Are you still reconciling bank and payment processors manually? Ledge automates it.

Ledge automates reconciliation and journal entry prep across all your accounts – banks, PSPs billing systems, data warehouses, you name it – and syncs it back to your ERP in real-time. Scale complex, high-volume reconciliation without having to scale headcount.

With pre-built integrations to 12K+ institutions, Ledge has all the power of a custom reconciliation solution with none of the heavy lifting – no R&D or IT help required.

Common sense

“It’s… ya know… a regular WACC calc, and it comes up with the answer 11.3%.”

I don’t like it when people talk about an Excel spreadsheet like a sentient being. Like it’s somehow making decisions to get to the answer.

I’ve always had a good nose for when to dig into the details behind a calculation.

But I didn’t need it here. It was glaringly obvious there was a problem.

Too many poor quality capexs had been approved. Justified by being Net Present Value (NPV) positive.

After the debacle with Nathan, I’d asked Paul - my treasurer - to take me through the Weighted Average Cost of Capital (WACC) calculation.

This WACC was being used as the discount rate in the NPV calculation.

As Paul talked me through the details - to my surprise - it was well put together and clearly laid out.

The cost of equity had been calculated using a Beta of thoughtful comparable companies. The cost of debt was based on the interest coupon at the last debt raise. The weightings applied were reasonable too.

All by the book.

It was actually a perfect application of the cost of capital theory.

It was just missing one thing…

COMMON SENSE.

The reality…

This business was breaking under the weight of an unmanageable debt burden.

It had burned $100m of free cash in the last year.

And now we were borrowing mezzanine debt to keep the business alive at an interest rate of over 20%.

In that context, a WACC of 11.3% was complete nonsense.

The marginal cost of debt was nearly double the stated WACC.

Time for common sense to overrule corporate finance theory.

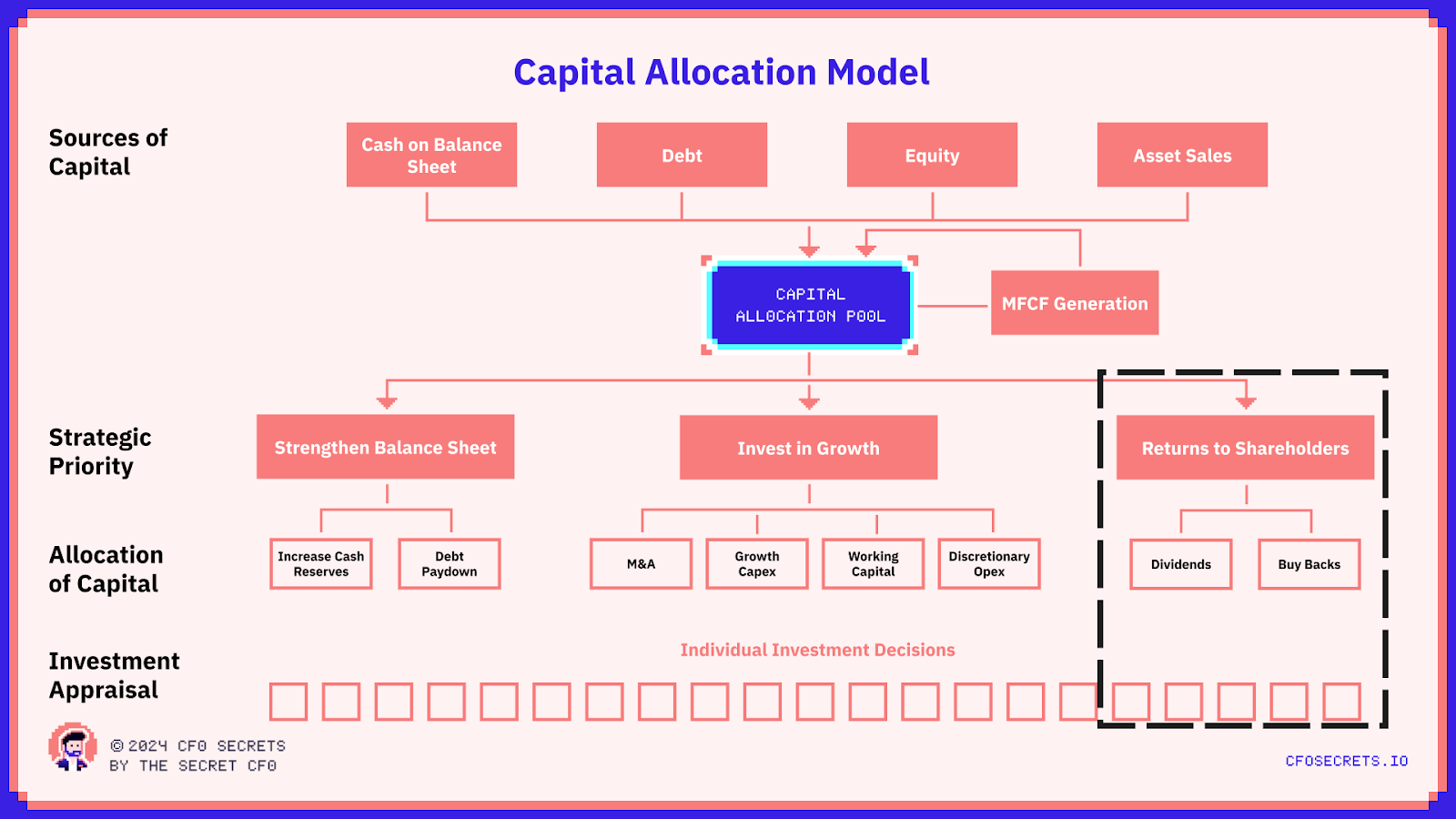

This is the third part of a four-part series on corporate capital allocation. See the second post here.

WACC is wack (and other corporate finance sins)

Last week we looked at how businesses fund their growth.

And how they choose between growth investments; R&D, Capex, M&A, etc.

This week we look at how and when to allocate capital back to shareholders:

As a reminder: surplus capital should be returned to shareholders. Unless there is a compelling reason not to.

That ‘reason’ needs to be that the company can improve shareholder returns by allocating it to investments.

But how do you quantify this?

Well, this is what the textbooks say…

Every finance undergrad or business school course in the world will show you this chart:

I’m not going to cover cost of capital theory in detail. Partly because I can’t remember it all. And secondly, because it is probably the most documented topic in finance. So there isn’t really anything more for me to add. I will drop a couple of links below to more in-depth theory if you want a recap.

IRR = Internal Rate of Return (primer). Which is the time-adjusted return on investment expressed in %.

WACC = Weighted Average Cost of Capital (primer). Which is the opportunity cost of employing capital.

Purist corporate finance theory says if IRR > WACC then make the investment. If IRR < WACC then don’t.

Put another way, If you can achieve a return on capital that exceeds the cost of that capital, you should invest. If not, you should not invest. And if there are no alternatives, that capital should be returned to shareholders.

This is nice in theory. But that’s all it is… a nice theory.

Here are the problems with it:

Return estimates are only a forecast. Riddled with inaccuracies and execution risk. Not to mention biases.

Return estimates are not absolute, they have probability distributions. As we discovered last week. IRR works on absolutes

IRR ignores $ values and relative sizing of investments

WACC is impossible to measure in practice. Just ends up a meaningless Excel salad of assumptions that mean nothing to anyone. Other than the nerds in treasury - see the opening anecdote

You can circumvent the issues with IRR, with good finance business partnering. And by using IRR as part of a suite of metrics.

But the weakness in WACC as a practical tool is inherent in its definition.

It assumes companies have a limitless availability of capital at the defined WACC in any practical sense.

This is, of course, not true in any practical sense.

Capital is constrained.

And capital won’t be available on a menu in the way WACC assumes. You will have a handful of discrete options for raising the capital you need at specific rates.

So if WACC is wack… what is the alternative? Well, most projects would never be funded at the weighted average rate. They’d be funded at a marginal cost of capital i.e. if you have $1bn of capital employed, and want to raise $100m to invest. For that individual project, it is the cost of the $100m of capital that matters. Not the weighted average cost of the $1bn or even $1.1bn.

So when I need a discount rate for NPV analysis, I prefer to use the HIGHER of:

Marginal cost of capital (often SOFR + a margin)

WACC on a post-capital raise basis

Let's head back to the original example. A business with a WACC of 11.3% and a marginal cost of funds of 20%, should not be discounting projected cashflows at 11.3%. It should have been discounting at 20%.

You guys loved my graph last week, so I made you another one:

This is a profile for an example company, you can see how it’s easy to get carried away justifying marginal investments using WACC as a discount rate. Even if the marginal cost of funds explodes.

A good CFO will be trying to solve for the lowest blended cost of capital, but not at all costs. Increasing the cost of capital (i.e. by raising more expensive money) can be, and is often, the right thing to do. Especially if you are confident in the return business case of the use of that capital.

But that judgment is a fine one (art not science) and must be in the context of the strategy.

Let’s overlay a practical example.

Surely we can learn from the best?

Well, turns out they don’t always get it right either.

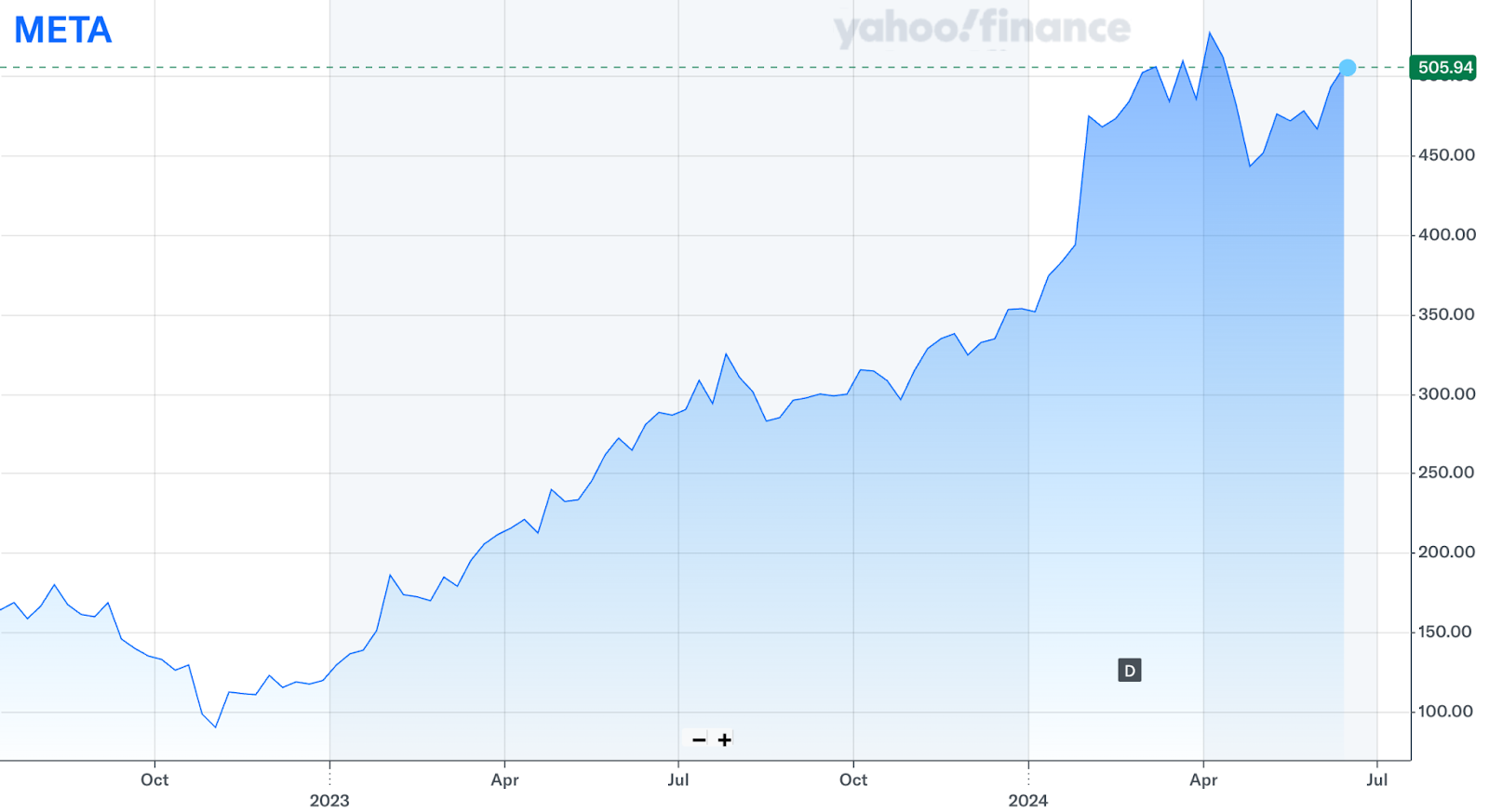

Let’s look at Meta.

In late 2022 they announced intentions for huge investments into VR and the metaverse. At the time, Chamath Palihapitiya called it the largest corporate capital allocation decision in history.

The market hated it. HATED IT. The stock fell from $130 to $90 in less than two weeks.

It’s easy to laugh now, but this was 2022, and the metaverse (whatever that is) was hot sh*t. And Zuck was prepared to bet the future of the company on it.

But more than that. He was also gambling shareholders' capital on it.

Meta is not a plucky venture-backed start-up anymore. For shareholders, it's a cashflow juggernaut. Shareholders expected a good share of cash generated from the core business would be returned to them.

And Zuck had just told them he was going to gamble it all on cartoon characters with no legs …

Source: Meta

Zuck is a genius, and I am not. So maybe he’s right. Maybe his vision is the future, and this is the lever that takes Meta to a $20tn company by 2035.

But shareholders (rightly) felt robbed of their agency.

Now, the irony is, that this ended up being overblown. Coincidentally, the same week the Meta news hit the market, Elon Musk closed on Twitter.

And in doing so ripped 90% of the headcount out of the business. This exposed how many discretionary expenses these businesses were carrying.

The other tech giants followed.

Zuck completely (and quietly) reversed the Metaverse investment decision, just a few weeks later.

Meta went on its own Elon-esque headcount cull, cutting roles like this.

@durbinmalonster Every one of my coworkers watching this I hope you’re happy

Meta’s stock ripped 5x in less than 18 months. Market cap grew by $1tn.

The Metaverse mega investment came and went quickly.

So how does this link to theory?

The guys and girls at Meta are not dumb. They will have done the math on the metaverse. But my guess is they hugely underestimated their equity cost of capital.

Their investor base would require a much higher return to accept their sweet reliable Instagram ad dollars being re-invested in the Metaverse (vs those same dollars being paid as dividends.)

Investors ultimately felt that if they were going to invest in the Metaverse, THEY wanted to make that decision, through their own portfolio. They didn’t want that decision made for them.

Especially not at the expense of dividends. An emerging tech investment is much more like a venture-backed investment. A totally different class of investors to those expecting an annual cash yield.

While the stock rallied after the U-turn, plenty of institutions sold out at $90 and:

Lost a fortune

Missed out on the bull rally that followed

So how do you combat this?

As CFO you must… I repeat MUST… understand the composition of your shareholders. What they expect, and what their own limitations are. Most institutional fund managers are operating within their own guardrails. Whether that be credit ratings, dividend policy, leverage levels, ESG strategy, etc.

If something in your business changes that goes against their investment thesis (or fund rules), they could become a forced seller.

I think the Meta example demonstrated a poor understanding of their shareholder mix. And maybe even that they’d lost touch with who their investors were.

But these are smart people, credit to them for realizing the mistake quickly and correcting it.

Buybacks vs Dividends

So once you have decided it’s time to return money to shareholders, how do you do it?

There are two main options:

Dividends

If a business is producing more profits and cash than it is able to sensibly reinvest, then it would be paid as a dividend.

Typically, you would set some level of guardrails on post-tax profits. For example, your financial policy could say that your dividend payout ratio of post-tax profits will be somewhere between 20%-50%. Targeting 50% but never lower than 20%.

This ratio will depend on the reinvestment opportunities (see last week), and shareholder expectations.

You can move the guardrails and dividend guidance, but good management teams do this in a controlled and well-communicated way.

Share Buybacks

Alternatively, a business can use surplus cash to repurchase its own shares.

Share buybacks tend to be one-offs or a series of one-off transactions. They are attractive to companies because they give the company flexibility on timing and size.

So if, for example, an irresistible, large, M&A opportunity had arisen for Apple, during their unprecedented buyback program, they could have stopped and reallocated capital to M&A at any time.

Dividends vs Buybacks

The appropriateness of dividends vs buybacks depends on the following:

Stock Price vs Intrinsic Value

Tax Treatment

Strategy

Shareholder Expectations

For example, an increased dividend payout ratio will:

Please some shareholders; more cash sooner

Disappoint others; reduced reinvestment opportunities inside the business (lower confidence in future)

Whereas buybacks are considered to be more opportunistic. The company will use spare cash to repurchase shares when it makes sense. Shareholders will be more accepting of ‘lumpiness’ in buybacks vs dividends.

Tax is in play too. Dividends tend to be taxed as income (on shareholders) and buybacks are taxed as a capital gain. In most jurisdictions, buybacks are more tax-favorable for shareholders. But not everywhere/always.

Shareholders looking for long-term capital growth love buybacks. When a company offers a buyback, shareholders have two options:

Sell their shares at the quoted price

Hold their shares

If any one shareholder believes that the quoted price represents above market value for the shares, they would sell. And in turn, be happy with their lot.

And the shareholders who choose to hold their shares will be even happier. The company has just been able to buy back shares at a price that is less than they think those shares are truly worth. This creates value for the remaining shareholders.

This pushes the share price up in the long run.

I call this Buffett thinking. As an investor, Buffett says you must understand the ‘intrinsic value’ of a business. Then buy that stock where it is available at a price that is a suitable discount to that intrinsic value.

Samesies for a CFO with their own stock.

If your stock is undervalued vs its intrinsic price - it’s a great time to buy back. If your stock is overvalued vs intrinsic price, it’s a great time to raise equity (cheap capital). Or, to use your stock as consideration for an M&A opportunity (cheap currency).

Arbitraging your own stock price is a smart way for CFOs to create shareholder value for long-term shareholders.

So the obvious question… how do I know what my intrinsic price is?

Intrinsic Value

Intrinsic Value = the Net Present Value of your future cashflows.

And as CFO you are uniquely placed (vs investors). You have the inside track on forecasts, strategy, and investment opportunities.

You can use different scenarios from your Long Range Planning Process to form an informed intrinsic value.

I like to have my VP of Corporate Finance update our intrinsic value model quarterly. Usually, a light touch based on the latest performance vs a full review on an annual basis.

Those are the fundamentals for returning capital to shareholders.

Next week we will explore strengthening the balance sheet and bring this series together by working through how you apply this practically and turn it into a plan for your own business.

WACC is too technical for most purposes. Make sure you understand your marginal cost of capital

Maintain an Intrinsic Value model to help make better corporate finance decisions

Know your investors. Different investors want different things. Dividends, buybacks, reinvestment, high leverage, low leverage. No (negative) surprises.

Alex from London, UK asked:

Hi Secret. Firstly, thank you for the great blog. I'm a Big 4 Management Consultant focused on shaping and delivering enterprise transformations. This work naturally sees me working with CFOs, and your blog has helped me better understand the CFO role. I think I'm becoming more impactful in my interactions.

My question is about the role CFOs play in strategy. Another blogger I admire is Roger Martin, and he recently posted a piece on this. I'd be fascinated to know what does and doesn't resonate for you, particularly his call for CFOs to "master Strategic Economics."

I don’t often like much I read on the CFO role (it’s why I started writing myself), but this was a really interesting piece. Thank you for sharing this, Alex.

I am in two minds on it

I absolutely agree that the CFO needs to be the guardian of long term strategic economics. That is where real long-term shareholder value is created. Imagine if the Apple CFO of 2006 had insisted on distributing all discretionary profit as dividends rather than doubling down into the iPhone…

However, the business also needs someone holding them to account in the micro. If the CFO isn’t the ‘no’ force, then who is? Without that balance, you can end up with WeWork 2018.

The skill and the judgment is in assessing whether you are approving investment into an Apple iPhone or an Apple Newton.

This is ultimately about capital allocation. The topic du jour. If expenditure of all types can be split between a) costs of doing business, and b) investments into the future. Then we should be trying to be as lean as possible on (a). No exceptions. That maximizes resources available for (b). Then (b) is just about choices; invest in R&D or marketing; M&A or dividends, etc. And the CFO should set the framework for those decisions, as we discussed in this series. They MUST have long-term economics in mind when making those decisions. And link it to the strategy, of course.

It all comes back to the chief role of the CFO to be maximizing long-term maintainable free cash flow per share.

With that north star, you can’t go too far wrong

If you would like to submit a question, please fill out this form.

And Finally

Next week, we will bring this series home with a practical framework for allocating capital.

If you enjoyed today’s content, don’t forget to check out this week’s sponsor Ledge.

Stay crispy,

The Secret CFO

Disclaimer: I am not your accountant, investment advisor, tax advisor, lawyer, CFO, director, or friend. Well, maybe I’m your friend, but I am not any of those other things. Everything I publish represents my opinions only, not advice. And certainly is not investment advice. Running the finances for a company is serious business, and you should take the proper advice you need.

What did you think of this week’s edition?