Expand globally, operate locally

CFOs often must navigate complex international regulations and financial risks to ensure successful global expansion. So what do they need to know to succeed? The global CFO playbook shares how top finance leaders manage FX risk, simplify tax and regulatory compliance, and localize their operations to improve their ROI.

P&L under the microscope

Welcome to part two of our Peloton deep dive. Last week we set the scene.

This week, we're ripping into their P&L to understand:

Are they actually making money on bikes and treads?

How profitable is that $44/month subscription?

What the hell is going on in the cost base?

If you missed part one, catch up here.

As a reminder…

This is not investment advice. I may have investments in Peloton or other companies that are discussed in this post. And you might too if you own index funds! This post is for information and entertainment purposes only. Any assumptions made are my own.

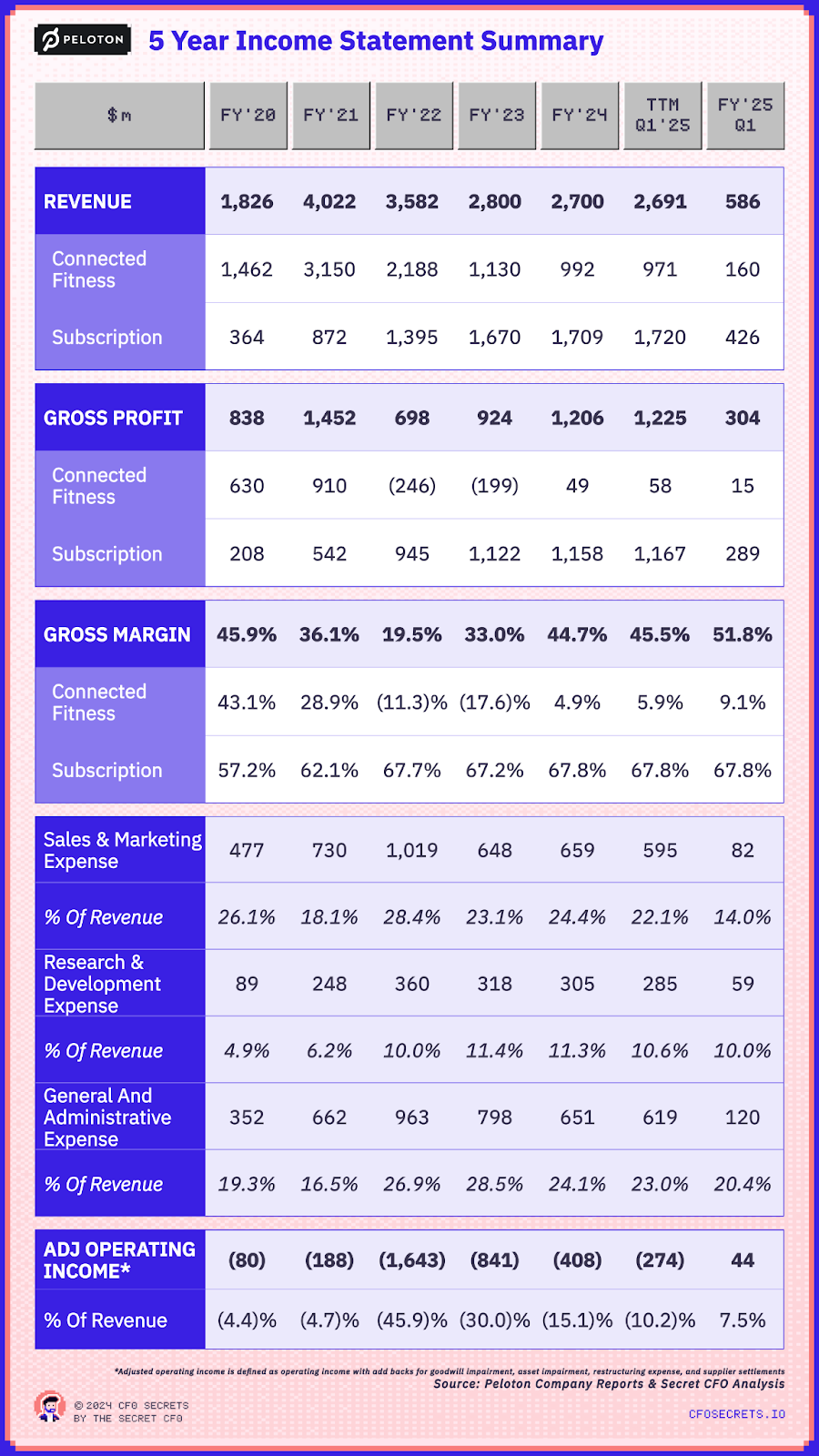

Now let’s dive straight into the Peloton Income Statement (Peloton has a June year-end):

Full disclosure: I'm a turnaround CFO, not a subscription business veteran. I've analyzed this the way any CFO would approach a new business - by following the money and asking obvious questions. If you're a subscription expert with a different take, I'd love to hear it.

Sales

Peloton's sales have grown from $1.8bn in FY20 to $2.7bn in FY24. But the shift in mix is huge. Just 20% of revenue in FY20 was from subscriptions. That is up to 60% last year.

The Peloton management team is forecasting that sales will fall to $2.5bn for FY25. Churn is increasing (more on that later).

And they are slashing paid advertising spend, which will hurt new subscriptions. Good for profit (in theory). Bad for sales, though.

It’ll create an interesting investor relations dynamic for the Peloton team.

Peloton has been sold entirely as a growth story before now: “Hey, sure our fixed costs are huge, but just look at our subscription contribution margin. As we grow, that’s going straight to the bottom line.”

As the numbers show, it’s not worked that way. It will be fascinating to see how they position this with Wall Street.

Gross margin

As we dive in, two very different gross margin stories emerge:

Subscriptions: Rock solid 67-68% gross margins

Equipment: A rollercoaster from 43% pre-COVID to serious negative territory and back to 9% in the most recent quarter (FY25 Q1)

That 9% equipment margin is an improvement, but nowhere near the glory days of 43%. Those 34 percentage points are worth ~$300m of gross profit per year. That’s a hell of a gap to fill versus the unit economics that took the business public.

Sales & marketing expenses: The problem child

Sales and marketing costs have stayed stubbornly at 24-28% of revenue for most of the last five years.

But why haven’t they diluted more as revenue stabilizes and converts to recurring subscription revenue?

With the mix shift from equipment sales to subscription revenue, you would expect sales and marketing costs to dilute as a % of sales. Unless new customers are becoming more expensive to acquire (more on this later).

Peloton closed more than half their showrooms. So why aren’t we seeing those savings in the P&L? Presumably they’ve been reinvested in paid media advertising to capture those sales online.

There has been a change in trend of late, though. In Q1’25, sales and marketing spend is down to 14%. Peloton has slashed paid media spend. It will make them more profitable, but how will they get back to growth?

The $300M R&D mystery

Something doesn't add up in Peloton’s R&D spending. Here's why:

Peloton is spending $300m a year on R&D. That’s over 10% of sales. But on what?

Core bike/tread products have barely changed in 5 years

New products (Row, Guide) haven't moved the needle on margins or sales

Software updates like Netflix integration are nice, but $300M nice?

In 2020, R&D was $89M. Today it's $305M. That's an extra $875M spent over four years. So what improvements in the Peloton product have there been to merit this spend?

For that level of spend you would expect new breakthrough technology that supercharges either growth or margins.

But it hasn’t happened - the core offer of the business is much the same as it was four years ago.

So the question it begs is, is this really true R&D spend? Maybe this is where content costs and other platform integration costs live. Peloton's star instructors can earn $1M+ annually, and the content is the magic that keeps subscribers hooked.

But if that’s right, then content costs should be in COGS, not R&D. The content is literally what subscribers are paying for. Hiding it in R&D inflates subscription margins.

And if it isn’t that, then we come back full circle. What the hell are they spending $300m a year on?

Ever notice how companies report similar costs in different buckets? Here's why: while auditors will obsess over headline revenue and profit numbers, they rarely challenge whether a cost is in the right bucket between R&D, Sales & Marketing, or even COGS. This makes it hard to be conclusive on what costs sit where from the public filings alone. It also makes it hard to compare companies at a P&L line level (especially gross margin).

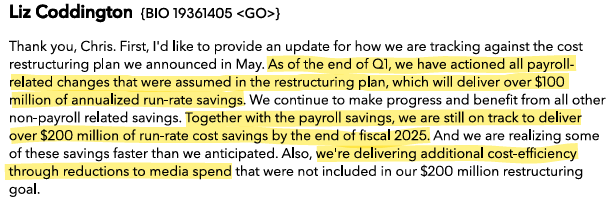

More restructuring

The good news is that Peloton is having success restructuring the cost base. Here is an extract from last week’s earnings call:

Extract from Peloton CFO Elizabeth Coddington, Q1'25 earnings call

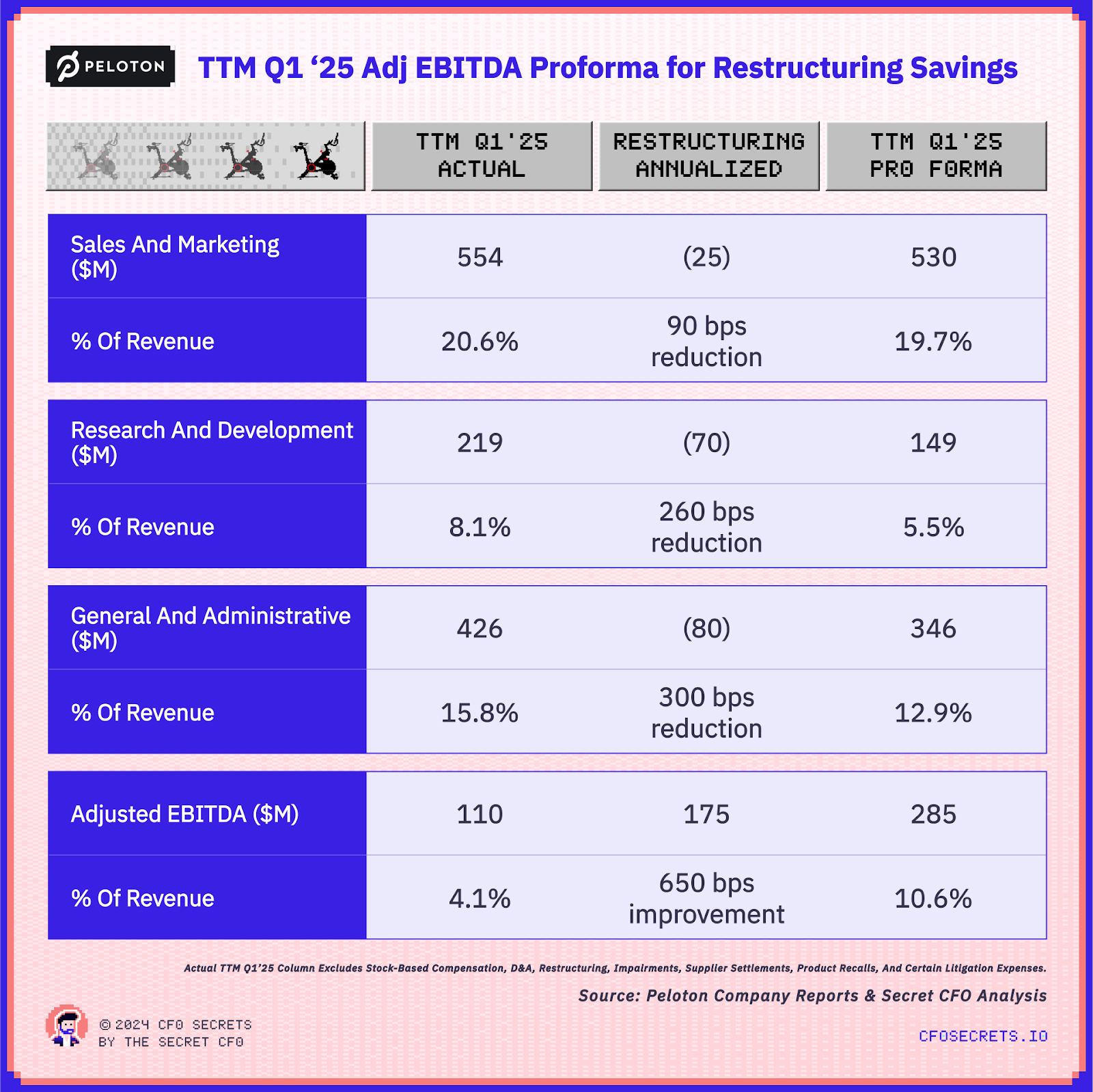

What happens if we extrapolate those savings onto the TTM Q1 ‘25 cost structure? An impressive further ~ 650 basis points of profit margin improvement:

A single restructuring plan having a 6.5 percentage point improvement effect on profit margins? That’s good news. Is Peloton finally getting on top of its cost base?

Let’s dive deeper into what is happening in fixed costs…

General & administrative expenses: Real savings or just less drama?

G&A costs have dropped by over 30% since FY22, and will likely fall by 10-15% again this year. The latest quarter shows GAAP G&A at $120M, down 21% year-over-year.

But why?

Some is real: Restructuring and headcount cuts

Some is normalization: Fewer legal settlements and write-downs vs the chaos period

That's progress, but the real test is whether they can keep the soap operas at bay. There have been A LOT of legal settlements and product recalls over several years. So many, that you’d argue they’ve become a cost of doing business for Peloton.

There are lots of tricky parts about the Peloton story. But costs are not tricky. This business desperately needs to right-size the cost base aggressively and as quickly as possible.

Reflecting on many years of turnarounds, I've never once thought "damn, we cut too deep, too fast." But I've lost count of the times I've muttered: "We should have cut harder, sooner." Yes, deep cuts hurt. Yes, they're unpopular. But you know what's worse? Drip-feeding bad news every quarter.

Death by a thousand cuts destroys morale and delays the recovery. The sooner you right-size, the sooner you can start talking about growth again. Sometimes you have to burn the field to restore the soil for new crops.

Adjusted operating income: A profit plot twist?

The P&L has been on a wild ride. Even using a generous definition of Adjusted Operating Income (adding back impairments, restructuring, and one-off supplier settlements):

FY20: $(80M) loss; (4)% of sales)

FY22: $(1.6B) loss; (46)% of sales)

FY24: $(408M) loss; (10)% of sales

‘25 Q1: $44m profit; 8% of sales

Credit to management for getting this business back into positive Adjusted Operating Profit territory. It’s only one quarter, but it’s a start.

Sales and marketing costs were down 44%, which drove the improvement in profitability. Consequently, revenue and subscribers were down. While it’s better for cashflow in the short term, it’s a damning sign on unit economics.

Right now, the best way for Peloton to improve its bottom line is to shrink, rather than to sell more. Let’s see what’s going on.

Unit economics: Following the money

Remember the razor/blade model from last week? Sell bikes at cost, then profit on subscriptions.

Great in theory. Let's pressure test it and look at the equipment P&L and subscription P&L separately.

Our approach, keeping it simple:

Equipment business (Connected Fitness Products) bears all sales & marketing costs (saving arbitrary cost allocations)

Subscription business bears all R&D and G&A

New subscriber adds as proxy for core equipment sales (Peloton doesn't disclose actual units)

Now for the fun part...

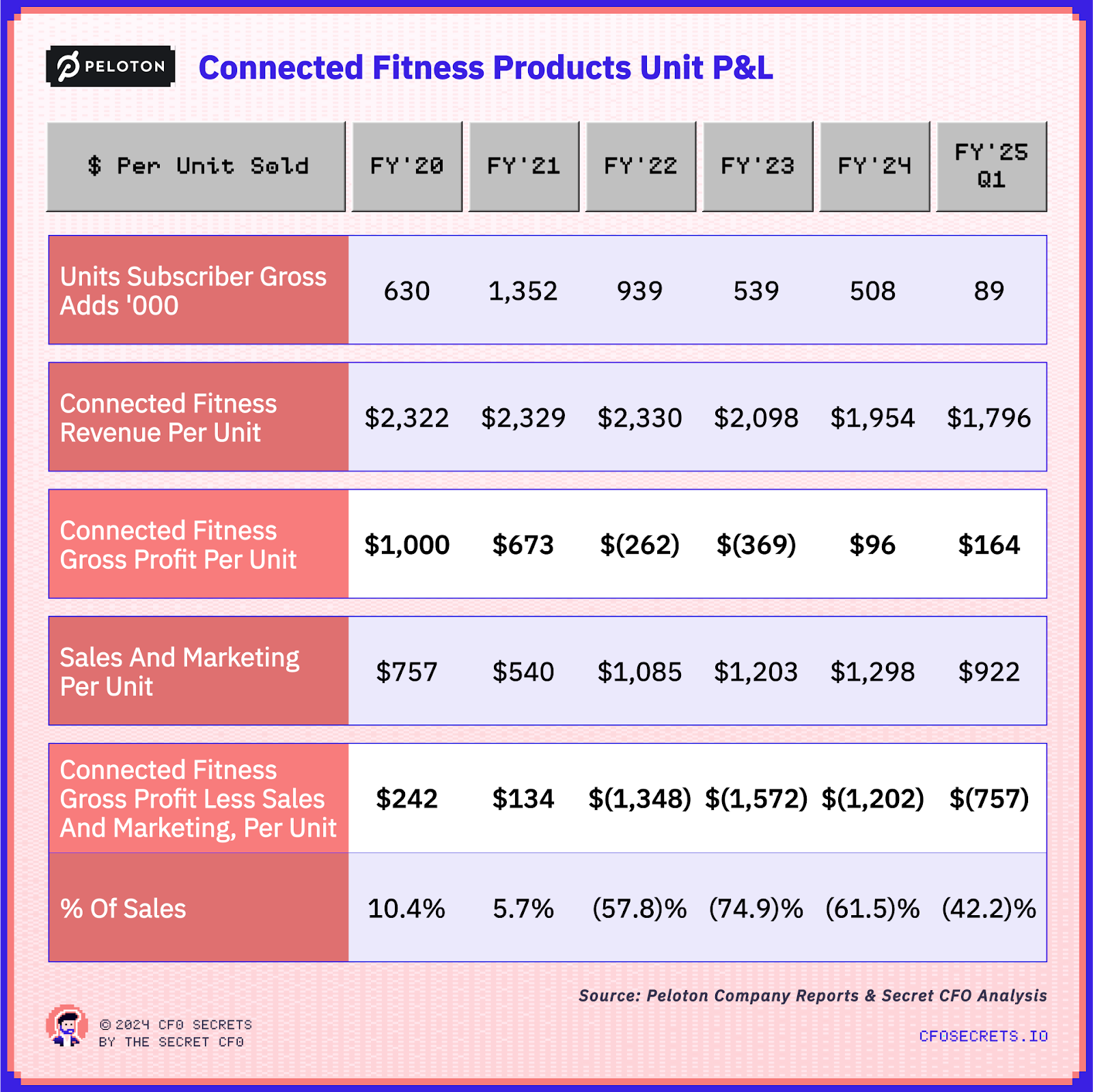

Connected Fitness Product unit economics

Peloton loses their Spandex bike shirt to the tune of $1,202 on each new customer sale, in FY ‘24. But it hasn’t always been that way. Back in FY20, and even FY21 they were clearing enough gross profit on each new subscriber sale to cover the cost of customer acquisition. That was a winning model.

So what has changed?

Customer acquisition costs have increased. Some one-time pandemic benefits were offset by paid digital media getting more expensive.

Average COGS per unit has increased by 40% (even ignoring the supply chain chaos of FY22). There will be some product mix effects in there, but I’ll bet most of that is inflation.

Average revenue per unit has fallen 16% in the last four years. In 2020 the Bike was priced at $1,895, today it is priced at $1,445. And the Bike + is still retailing at $2,495, the same price upon launch in 2020.

So Peloton is facing a brutal reality. $2,000 bikes are harder to sell today than they were four years ago. Yet, thanks to inflation and growing paid media costs, to restore the unit economics of FY20, they would need to increase prices by 30-50% ($700-$1,000).

That would crush demand.

Unless… the subscription business can cover the shortfall.

Let’s take a look at that.

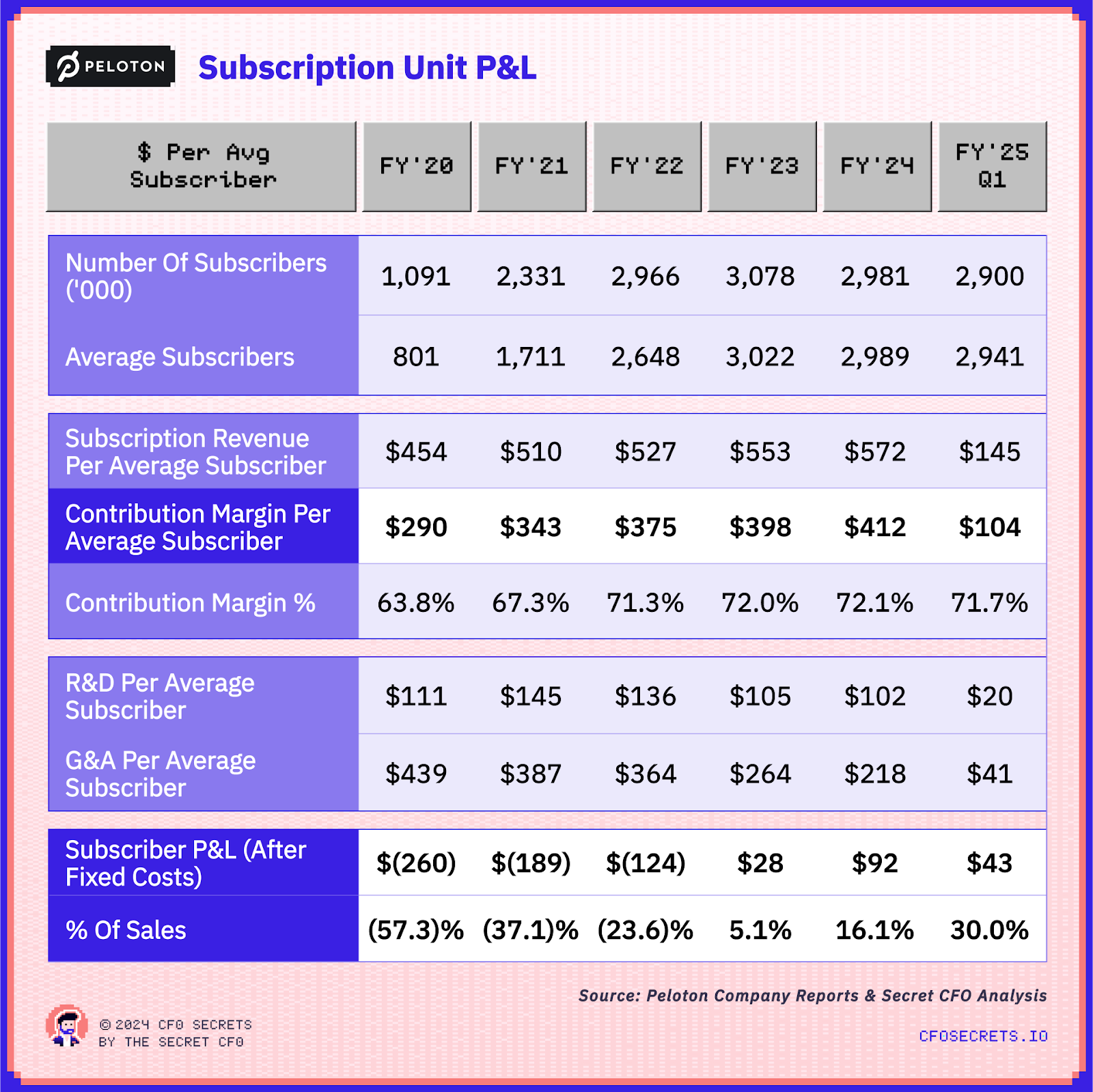

Subscription economics: The silver lining?

The subscription story looks better:

Stable 72% contribution margin since FY22 price hike to $44 per month

Fixed costs per sub falling (though not as fast as they should with more aggressive cost savings)

Each subscriber now worth $92 per year after all costs (except the upfront losses made on each new customer).

Finally, some good news? Not quite.

The math only works if they can:

Keep subscribers from churning (more on that next)

Solve the equipment sales nightmare we just saw

In other words: Great subscription economics don't matter if they're losing money getting bikes into homes.

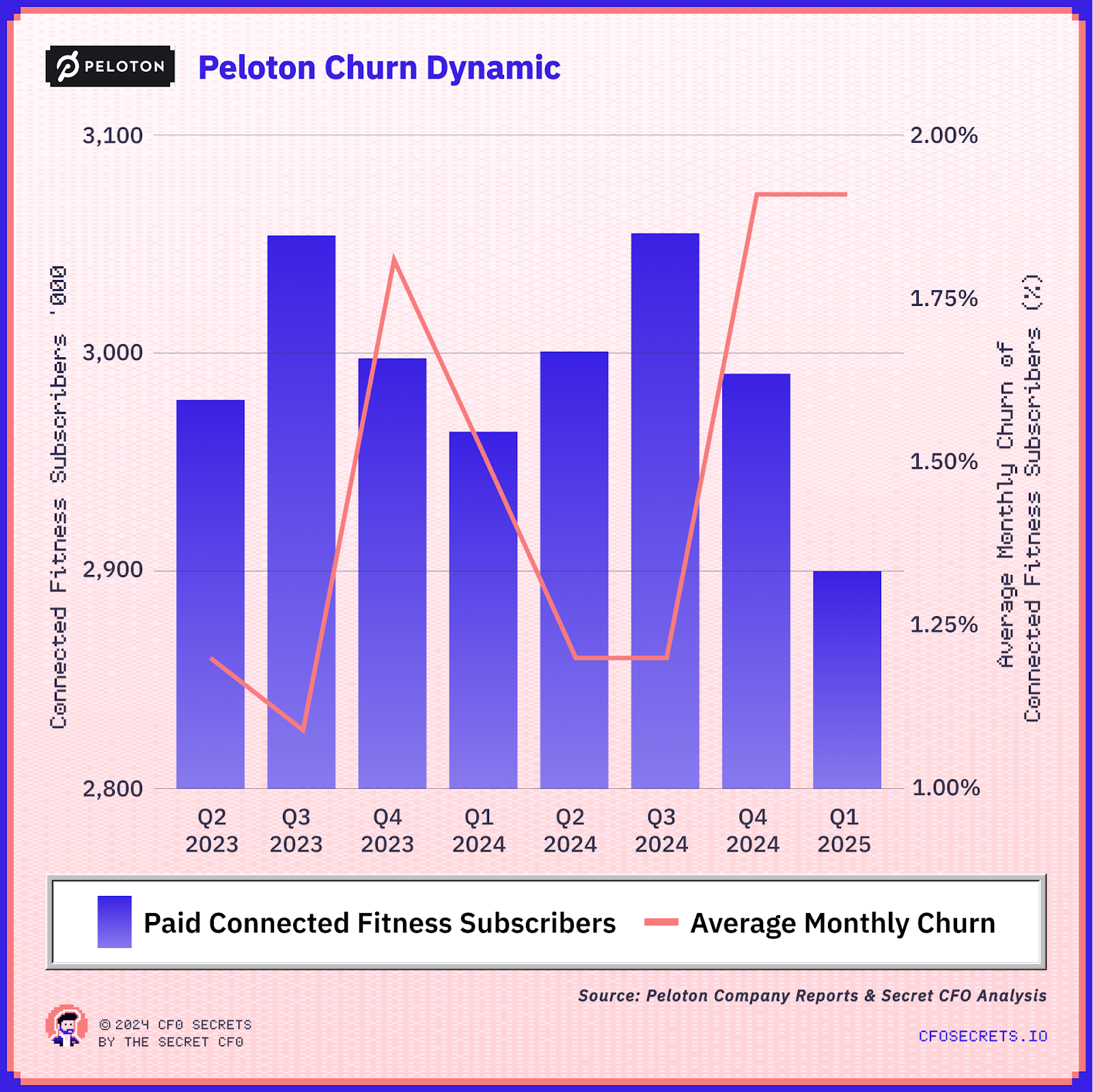

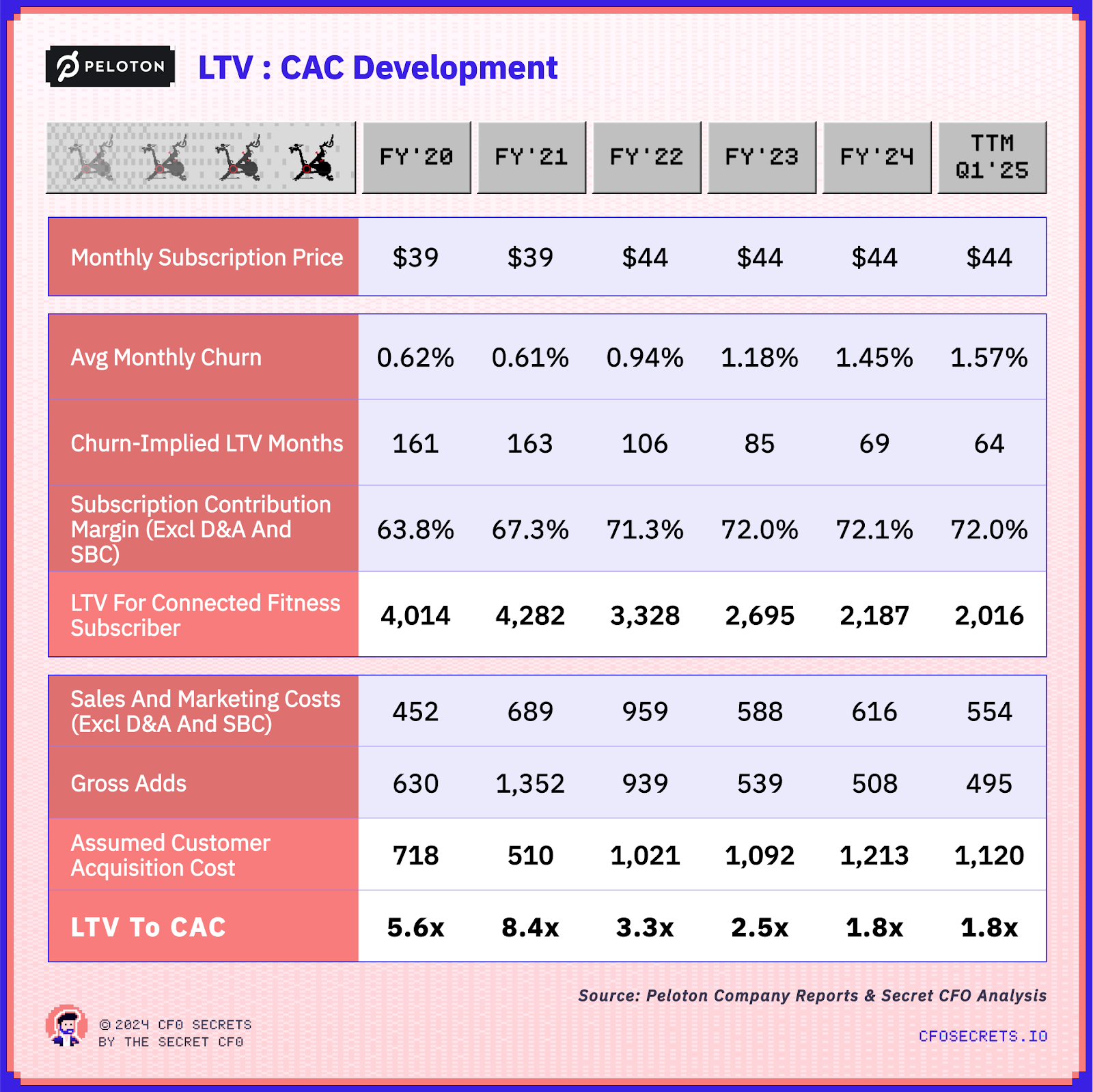

Subscriber churn

Churn levels of valuable $44 per month connected fitness subscribers are growing at a pretty alarming pace:

This is not hugely surprising. That surge of sales during the pandemic was 3–4 years ago now. So that cohort of new sales has aged. And with it comes a higher risk of churn.

1.9% of average monthly churn is still impressively low for a consumer subscription business, but higher churn does unquestionably change the economics of a new subscriber for Peloton.

The good news: Even with rising churn (0.61% → 1.57% in FY24), customers still stick around for 5+ years. That's impressive.

The bad news: In FY21: Each customer was worth 5.6x their acquisition cost, and today that has fallen to 1.8x.

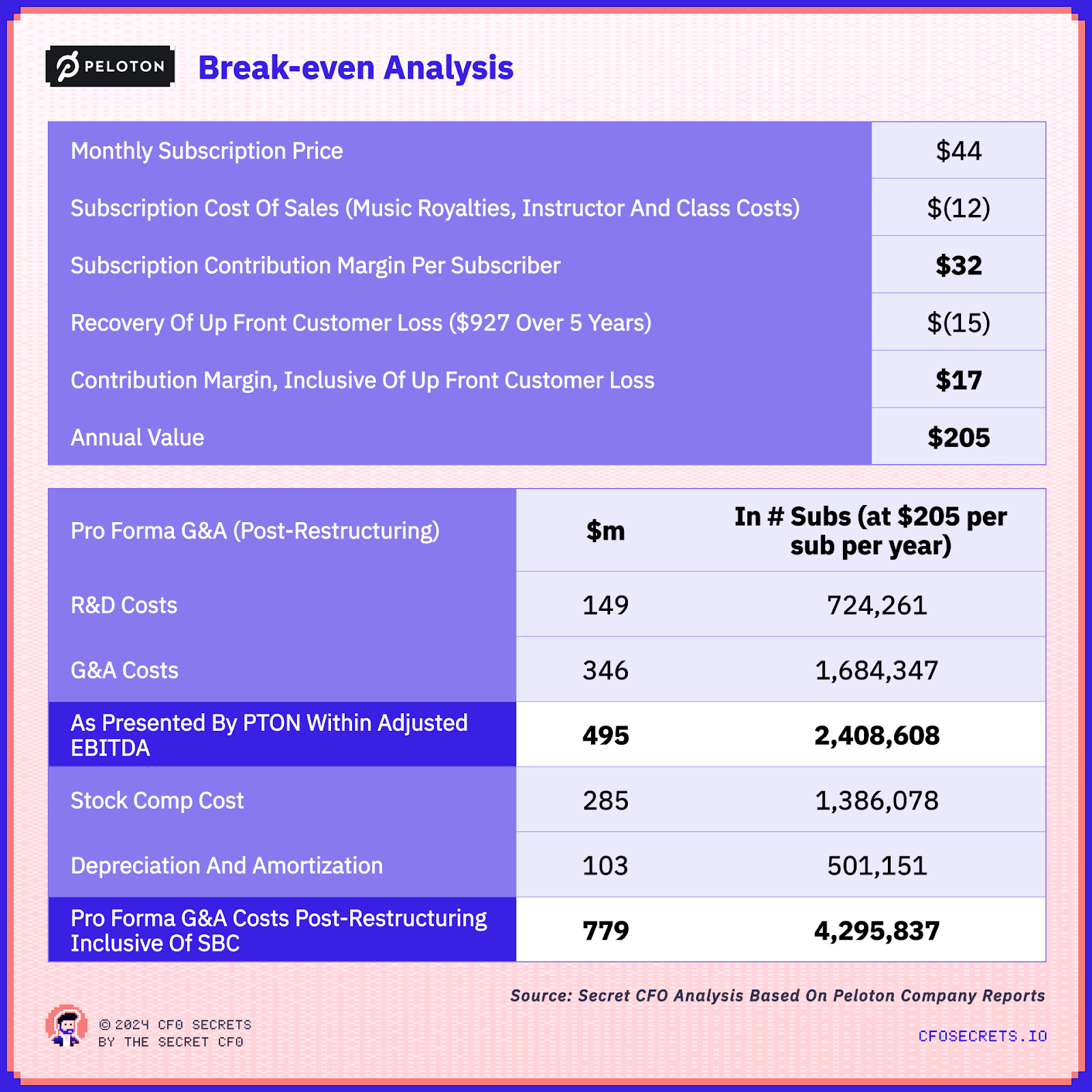

So where does all this leave us?

Of the $44 of monthly subscription revenue, $12 is needed for variable costs (technology, music licenses, some content costs, etc). The model was built on the rest of that $32 contributing to fixed costs, and ultimately delivering cashflow returns.

But with an average upfront loss per customer of $927 in FY24; $15 per month of that subscription margin is needed to amortize that cost (assuming a 5-year customer lifetime).

That means only $17 is available to contribute to the fixed costs of the business (R&D, G&A, Depreciation, etc.).

And while they can break even to their generously defined Adjusted EBITDA on 2.5m subscribers, that is assuming successful execution of the cost-saving program. The true breakeven point is likely far higher:

And on these economics, they will need 4.3m subscribers to reach real adult breakeven (after accounting for stock-based compensation, depreciation, etc).

That is out of reach currently.

The brutal math is that Peloton has to reset its unit economics:

Rip out as much fixed cost as they can. More and sooner to bring the breakeven point down.

Find cheaper routes to market. They need to cut their customer acquisition cost by at least 50% to improve contribution to fixed costs.

Deliver this all while increasing prices either on the upfront equipment or through the subscription price

This will take real commercial and operational skill to execute without crushing demand. New CEO Peter Stern has his work cut out.

Subscriber numbers are expected to fall from 3m to 2.75m during FY25. That alone will mean ~$100m less contribution margin than FY24. Peloton is betting that they can strip cost out faster than that.

That will help cashflow, but at some point, they are going to have to work out how to grow efficiently again. They will not shrink to glory.

One thing is for sure. This is a business that hasn’t figured out its unit economics at scale. And now it is doing so in the glare of the public markets. Not ideal.

And we haven’t even talked about the cashflow impact of all this, which is a whole different bucket of fun. Including that GLORIOUS Adjusted EBITDA bridge.

That’s next week.

Follow the money through the business. It never lies

Distribution is everything. If you can’t get your product to market efficiently it will hurt.

Understand how your unit economics will scale, before you scale. You can’t put the toothpaste back in the tube.

And Finally

No Q&A or anecdote this week … the email size was too big! Don’t worry they’ll be back soon.

Get your side hustle on. Are you a fractional CFO, or a finance professional interested in picking up part-time advisory work? We're launching a platform to help match you with SMBs looking for exceptional talent. Apply now

Find amazing accounting talent in places like the Philippines and Latin America in partnership with OnlyExperts (20% off for CFO Secrets readers)

Thank you to today’s sponsor, Brex…

Any controllers reading? Get the blueprint for automating compliance with NetSuite + Brex.

Next week we’ll dive into Peloton’s cashflow. If you follow the Peloton business, or read the 10-K, and have any thoughts, I’d love to hear them. You can send them straight to me by just hitting reply…

Stay crispy,

The Secret CFO

Was this email forwarded to you? You can subscribe by clicking the button below:

Disclaimer: I am not your accountant, investment advisor, tax advisor, lawyer, CFO, director, or friend. Well, maybe I’m your friend, but I am not any of those other things. Everything I publish represents my opinions only, not advice. And certainly is not investment advice. Running the finances for a company is serious business, and you should take the proper advice you need.

What did you think of this week’s edition?