Orb makes the hassle of usage-based billing a thing of the past.

Finance leaders know how much of a headache usage-based pricing can be, even if it’s a hit with customers. Discounts, non-first-aligned billing, and custom contract terms can make closing the books painful.

Orb’s CEO, Alvaro Morales shares how to migrate smoothly to a usage-based pricing model for better reporting and fewer headaches.

Losing control

"We've put the last year behind us. The future is bright."

It was my first time meeting Edward. The VP responsible for this particular business unit.

He was certainly optimistic.

His BU had been at the top of my hit list for a visit since I started in the role a few weeks earlier.

And for good reason…

Just before I joined, there had been a huge reporting issue.

The Director of Finance had been wilfully manipulating results and was fired. The Group had to issue a restatement for nearly $15m.

As you’d expect, there had been several casualties in finance. And now I was here as the business unit CFO responsible for the clean-up job.

Alongside the job of repairing reporting and control issues, the business unit had won a major contract that would double sales from $80m to nearer $150m.

Edward explained the new contract win would move the business from a $10m loss (after the adjustments to correct the reporting) to a $5m profit.

$15m of contribution margin on $70m of new sales sounded promising.

There was one problem. Most of that new volume had been onboarded in the last couple of months. Yet there was no sign of that additional profit in last month’s accounts. The revenue was there, but the losses had, in fact, widened.

When I challenged him, Edward explained this was just teething problems with the new contract.

While the huge adverse operational variances in the Income Statement for the most recent month were consistent with that explanation, something didn’t smell right.

And given the recent history here, I had every right to be suspicious.

Susanne (the new Director of Finance for the business unit) to go through the standard costings for the new product launches.

Susanne had only been in the role for a few months. And understandably, until now, had been focused on cleaning the balance sheet and reporting.

3 days later she called me:

“There's a big problem. I've been through the standard costing model. It's complicated. But the base data for the costing assumptions was pulled from the accounts that we now know were wrong. The whole contract has been under-costed and priced incorrectly.”

"Oh shit. By how much?"

"Hard to say, as we aren't yet in any position to be accurate at a product level. But, I'm pretty sure when it shakes out this contract will have a negative contribution margin. I think it's been under-costed by 20%-25%.”

I spat my coffee out (like in a cartoon).

This business unit was hemorrhaging cash.

If this was right, Edward's $5m profit projection was nonsense. His business would lose at least $15m annually. He had no clue what was happening in his own business or why (notwithstanding he had been badly let down by his previous finance team).

To cut a long (and complicated) story short… Susanne's high-level conclusion turned out to be right. To make things worse, this factory had locked that additional volume into long-term contracts. And, ultimately, it was unfixable.

They could have recovered from the reporting problem, but not from this.

The consequence was that the factory had to be closed. 900 people lost their jobs.

All driven by an error in unit economic calculations.

This is the first part of a three-part series on unit economics.

Costs Behaving Badly

This July series will focus on unit economics. Long-time readers will know that we tackled this topic piecemeal earlier in the life of CFO Secrets (before we adopted the series format).

So, this month we will go deeper into unit economics and their practical applications.

This week though, we will recap unit economics 101.

Let’s get into it:

What does unit economics mean?

The technical definition is the measurement of profit on a per-unit basis.

But I prefer to think about it more broadly than that…

Unit economics is the science of how your business makes money.

Why are unit economics important?

The best CEOs and CFOs I have worked with all had an incredible feel for the unit economics of their business. They could quickly (mentally) calculate what a new store, product launch, discount, new hire, etc. would mean for their business in $ and cents.

They didn’t put the whole business on standby, drowning in weeks of analysis to make 95% of their everyday decisions. They saved that resource for the more complex decisions.

Think of it like Daniel Kahneman’s System 1 thinking vs System 2. By making more everyday decisions from System 1, it gave System 2 more capacity to process harder problems.

The result of that is faster decision-making and better execution.

And you have heard me stress the importance of speed of execution in business success. It’s everything.

Finance’s role in unit economics

Think of this in three levels:

Level 1: Firstly, unit economic analysis is useless without good bookkeeping. You MUST have accurate and well-controlled systems for cost capture and coding. We saw in the opening anecdote how bad this can be when it goes wrong.

Level 2: Secondly, with the right data captured, you must have the analysis skills and commercial savvy to understand the business’s unit economics as a finance team. Whether that’s through costing models, cost curves, contribution statements, etc. But it’s not just about the analysis, you have to bring it back to the ‘corner shop.’ What does it mean in practice? Most FP&A teams are bad at this from my experience. The best I’ve seen tend to be CEOs and founders.

Level 3: Finally, good finance teams have an intimate understanding of the business’s unit economics. But GREAT finance teams find ways to share that understanding with the business. That’s about education. But also about business processes. Whether that’s pricing decisions, capital expenditure investments, or operational improvement initiatives. How do you embed an education on the unit economics of the business into the processes?

Whether you are at level 1, 2, or 3 depends on the maturity of your business and finance team.

You must assess your current state critically. I’ve seen many examples where issues that were thought to be Level 3, were, in fact, Level 1.

I once saw an instance where the finance team was struggling to explain its costing model to the operations and commercial teams. It was seen as a ‘complicated finance tool’ and buy-in was difficult. The model was robust. It worked. But they were right… it was complicated.

For a long time, it was assumed to be a communication / capability issue in the FP&A team. A level 3 issue. But it turned out the root cause was a messy chart of accounts (level one problem). Once fixed, the rest fell into place.

Unit Economics 101

Let’s get into some terminology

Variable costs: costs that vary directly with volume

Fixed costs: commonly defined as costs fixed regardless of volume. Things like rent, management salaries, etc. I prefer to think of them as costs that vary with time rather than volume.

Contribution margin per unit: Average selling price per unit minus average variable cost per unit (i.e. the incremental $ profit you make from one additional unit sale)

Breakeven point: the number of units you have to sell to ensure you are not losing money. Especially important for businesses on the growth curve. Calculated as fixed costs/contribution margin per unit

We explored this terminology in more detail in this earlier post.

No doubt you have seen break-even charts before. My favorite illustrations are the following:

Source: Kaplan

Source: Toptal Finance

If you are looking for a worked example of breakeven analysis, please check out these two:

Operating Leverage

Operating leverage refers to the mix of fixed costs and variable costs in your business.

High operating leverage: Fixed costs are the dominant part of the cost structure

Low operating leverage: Variable costs are the dominant part of the cost structure

High operating leverage works well at scale. The more scale you have, the more unit volume you have to divide your fixed costs by (and the lower your total cost per unit).

Another way to describe operating leverage is the ‘cost structure’ of a business.

For example, a high-growth business might test new volume levels on a cost structure weighted on variable costs (to reduce exposure to volume fluctuations). And as confidence levels increase in volume levels, so can the investment in fixed cost.

The reason you see so many DTC ecommerce start ups on your instagram fees is that they can be started with zero operating leverage, limiting downside. Here’s the playbook: Find a dropshipper with a product they like, spin up a shopify website for next to no investment. If it doesn’t work, kill it a month later. If there’s demand, double down and invest in fixed costs and a supply chain to make it more efficient.

Operating leverage is interesting in seasonal businesses too. They are hard to manage, because of the need to flex the cost base to meet the volume volatility in the business. Effectively forcing low operating leverage.

Well-placed fixed-cost investments become effective barriers to new entry. We are seeing an interesting time with automation and robotics. As businesses convert variable costs (labor) to fixed costs (depreciation and engineering).

This will eventually become an arms race, as it will lock out new entrants who simply won’t be able to afford to make the fixed-cost investments necessary to compete.

All costs are mixed if you look hard enough

Our finance education suggests that costs show up wearing a name badge: ‘fixed’ or ‘variable’.

In practice, they do not.

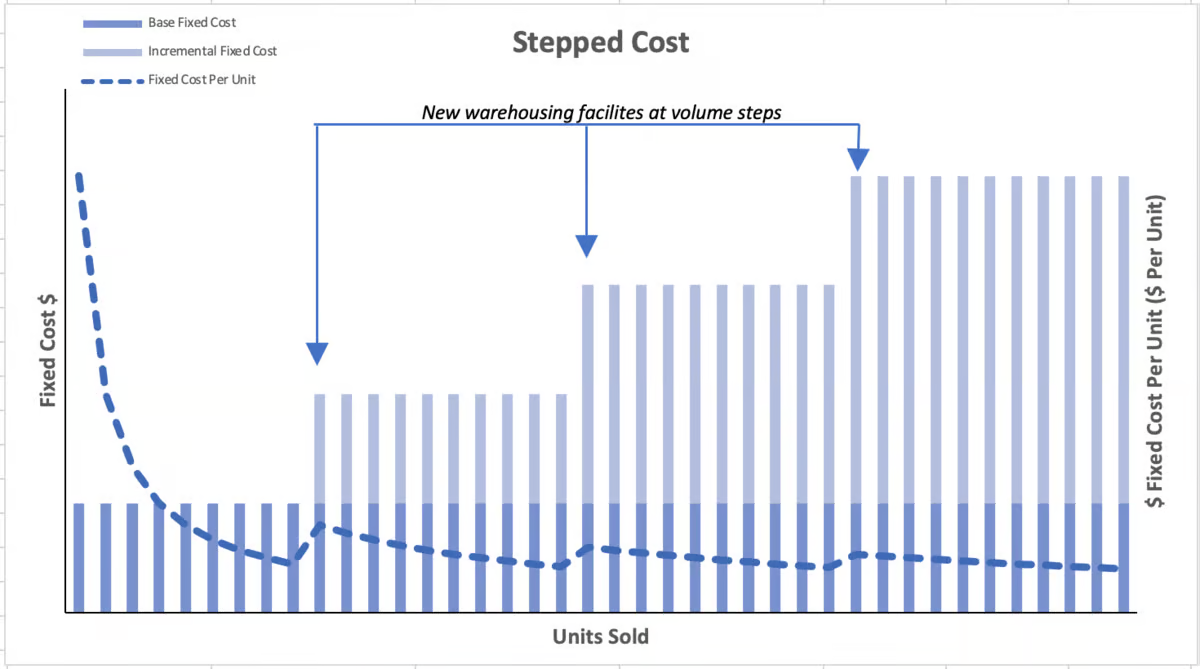

For example, rent is a fixed cost. Until it isn’t …

Once you outgrow one warehouse and need a second, your rent just unfixed itself.

Secret CFO: https://www.cfosecrets.io/p/fixed-variable-costs

We call these mixed costs. And, in fact, when you look hard enough, all costs are mixed costs.

Very few costs remain the same (either on a $ or per unit basis) for the same business at 10 units and 1,000,000 units.

You would expect your so-called variable cost to get cheaper on a per unit basis as your business grows. You can negotiate better deals with suppliers.

And suppliers have their own unit economics, so it’s reasonable to believe they can serve you more efficiently as you help them grow their business.

Likewise, fixed costs are only fixed to a point. Once you move through a certain volume level, those fixed cost will ‘step’ out. Managing those steps effectively is the name of the game.

If you take on fixed costs before you have the volume, you end up with stranded costs. And that can get hideous:

Secret CFO: https://www.cfosecrets.io/p/fixed-variable-costs

Logan Paul’s Prime brand is a great example. Some people have called it the most successful CPG launch in history. And it’s hard to argue. Sales reportedly exploded to more than $1.2bn in the first full year.

The supply chain couldn’t keep up, meaning shelves were empty. Bottles started changing hands on eBay for up to $1,500. The Secret CFO Jr’s even talked this frugal old finance boy into paying $20 a bottle at one point.

Buoyed by the demand explosion, the supply chain turned the machine on to deliver the astronomical levels of demand. One problem: once the initial hype had settled, sales started to fall. Leaving surplus stock. Which had to be discounted, presumably killing margins.

Getting the balance between flexibility, efficiency, and the lowest cost price in a supply chain is tough. Especially if demand is volatile. It will be fascinating to see how Prime addresses this.

Cost Behavior vs. Cost Classification

One common misunderstanding.

People often confuse gross profit with contribution margin.

They are different.

Gross profit is an accounting term, driven by the technical accounting definitions of costs. Whether they are ‘directly attributable’ or not. This is open to interpretation and applied very inconsistently across businesses.

Contribution focuses not on technical definitions. But on the substance of a cost. It’s behavior.

You can see here that the cost of sales (inverse of gross profit) can include fixed and variable components.

Accountants frequently get this point wrong and obsess with gross margin at the expense of contribution margin. When asked about cost structure, your average CPA will be snow-blinded by cost classification issues. That is the wrong lens for unit economic analysis.

It’s cost behavior that matters in unit economics. Not where it sits in the income statement.

Naturally, if you can build a chart of accounts that aligns cost behavior to classification, that makes this all much easier.

We previously tackled this point in depth.

Costs behaving badly

There’s just one problem with cost behavior. Costs don’t always behave themselves…

For example, we saw those nice clean straight lines in the breakeven charts we shared earlier. But when you zoom out, there is no linear relationship between volume and profits

Secret CFO: https://www.cfosecrets.io/p/unit-economics

So costs will only behave in a linear way inside certain relevant ranges of volumes. Those ranges could be defined by your manufacturing capacity, warehouse space, supplier contract volume parameters, management, and marketing channel costs. Anything.

We walked through a detailed example here.

The crucial point is that unit economics is a science, yes. But it’s an imperfect one. It only works alongside a robust understanding of the business.

Every rock star CEO I’ve ever worked with can do this unit economic math on a napkin. Often in extraordinary detail for their business.

But here are some steps you can take to better understand your own unit economics

Breakdown your current cost behavior (fixed vs. variable)

What would your breakeven volume or volume required for target profit be?

What is your relevant range? At what volume level would your cost structure change?

Use low operating leverage to start (proving demand). Fixed costs are 10x easier to increase than to reduce.

Set upper and lower bounds for your cost structure, so you are ‘ready to go’ in either direction

Repeat 3-5 assuming your volume was 3x the size & 50% of the size. Understand your volume breakout impacts in both directions.

Think about the cost dynamics for your customers, competitors, and suppliers too - find moats

Next week we’ll get into the practical ways you can drive unit economics in your favor.

A good CFO is a Jedi in unit economic napkin math for their business.

Cost behavior and cost classification are two different things. Focus on cost behavior for unit economics.

There is no such thing as pure variable or pure fixed costs. All costs are mixed in practice.

Mike and the Mad Dog from Truckee, California asked:

I actually have two questions:

1. I was trained in using marginal cost of capital in my WACC. And in general, always looking at marginal and incremental vs. historical cost and allocation.

Q: When do you think historical cost is important as part of decision-making?

2. Curious how you take notes in meetings and use them going forward?

I guess I can give you two questions, one for Mike and one for the Mad Dog.

On your first question. I think a full blended current cost of capital WACC is important in ensuring your overall strategy and returns profile works in the context of your actual delivered returns for shareholders.

Ultimately, if you are ensuring your decisions are always optimized to the higher of WACC and marginal cost of funds, then you can’t go far wrong…

On the second question, it’s an interesting one. I’ve worked with a brilliant CEO who took pages of notes in every meeting and could refer back to them at will. I still have no idea how he did it. I suspect he had a photographic memory and chose not to tell anyone.

My style is to capture a handful of key notes. That tends to mean two or three takeaways from a meeting. If it’s less than that, it means I shouldn’t have been in the meeting, and I make sure I am not next time.

I use a digital notepad and organize my topics into different folders and notebooks. I love it because it offers the simplicity of paper and pen, but takes it from a 2D tool to a 4D tool, with everything in one place.

Referring back becomes much simpler when your notes are organized by topic.

I don’t claim to be particularly strong in this area, though, so find a system that works for you.

If you would like to submit a question, please fill out this form.

And Finally

Next week we’ll get into how to drive unit economics in a business.

If you enjoyed today’s content, don’t forget to check out this week’s sponsor Orb.

Stay crispy,

The Secret CFO

Disclaimer: I am not your accountant, investment advisor, tax advisor, lawyer, CFO, director, or friend. Well, maybe I’m your friend, but I am not any of those other things. Everything I publish represents my opinions only, not advice. And certainly is not investment advice. Running the finances for a company is serious business, and you should take the proper advice you need.

What did you think of this week’s edition?