Capital allocation is art AND science. But it’s hard to find time for strategic things without automating those time-sucking tasks. Meet Ledge…

"Time is money. Ledge saves us both. We can now reconcile instantly, freeing our team for higher-value tasks."

– Liran Daudi, Director of Finance at Papaya Global

Struggling with reconciliation? Ledge automates it across all your accounts – banks, PSPs billing systems, data warehouses, and more – and syncs it back to your ERP in real time. Scale complex, high-volume reconciliation without having to scale headcount.

With pre-built integrations to 12K+ institutions, Ledge has all the power of a custom reconciliation solution with none of the heavy lifting – no R&D or IT help required.

Book a demo to learn more about Ledge.

Sh*tty situation

"Yep, you are right. This particular turd has your name on it."

This is why Adam was a great mentor... he always told me how it was.

Whenever something goes wrong I always ask myself the same question; “what could I have done differently to stop this?”

It's how I keep sharp.

In this particular case, we'd recapitalized the balance sheet less than 12 months ago.

And here we were less than a year later. Forced to raise more capital to keep the business liquid.

And it was expensive money...

Certainly sounds like a CFO f*ck up.

And there was no question that with hindsight we'd undercapitalized the balance sheet a year earlier. But over-capitalization is a mistake too. Capital has a cost (as we learned last week).

I tend to plan balance sheet liquidity to a 95% confidence level over the next 18 months i.e. I can live with the risk that once every 20 years I will need to find emergency capital. Providing I have an open channel for accessing that capital if needed.

So once the issue had been resolved (at a cost), and the dust had settled, I was here now with Adam. Asking the question, “Was this a true 1 in 20 years? Or should I have seen it coming?”

The issues that caused the cash shortfall had been an unfortunate cocktail of operational and commercial issues:

Big customer loss

Supply chain issues

A breakout movement in input costs

I was confident I had planned adequately for one or two of these things happening. But not more.

The question was, should I have?

Adam’s view was clear: “Yes.”

The issues the business had seen were not mutually exclusive. The likelihood that we had ended up with this particular melting pot of sh*t had been far more probable than I had thought.

Adam's view was that I'd underestimated the compound effect of the risks. Once the first 1 in 10 event occurred (material price hike) the probability of that snowballing into a much bigger issue was bigger than I’d assumed.

So, it's one I had to wear. We were able to find the liquidity easily enough, but at a much greater marginal cost of capital (over 5% more) than if I'd got it right a year ago.

You live and learn.

Are You Being Paid Enough?

This week I launched the first ever Secret CFO Compensation Survey. We have already had over 1,000 responses. It’s not too late to have your say.

This is the final part of a four-part series on corporate capital allocation.

Practical Capital Allocation for CFOs

In week 1 of this series, we covered what capital allocation means and the role of the financial policy.

In week 2 we covered how (and when) to reinvest capital to grow a business.

In week 3 we covered how (and when) to distribute capital to shareholders.

This week we will bring it all together in a practical framework.

But before we do… the eagle-eyed among you will note we have only covered 2 of the three types of capital allocation so far: investing in growth and distributions to shareholders.

Now let's cover the 3rd: strengthening the balance sheet.

And just because we've left it until last, doesn't mean it's the least important.

In fact, the opposite is true.

We have talked throughout this series about the trade-off between shareholders distributions and reinvestment for growth. But if the balance sheet needs strengthening, that takes priority.

Think of it like an athlete training for a marathon.

The result of the race itself is the end goal (shareholder distributions). And the training is the way of improving that result (investment in growth).

The more they train… the better the end result (as long as it is good training.)

But what if the athlete has a broken leg?

Then neither the training nor the race matter one bit. Until that leg is fixed. Think of the broken leg like a weak balance sheet. Resources have to be allocated to fixing it first.

Don’t run until you can walk.

Strengthening the balance sheet can come in two forms:

Increasing the level of cash held on the balance sheet

Reducing the level of debt on the balance sheet

Holding Cash vs Paying Down Debt

The choice between holding cash and paying down debt is one of flexibility vs cost. Cash is flexible, but holding cash has a cost.

You can always use that cash later to pay down debt if you want to. But once you’ve chosen to pay down debt, getting that cash back is harder. Unless it’s revolving debt, but that’s for another time.

So it’s a trade-off… but unlike most other cost of capital decisions, fortunately it’s simple to quantify.

You will earn interest on your cash at a rate (S) and pay interest on your debt of S + a spread (2% to 5% for good credits).

So ‘S’ nets off and you are left with the spread as the cost of holding cash vs paying down debt.

The extent to which you want to use debt in your business will depend on lots of things, but notably:

Shareholder risk appetite/expectations

Strategy and strength of investment opportunities

Cost of current debt

Cost of new debt

Expected shifts in interest rates

Lender appetite

Liquidity requirements

Leverage targets

Collateral requirements

Covenant expectations

We will run a separate series on raising debt and managing lenders in the future. For now, we will focus on the capital allocation considerations with debt and cash.

The key question here is when to prioritize debt reduction.

This is about finding the right balance of:

Keeping within financial policy guardrails on leverage/interest cover targets

Optimizing cost of capital

Ensuring the business has enough liquidity to operate properly

Ensuring the business has the capital it needs to execute on investment opportunities and its shareholder distribution program

Setting Cash & Liquidity Levels

There are many different methods you could use to define the right liquidity level for your business. Here are two I have explained before (but there are others):

18 months and 95% - what cash level do you need to fully fund a reasonable worst case forecast scenario

Armageddon survival buffer - Liquidity Headroom / Avg Daily Sales. i.e. How long can we survive if our customers stopped paying tomorrow.

Your financial policy needs to have a clear rule on the level of cash on hand that the business needs. This rule flexes as the forecasts and needs of the business (and the macro-environment) change.

I have approximately doubled my policy levels of liquidity vs 3 years ago.

There is so much more uncertainty around:

Record inflation levels

Rate hikes

Wars in Eastern Europe and the Middle East

I'm not a geopolitical analyst and never try to be. I find scenario planning for these sorts of things to be an utterly academic exercise. The best way for businesses to prepare for macro uncertainty (especially in an election year)? Bigger cash reserves. Ya know, just in case.

The bigger the cash balance, the bigger the force field. Just remember that a big force field costs more than a small one.

‘Amber’ & ‘Red’ Warning Zones

I also like to set both Amber and Red liquidity warning levels.

If our forecasts project that our liquidity levels fall below a red level, we pause all other capital allocations until that is resolved. 100% of capital gets allocated to strengthening the balance sheet. That means disappointing a lot of stakeholders (capex freezes, dividend freezes, etc). I don’t take this lightly.

In the event that we fall below the amber warning level, then we increase the level of cash retained in balance sheet, but in a partial/smoother way. Rather than a total stop on investments and distributions.

If your amber warning level is set in the right place, you should be able to steer the balance sheet back to green without shredding your long range plan (and strategy) with it.

Debt works the same way. You will have set guardrails for debt in your financial policy. This includes leverage levels, debt duration, interest cover, etc. Use amber and red warning levels to keep the business in a safe landing zone. And take increasingly drastic interventions as you trip the thresholds you have set.

Defining Liquidity

Liquidity = Cash + Undrawn credit facilities i.e. could be cash on balance sheet. Or it could be a flexible credit facility: revolving credit facility/overdraft etc. This is typically more capital efficient than just holding a big cash war chest. Just make sure you understand the covenants of that debt. No good having an insurance policy that doesn’t pay our when you need it.

Look Forward not Backward

One common mistake I see is finance teams measuring their conformance with finance policy on an actual/reported basis. But not on a prospective/forecast basis.

These are ‘survival tests.’ The history is irrelevant. The important question is whether the lion is going to eat you tonight, not whether or not it did last night.

You should use your Long Range Planning model to spot emerging issues. And if you spot a breach, take action now to steer the balance sheet to safety.

Being super thoughtful about your financial policy and reviewing it constantly is the name of the game here.

And with that… we've completed our tour of the different ways in which managers can allocate corporate capital.

But we still have to bring this together in a practical framework.

This is impossible to do comprehensively, as it will depend on your capital structure, growth ambitions, and risk appetite. But there is a series of steps and a thought process that should be applicable in most circumstances.

So to round the series off, here’s..

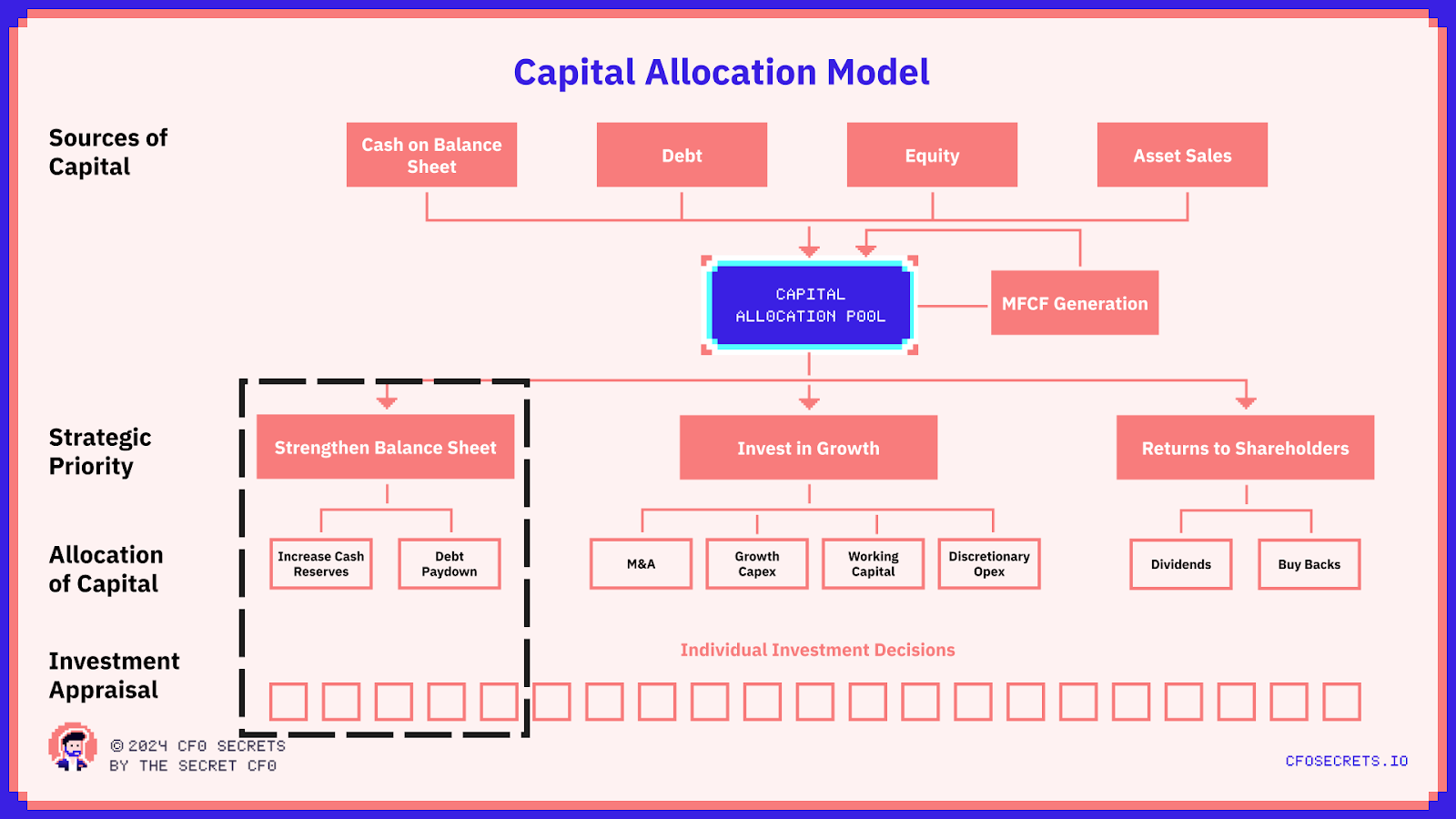

The Secret CFO Capital Allocation Framework:

1) Start with the strategy

Everything starts with what the business is trying to achieve, for whom, and why.

2) Long Range Planning scenarios

The strategy should drive the annual Long Range Planning cycle. Which should lead you to 2-4 different business/growth scenarios for your business. Once you have modeled those scenarios on both a base and a sh*t case, you have the base cashflow assumptions for your capital allocation framework.

3) Review financial policy

Based on the options in the Long Range Plan you should review the financial policy to ensure it still achieves the balance of executing the chosen strategy with satisfying stakeholders.

As described at the start of the series this will include setting the guardrails for dividend payout ratio, liquidity parameters, debt levels, etc.

4) Quantify available capital

Many get this wrong. How much capital are you actually allocating?

There are principally 3 sources:

Surplus cash on balance sheet

Generated maintainable free cashflow (accruing over time)

New capital raises (debt or equity)

Understanding how much capital you have to allocate, and when, is critical. Is it lumpy or does it accrue smoothly? All of this will influence your capital allocation framework.

5) Solve for liquidity first

The first 4 steps were all planning. Now we are into actually allocating capital.

The first allocation of capital should always go to securing adequate liquidity. Secure the balance sheet first. Without enough cash-on-hand, you won’t be able to execute the rest of your capital allocation strategy.

Your first priority is whatever liquidity requirement you set in your finance policy.

6) Debt paydown

And on the theme of strengthening the balance sheet, your second capital priority is to keep debt within the guardrails set in your finance policy.

It's no good paying a dividend or investing in a big capex project if you have to break your debt guardrails to do it.

7) Set investment hurdle rates

Once you have ensured the balance sheet is protected and the guardrails are set, you can get down to the serious business. Allocating capital to the fun stuff, like growth projects and shareholder distributions.

This is where you need to assess your discount rate for investments, investment metrics, and your hurdles.

IRR is the most common metric used to benchmark corporate projects. I like it as an investor, but not as a corporate allocator.

As I described in the second issue of this series my preferred metric for corporate capital allocation is NPV $ Per $ of Invested Capital. Ensure you have the right discount rate and hurdles on investments. That will make certain you prioritize properly between growth investments and returns to shareholders.

8) Evaluate opportunities & set priorities

Now you can set some overall capital budget guardrails. This will be based on the strength and depth of the projects and investment opportunities you have vs the hurdle rates. And in turn, lock the investments into the annual budget.

Note you are not (yet) approving the individual investments, but planning in principle which projects/budgets you intend to fund. And the resulting impact on shareholder distributions.

This, again, could mean revising your financial policy.

9) Manage stakeholders

By now you will have a clear idea of your plans (in aggregate) for capex, opex investment, debt levels, dividend expectations, etc.

You need to ensure that your stakeholders are aligned. Especially external stakeholders (shareholders and lenders).

With the previous 8 steps done, you have done enough to communicate your capital allocation plan with confidence.

As we said last week, don’t surprise these guys and girls. The art here is giving guidance that is narrow enough to be valuable and avoid investor speculation. But also wide enough to give yourself flexibility.

10) Execute investment appraisal

All of the first steps count for nothing if you get this one wrong. This is where you actually approve individual investments.

As we saw in the story that started this series, when you fail to appraise individual investments properly, none of the rest of it matters. You need a robust investment committee or capital allocation committee for appraising individual investments against the strategy and the return hurdles you have set.

It's not all about the numbers. And certainly, at an individual project level, it doesn't have to be. But as a whole, the numbers have to add up back to the original guardrails you set earlier.

This is where the art and judgment of capital allocation come in. It takes brains and guts as a CFO to approve a $5m speculative spend with no clear payback vs a $5m spend with a $2m hard payback. But there are circumstances where you should make that decision.

The more you understand your business, the easier those judgments are to make.

11) Post investment review

Once you have approved the individual investments, you need to ensure those projects actually deliver the returns. We’ll cover post-investment reviews in a future series.

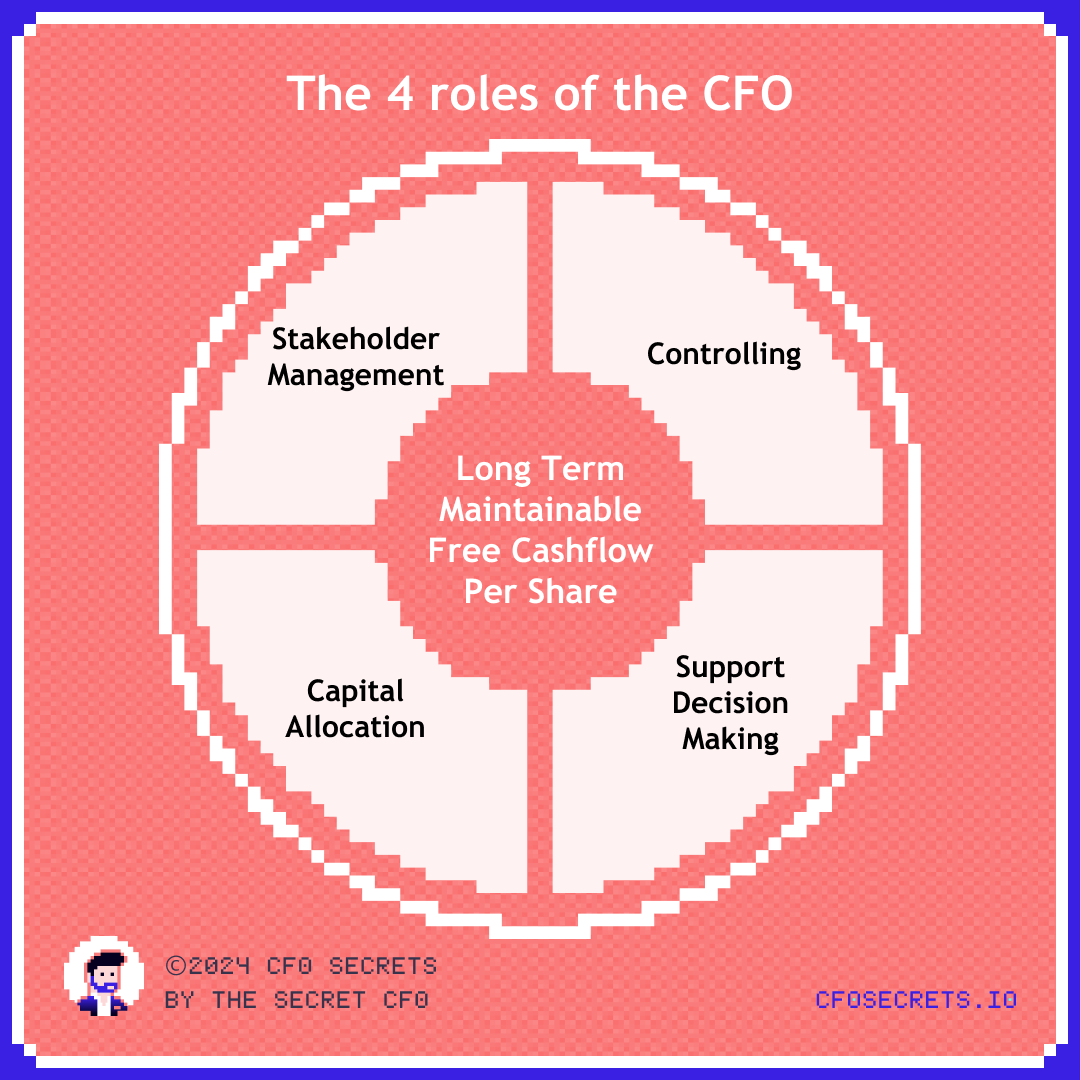

Capital allocation is such an interesting topic because it cuts across so many business processes. And so many different functions.

It goes directly to one of the four axiomatic duties of a CFO: how you use the money available to you.

Consequently, there is so much ground to cover on capital allocation. This could have been a 6-month-long series with all the threads and sub-threads we could pull.

So there will be subsequent series that each lean on the principles introduced here.

Just hit reply and drop me a line so I know where exactly you’d like to see me dive further into the topics covered in this series.

A lot more to come!

Ensuring adequate liquidity should be the CFO’s first priority for allocation of capital

Capital allocation cuts across many business processes and functions. Making good decisions requires discipline and rigor.

Have an investment committee to ensure capital allocation decisions are made in a consistent way.

NumberCruncher228 from Houston, TX asked:

How do I make the jump from just number crunching as a Controller to the CFO seat?

This is a big question, I actually wrote a piece on this topic last year.

In reality, your specific gaps will be unique to you. And what you need is a great role model or mentor a few years ahead of you (but not too many), who can be honest with you.

But typically, the most fundamental difference is that a controller is about adding value to the finance function, whereas a CFO is focused on adding value to the business.

You don’t need to wait until you have the CFO title to start practicing this skill (and it does need practice). You just need to start doing it. The best way to become a CFO, is to start behaving like one now. The challenge of course is in knowing what that looks like.

Start elevating yourself above the numbers and asking yourself what they tell you. What they mean for the business. How should it affect decision-making? Then ask yourself how you integrate those newfound insights into the business and drive action. Stakeholder management is the biggest leap for most new CFOs. So, start practicing.

You can also take the Secret CFO Scorecard, launched (in beta) back in March. It will help you find where your skill gaps are.

I hope this helps, and thanks for the question

If you would like to submit a question, please fill out this form.

And Finally

Next week is a special edition highlighting some of the best accounts/resources on social media.

If you enjoyed today’s content, don’t forget to check out this week’s sponsor Ledge.

Stay crispy,

The Secret CFO

Disclaimer: I am not your accountant, investment advisor, tax advisor, lawyer, CFO, director, or friend. Well, maybe I’m your friend, but I am not any of those other things. Everything I publish represents my opinions only, not advice. And certainly is not investment advice. Running the finances for a company is serious business, and you should take the proper advice you need.

What did you think of this week’s edition?