in channel strategy affect their customer acquisition cost?

All of this will need to come together to establish the trends in Customer Lifetime Value (CLV) vs Customer Acquisition Cost (CAC). And the rate at which Peloton can recover its fixed costs (and then deliver a return).

3) What does the fixed cost base now look like?

The cost base exploded following the IPO. Both intentionally and unintentionally.

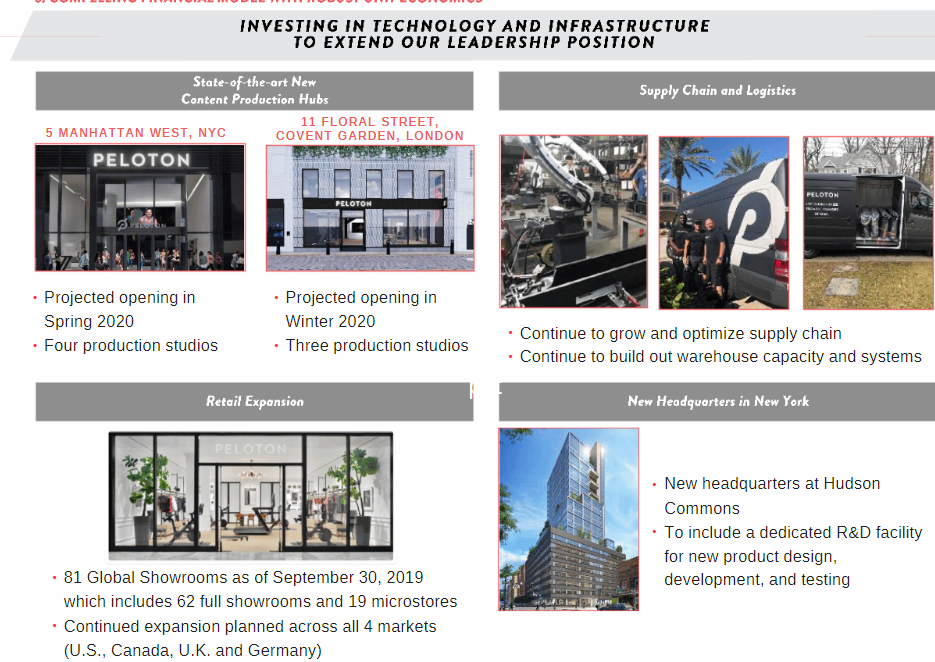

Firstly there were planned investments in retail stores, new headquarters, R&D, and manufacturing capacity.

McCarthy was quoted in 2022 as saying Peloton had “spent money on things that they shouldn’t have.”

Source: 2020 investor presentation

And then there were the unintended consequences of the supply chain issues. Massive inventory write-downs, astronomical shipping costs, and supplier settlements. The supply chain issues cost them hundreds of millions, maybe even more than a billion, against their planned unit economics.

As a result, gross margins on equipment were negative double digits through this period.

This is when Barry McCarthy came in with his ax.

On day 1 he announced a restructuring plan expected to save $800m of annual expenses. The restructuring plan included:

a headcount cull of 2,800 people; 20% of the workforce.

closure of many several retail locations

canceling the plan for the $400m investment in a manufacturing facility in Ohio.

Being good at fitness, technology, and content all at the same time is hard.

But also being good at retail and manufacturing at the same time is just not possible. Especially for a relatively young company.

McCarthy took the business ‘back to core.’

And there were more cuts to come. A further restructuring plan was announced earlier this year, including more retail closures and another 15% headcount cull.

So the question now is what will the new cost base look like? How much will it cost to get there? And are there any circular effects on the customer acquisition cost profile through reducing the retail real estate? How does all of this affect the cashflow breakeven point of Peloton?

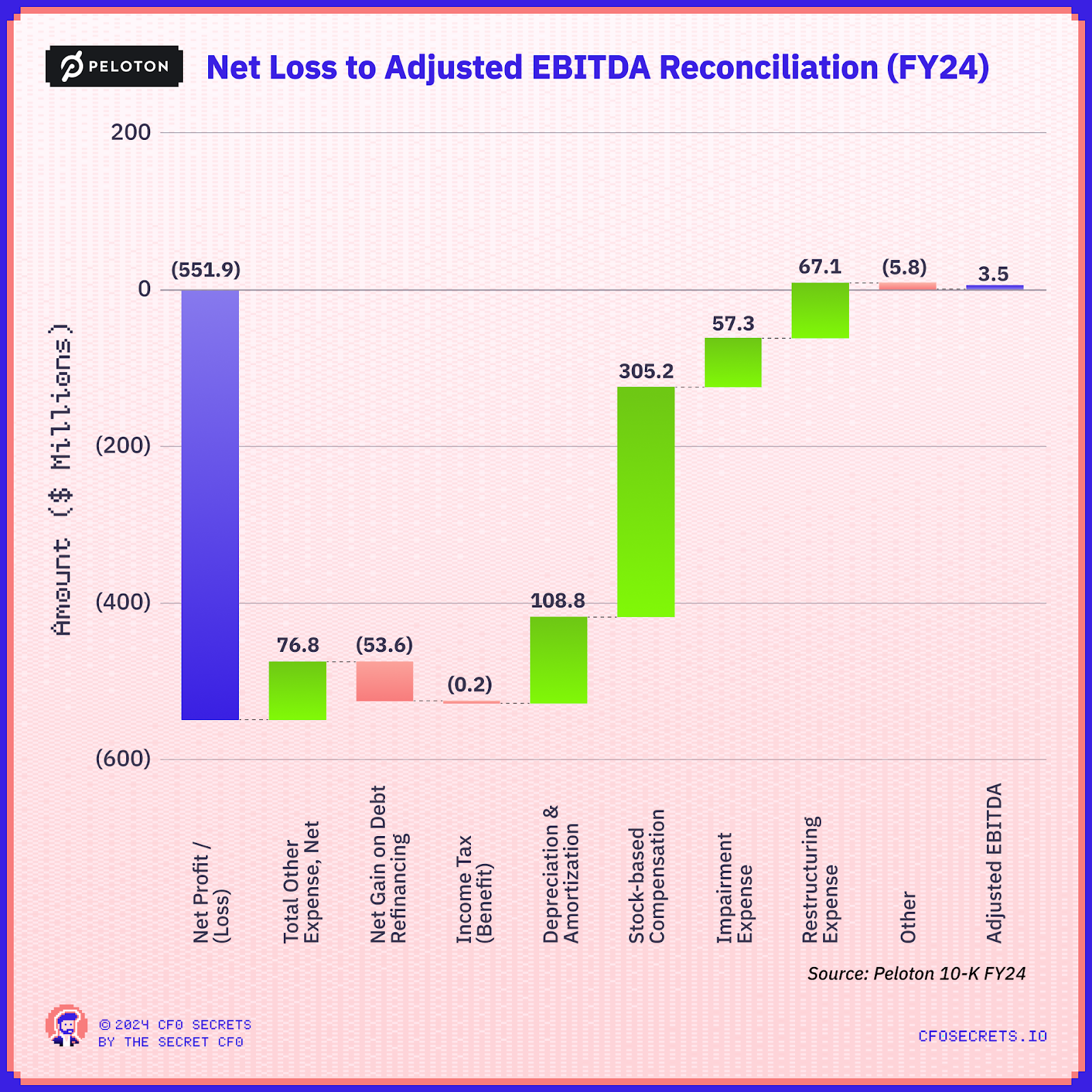

4) Look at this ABSOLUTE DOOZY of an adjusted EBITDA reconciliation.

Source: Peloton 10-K

The adjusted EBITDA chefs at Peloton have been busy in the kitchen, and I can’t wait to try what they are cooking. You know we are going through that line by line…

6) What is the current rate of maintainable free cash flow per share?

On the March 22 earnings call, McCarthy said, "The cash issues are more severe than I thought they were when I took the job."

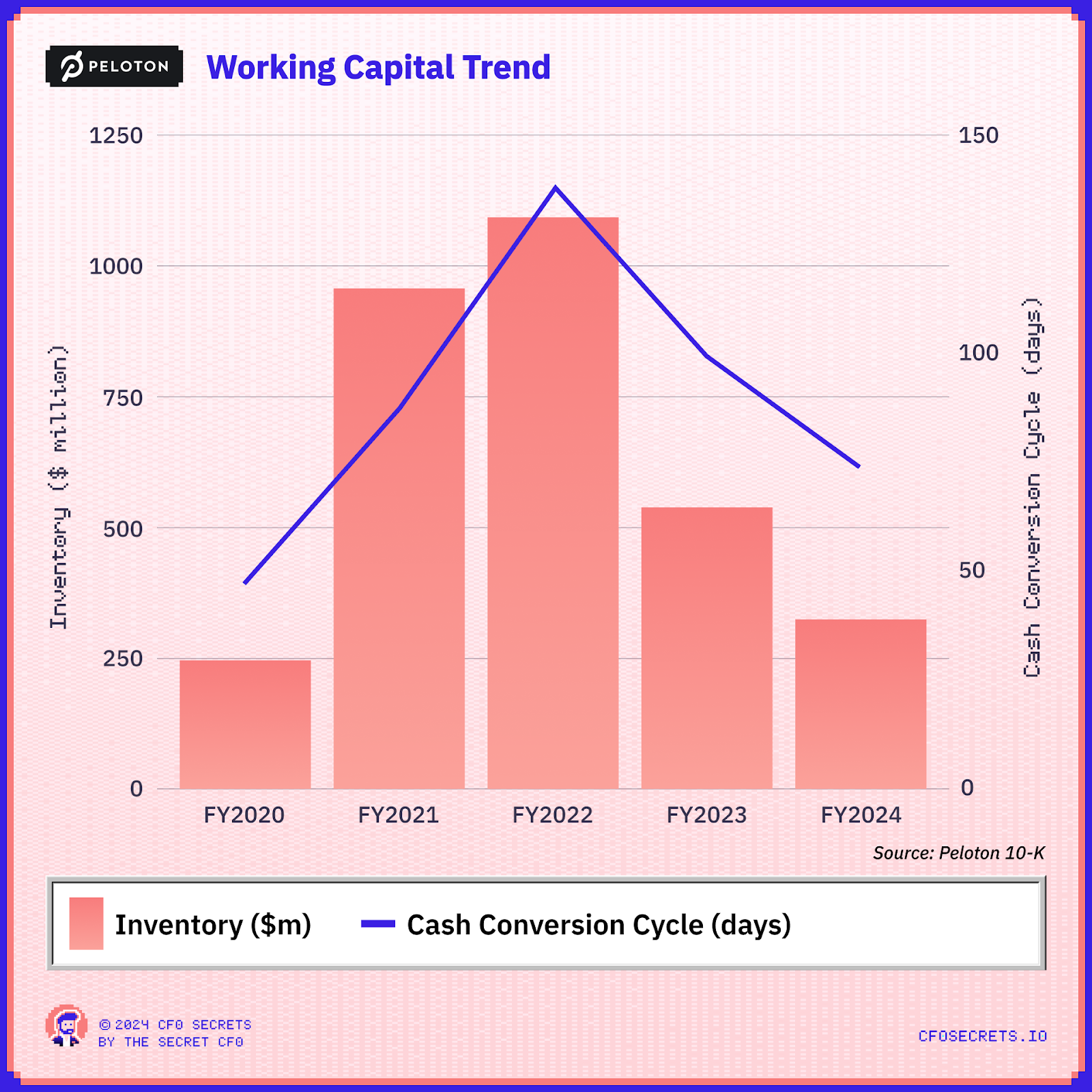

Look what happened to inventory during the supply chain panic:

Source: Peloton 10-K

Between the gross margin crisis and an explosion in the cost base… it’s a miracle they stayed solvent.

We will need to get under the hood of working capital. And understand maintainable free cash flow for the business as of today.

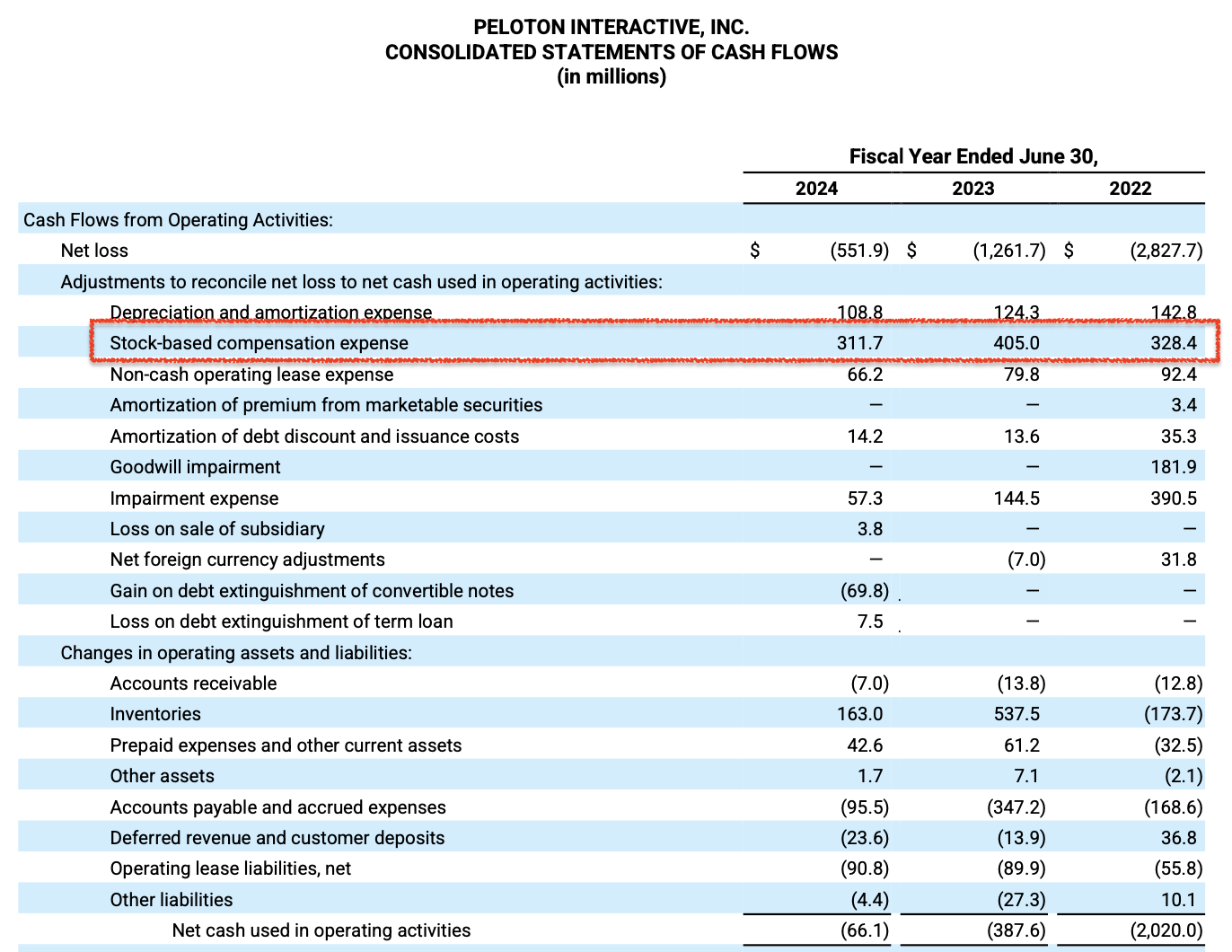

With stock-based compensation consistently over $300m, that’s going to be interesting:

Extract From Peloton 10-K

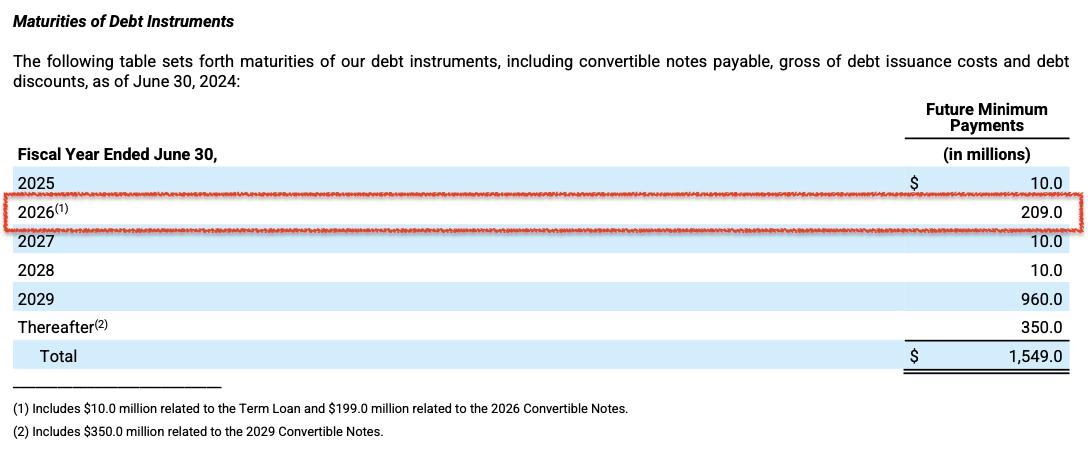

6) What effect does the recent refinancing have on the capital structure and cash flow?

In May, Peloton successfully refinanced most of its debt. But there is still ~$200m of 2026 maturing convertible notes outstanding:

Extract from Peloton 10-K

We need to understand whether Peloton can afford to repay the rest of that debt. And if not, what will the dilution effect be on the share count?

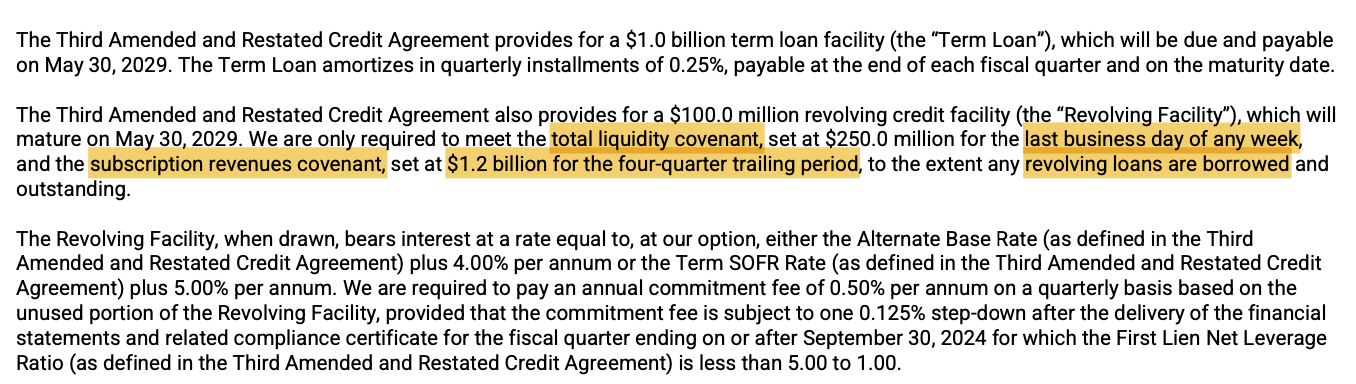

There are plenty of interesting things in terms of the new debt, too. Including a minimum liquidity covenant tested WEEKLY. Not something I’ve seen before:

Extract from Peloton 10-K

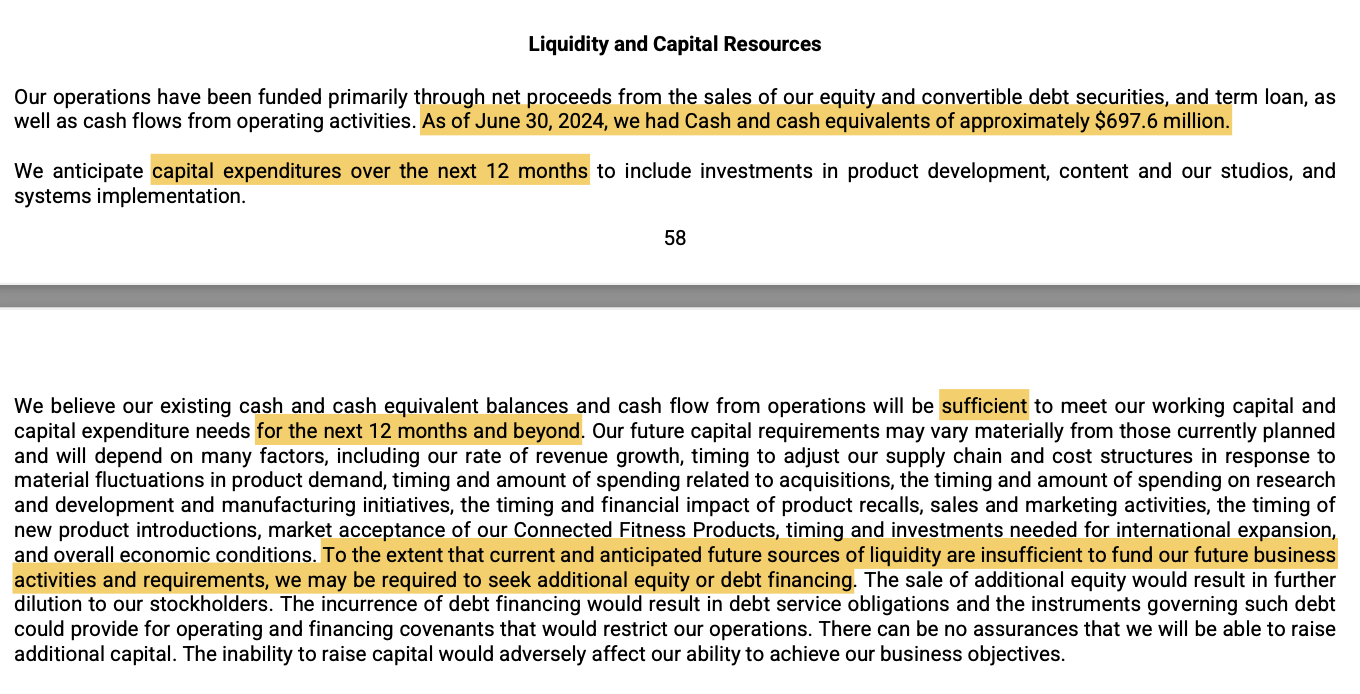

7) Does Peloton have enough liquidity?

They had $698m of cash at the end of June 24, plus an undrawn $100m RCF. So total liquidity of $798m.

Extract from Peloton 10-K

Is that enough to fund the cash burn for the next 24 months or so? And how resilient are they to the seasonal volatility in sales? They talk about 60% of annual sales occurring in Q2 & Q3 which will come with a working capital impact.

Overlaying seasonal volatility onto a weekly minimum liquidity covenant is particularly interesting. We will get into that and stress-test their liquidity. And at what level would an increase in churn threaten liquidity?

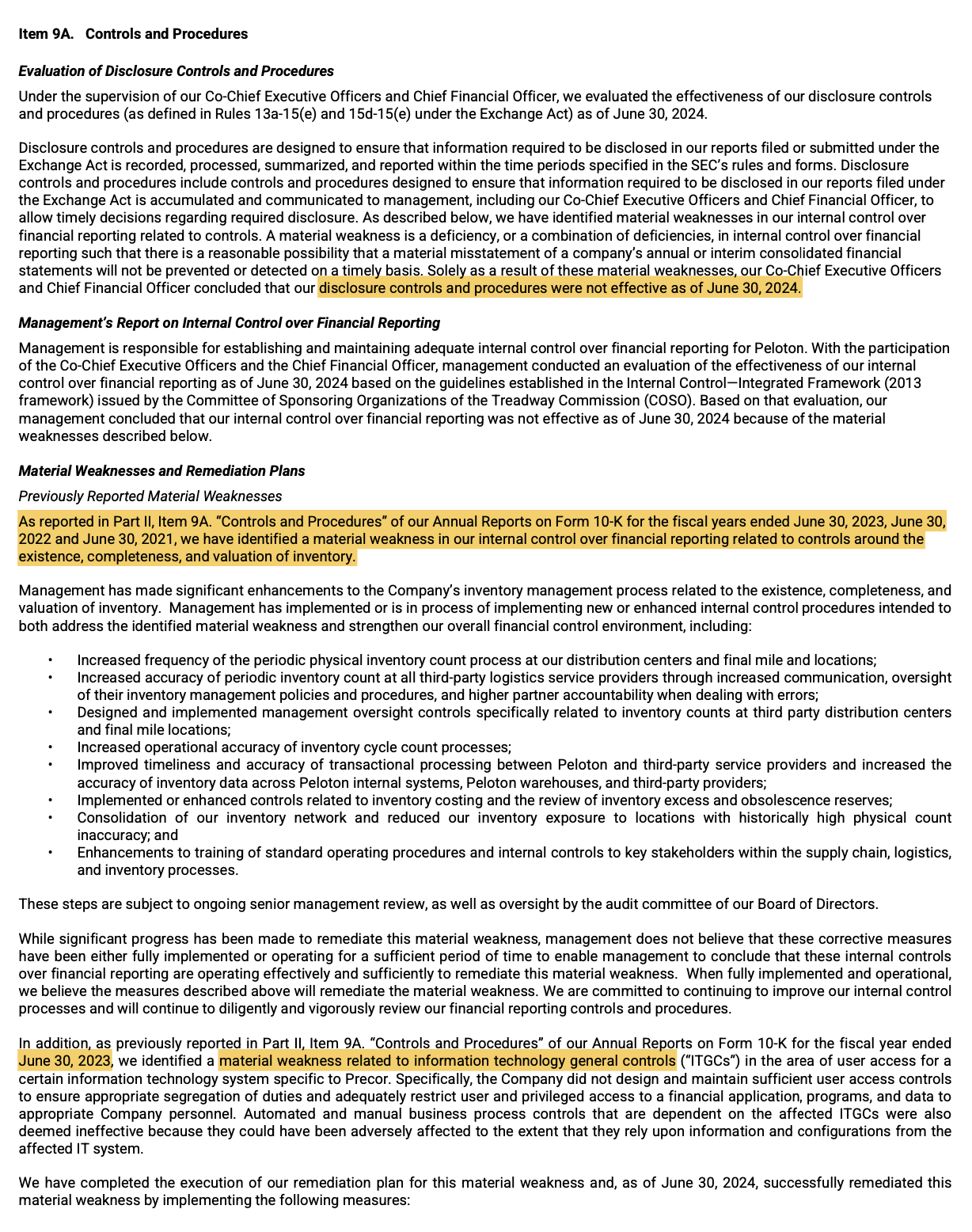

9) Are the internal controls fixed?

Fun fact if you hit Ctrl+F and type ‘Material Weakness’ and hit Return… you will get 119 results. One hundred and nineteen.

The SOX reporting was ugly reading throughout the chaos period. Seriously ugly…

Extract from Peloton 10-K

That’s a long way of saying. “Hey, yeah, for those 3 years… we had some bikes and some treadmills. But we didn’t know how many, where they were, or what they were worth.” A true nightmare.

As a new CEO/CFO, you get one chance to clean up this sort of thing. Air the bad news, and blame the previous regime (without ever saying it outright). And then work on fixing it.

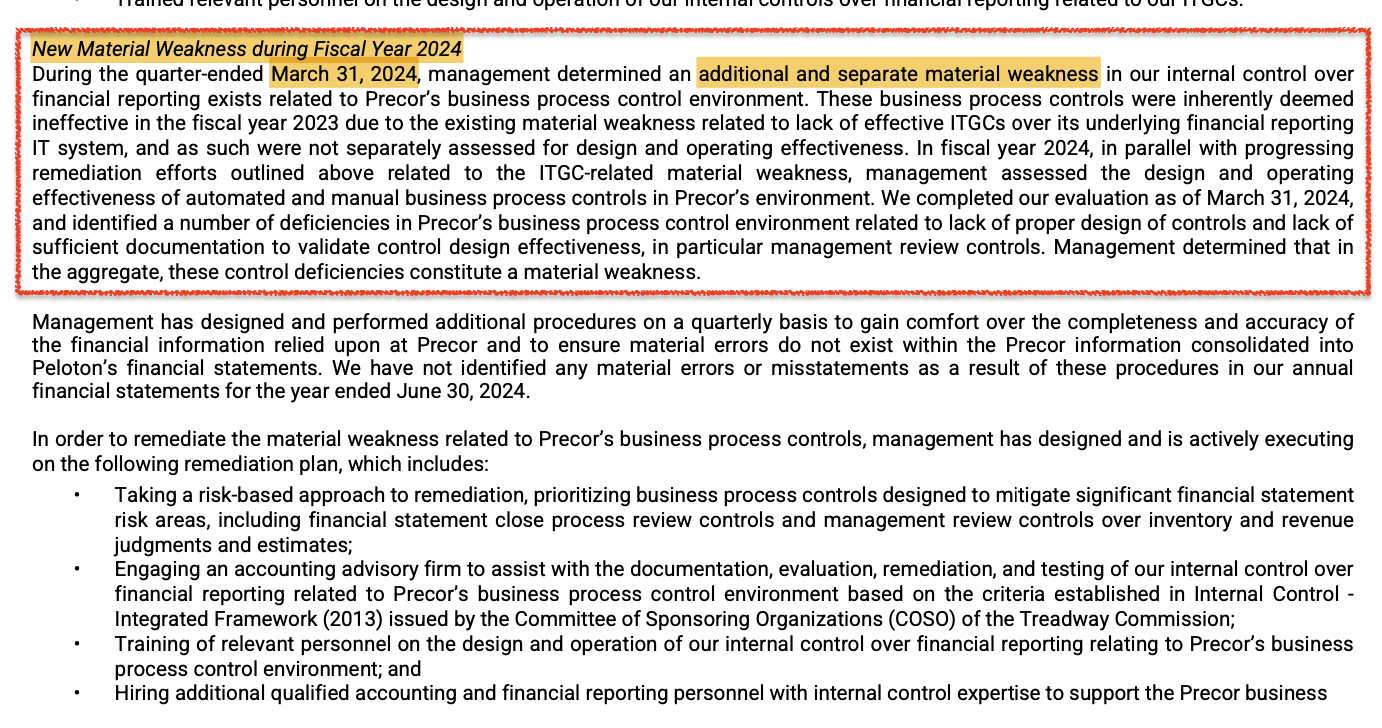

Which is why I was surprised to find this:

Extract from Peloton 10-K

A NEW control issue was identified for the financial year ending June 30, 2024. It’s hard to see why this wasn’t identified earlier. Frankly, that is a bad look.

Continuing concern around inventory accounting means the gross margins on the connected fitness products business will need even more scrutiny if we are going to get a clean read on unit economics.

Wrapping up

At this stage, there are many more questions than answers. The job over the next 3 weeks is to organize and answer these questions and share the process with you as we go.

That starts next week as we get into the weeds of the Peloton P&L.

One thing is clear though. The turnaround of Peloton is harder going than expected. McCarthy eventually stepped down in May of this year.

In a press interview following his resignation, he said “Turnarounds are a young man's game. I think it’s time for me to step aside and allow new leadership to take the company forward.”

“To shareholders, I once described turnarounds as full contact sport; intellectually challenging, emotionally draining, physically exhausting, and all consuming, the decisions never more consequential, the urgency every present, the teamwork never more central to the mission. From where I sit today, that pretty much explains my experience these last two years.”

And hot off the press… after a 6-month search, two days ago Peter Stern was appointed as the CEO charged with getting Peloton back into growth. Will he be Peloton’s white knight?

So many questions. This is going to be fun.

If you want to follow along in real time, the most recent 10K is a good place to start. And this episode of Acquired is a nice overview of the story up to the McCarthy appointment.

See you next week, when we’ll get into the weeds of Peloton’s unit economics.

You can’t understand the numbers until you understand the business

Turnarounds are always harder than you expect!

It’s 10x easier to put cost in than it is to take it out

And Finally

No Q&A this week, I had to cut some things to make room for all those 10-K screenshots.

Thank you to today’s sponsor… Close your books in minutes not weeks with accounting automation from Brex.

Next week we’ll dive into Peloton’s unit economics. If you follow the Peloton business, or read the 10-K, and have any thoughts, I’d love to hear them. You can send them straight to me by just hitting reply…

Stay crispy,

The Secret CFO

Disclaimer: I am not your accountant, investment advisor, tax advisor, lawyer, CFO, director, or friend. Well, maybe I’m your friend, but I am not any of those other things. Everything I publish represents my opinions only, not advice. And certainly is not investment advice. Running the finances for a company is serious business, and you should take the proper advice you need.

What did you think of this week’s edition?