The accountant shortage is real

And it's leading to some very public and costly accounting errors. Automation can help finance teams reduce manual work, improve accuracy, and boost efficiency. Turn routine tasks into automated workflows — and do more with less — with accounting automation.

Feel the (cash) burn

We are at the halfway point of this series on interrogating financial statements, using Peloton as a case study.

In week 1 we set the scene.

Last week, we dug into their unit economics.

This week we are going to dive into the cash flow disclosures.

But before we start…

This is not investment advice. I may have investments in Peloton or other companies that are discussed in this post. And you might too if you own index funds! This post is for information and entertainment purposes only. Any assumptions made are my own.

Let’s dive in…

In the year ended June 2022, Peloton unexpectedly burned through $2.4bn of free cash flow. This presented an immediate threat to Peloton’s very existence.

When Barry McCarthy joined as CEO in early 2022 he made free cash flow his number one priority. Here are extracts from an investor presentation at the time:

And while he didn’t deliver free cash flow positive by FY’23, there has been progress. Unfortunately for him, progress does not equate to job security.

The free cash flow burn (per management) in FY’24 was down to $86m. Still a burn, but now only ~3% of sales vs the ~70% of 2022. By any measure, that is a move in the right direction.

And Peloton management is pretty bullish about the cash flow outlook. They are guiding investors to a free cash flow generation of $125m for FY’25.

But we know Peloton have been prone to some quirky accounting, so let’s find out how much progress they have really made.

And where do we start? With everyone’s favorite metric: Adjusted EBITDA.

Adjusted EBITDA

There are lots of hot takes around Adjusted EBITDA on social media. How it’s useless. How you shouldn’t adjust EBITDA. Or Charlie Munger describing it as ’bull sh*t earnings’.

Munger is right, it’s bullsh*t as an earnings measure. But no one with an ounce of financial literacy uses it as an earnings measure.

It’s not ‘adjusted EBITDA’ that’s the problem, it’s the adjustments themselves. And those adjustments need to be evaluated one by one.

So if you use EBITDA, properly adjusted, as the first input to a cash flow-based analysis, it is golden…

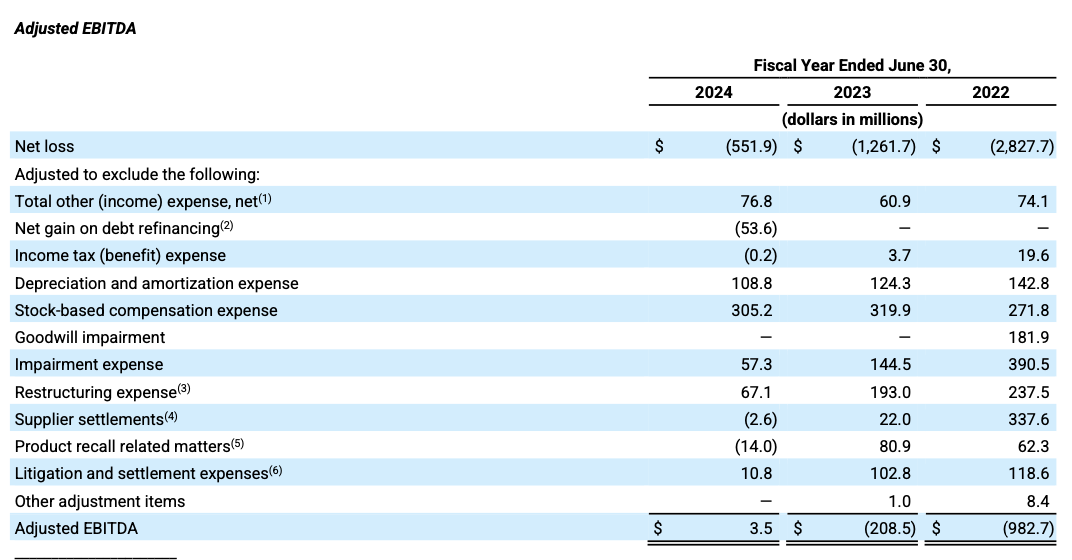

Ok, rant over. Let’s dive into the Peloton Adjusted EBITDA bridge:

Extract from Peloton FY’24 10-K

This bridge is key because Peloton's IR team has likely been touting their ‘Adjusted EBITDA positive’ status to Wall Street since its August release.

I like to go through a bridge like this by reviewing each adjustment line by line. The goal is to establish the extent to which I ‘agree’ it’s a reasonable normalization adjustment to EBITDA.

Then I would sort the adjustments into groups that can be thought about or analyzed in a similar way.

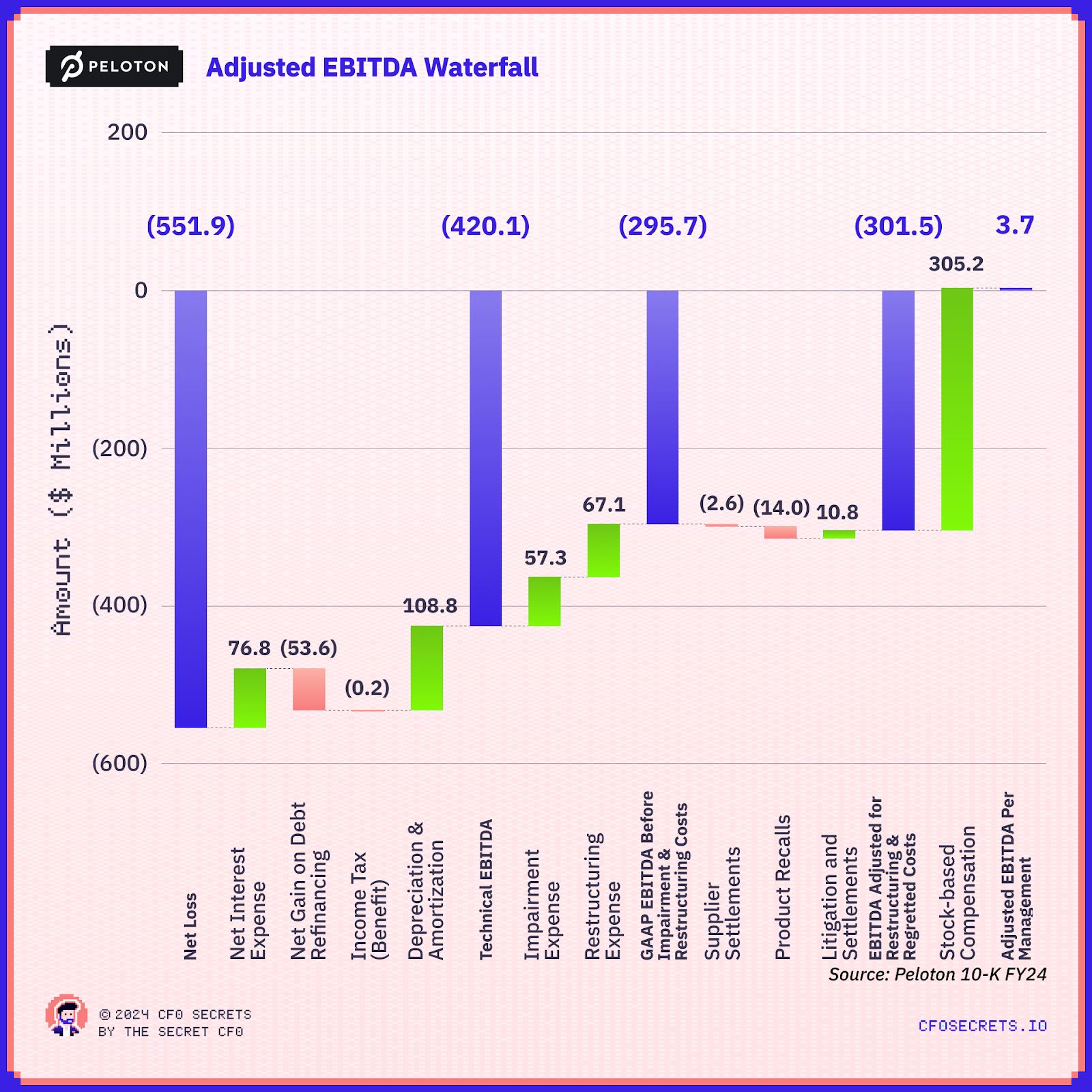

Doing this for the Peloton FY-24 Adjusted EBITDA bridge got me to the following:

You’ll see the bridge starts and ends in the same place as their 10-K disclosure (ignoring a $0.2m rounding error)

Let’s discuss the adjustments group by group:

1) Group 1 - The ‘ITDA’ Adjustments

The starting point is a GAAP ‘net loss’ of $551.9m. So the first step is to get to ‘technical EBITDA’, i.e. add back Interest, Tax, Depreciation, and Amortization. In this year Peloton also recognized a $53.6m gain on refinancing (they negotiated a haircut on maturing debt - more on that next week). We need to take exclude that gain here too.

Group 1 walks us from a GAAP net loss to a ‘Technical EBITDA’ loss of $420.1m

Nothing to see here.

2) Group 2 - Impairment and Restructuring Adjustments

Peloton has implemented two major restructuring plans over the last two years. The most recent in May of this year. This gave rise to a new restructuring reserve and true-ups to the reserve booked for the first restructuring plan from 2022. There was also a big impairment charge - presumably the effect of writing down the book value of the manufacturing and retail assets that are being closed.

I’m pretty comfortable with the treatment of these items as adjustments to EBITDA, as we will elect to handle them on a cash basis in a separate cashflow statement line.

We’ll get to the rest of the cashflow later.

After the Group 2 adjustment, we get to a ‘Technical EBITDA Before Restructuring and Impairment Expense’ loss of $295.7m.

3) Group 3 - Regretted Costs

This is where things start heating up. This group does not have any accounting justification for being an adjustment to EBITDA. But can it be justified on the basis it helps the readers interpret the financial statements?

These ‘regretted expenses’ are for product recall costs, supplier settlements, and litigation. Essentially, they represent the fallout of supply chain mismanagement through COVID. Compensation payments for canceling manufacturer orders for committed product. Litigation over music licenses. The recall of 2 million bikes after it was discovered the seats were faulty.

Management argues it should be adjusted because the costs are ‘non-recurring’. i.e. “This is money we wasted because we used to be less competent than we are now. But we’ll be better in the future… honest.”

It’s not totally baseless. It’s important to help investors draw out the lumpy one-offs affecting the accounts.

And you might ask, in the case of Peloton, why am I getting excited about an add-back that is only $5.8m net?

Well, two reasons.

First up, I’d argue that $5.8m is material. It’s the difference between negative and positive adjusted EBITDA in FY’24 using management’s definition.

Second, if these adjustments are material in FY’24, they were super-material in prior years. Peloton made equivalent adjustments to EBITDA of (brace yourself) $205.7m in FY23, $518.5m in FY22, and $135.8m in FY21.

So there can be no question that these adjustments are material.

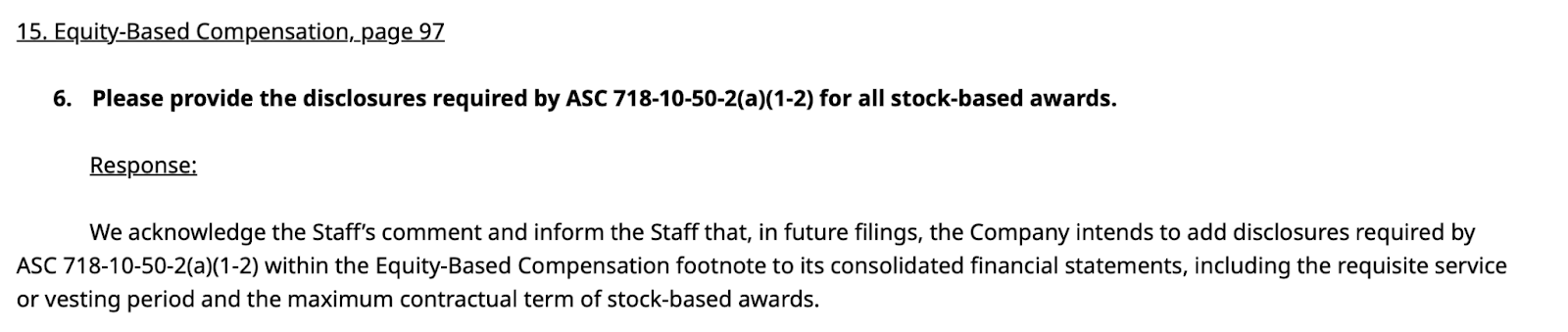

And you might be wondering what the SEC makes of this? Well, they felt strongly enough to write a letter to the Peloton board on March 20, 2024, seeking further information on these adjustments specifically in the FY’23 10-K filing.

The response by Peloton CFO Elizabeth Coddington can be found here. In it, you will see a line-by-line breakdown of the various litigation, supplier settlements, and product recalls.

In the nine-page letter, the word ‘nonrecurring’ is used 12 times. Lol. That’s a lot of recurrence for something that is nonrecurring…

If I were valuing this business for M&A purposes, I would absolutely be assuming some level of continuing run rate of costs for previous legal misdemeanors. It is hard to believe that they can go from such a high level of recall, litigation and settlements issues to zero in such a short space of time.

This takes us to the final adjustment…

4) Group 4 - Stock-Based Compensation

Presenting stock-based compensation as an EBITDA adjustment is not new. Many do it, especially in tech. But I hate it.

Stock-based compensation in Peloton was $301.5m in FY’24 and was even higher in the previous two years. 11% of sales. The idea that we can take a cost that represents 11% of sales and just pretend it’s not a cost is mind-blowing to me.

Warren Buffett said “If stock options aren’t a form of compensation, what are they? If compensation isn’t an expense, what is it? And if expenses shouldn’t go into the calculation of profits, where in the world should they go?”

If those stock options were not granted, then Peloton would have to pay their staff more cash comp to achieve the same result, which would, of course, be treated as an expense in any calculation of EBITDA.

For internal cashflow reporting purposes, I prefer to treat SBC as a cash expense. Funded by an ‘equity injection’ provided by the recipients of those stock awards. (I’ve discussed this at length in the posts on Maintainable Free Cash Flow).

It might not be technically correct, but it’s a healthier way for a business to think about it, and ensure department heads feel more accountable for the full cost of their teams and hiring decisions.

Now, it’s true that simply treating SBC as a cost based on its accounting isn’t quite correct, either. Especially in a case where many of those options are out of the money. Arguably, the better way would be to accept the add-back of SBC but look at cashflow on a per share basis - diluting the share count for the option awards.

My beef with Peloton management is that they are asking investors to treat SBC as a non-cash expense. But they also are pretty silent in their 10-K on the expected dilution effect of stock-based awards. This makes it very difficult for investors to get a meaningful read on forecast cash flow per share.

The SEC aren’t comfortable with this either. And picked this up in the same letter referenced earlier. Here is the response from CFO Elizabeth Coddington:

Extract from the Peloton response to the SEC letter

I’ve tried not to dunk on the Peloton team too hard in this series. I’ve tried to look forward more than backward and be balanced about the progress made.

But this adjustment coupled with the lack of disclosure is not easy to defend.

That meme would have been funnier if the escapee was riding a static bike, but never mind…

That gets us to the Adjusted EBITDA per management of $3.5m. Well by my math, their bridge has a $0.2m rounding error, but never mind. (You can take the man out of the audit, but you can’t take the audit out of the man 🤓)

So, with our interrogation of adjusted EBITDA complete, we now have a good foundation to build an analysis of Maintainable Free Cashflow (MFCF) for Peloton.

But first, let’s have a quick look at what’s going on in working capital.

Working Capital

The last couple of years have been a process of working through the inventory excesses of FY22 with the cash conversion cycle improving from +90 days to negative 12 days at Q1’25.

The Days Payable Outstanding has to be taken with a pinch of salt because Peloton's quarterly disclosures combine the stuff we want to include (accounts payable & GRNI) along with the stuff we do not want to include, like accrued litigation settlement costs.

Inventory

The real story is in inventory where stock levels have reduced from $1,105m to $330m over the last two years.

This has been good for cash flow, but not quite as good as it sounds. Some of the inventory reduction is a function of increasing reserves, so while inventories have reduced by $775m only $701m has converted to a cash inflow.

Inventory Reserves

Let’s have a look at inventory reserves:

This is extraordinary. The level of the inventory reserve is currently 35% of gross inventory. 35%!

There is an $80m reserve against ‘excess apparel and accessories’ inventory. Presumably a legacy of the 2020-2022 excesses. I don’t know exactly how many branded jerseys and bike mats Peloton sells, but I’ll bet it’s not huge in $. The lifetime gross margin on the equipment and apparel category must be a horrifically large negative number, once accounting for that reserve

But putting the misdemeanors of the past behind them… what will they do with that inventory? This is where things get interesting…

Here is an extract from the Q4’24 10-K inventory reserve disclosure:

Extract from FY’24 10-K

They have ~$175m of equipment, apparel, and returned equipment that the company ‘does not expect to sell’.

Here is the same disclosure from the recent Q1:

They’ve removed the ‘not expecting to sell’ note. Changes in disclosure like this do not happen by accident.

It would have been discussed with the audit committee, and maybe with the auditors too.

Sounds like something has changed. Watch this space I guess …

Anyway, let’s see what that all means for the total cashflow picture.

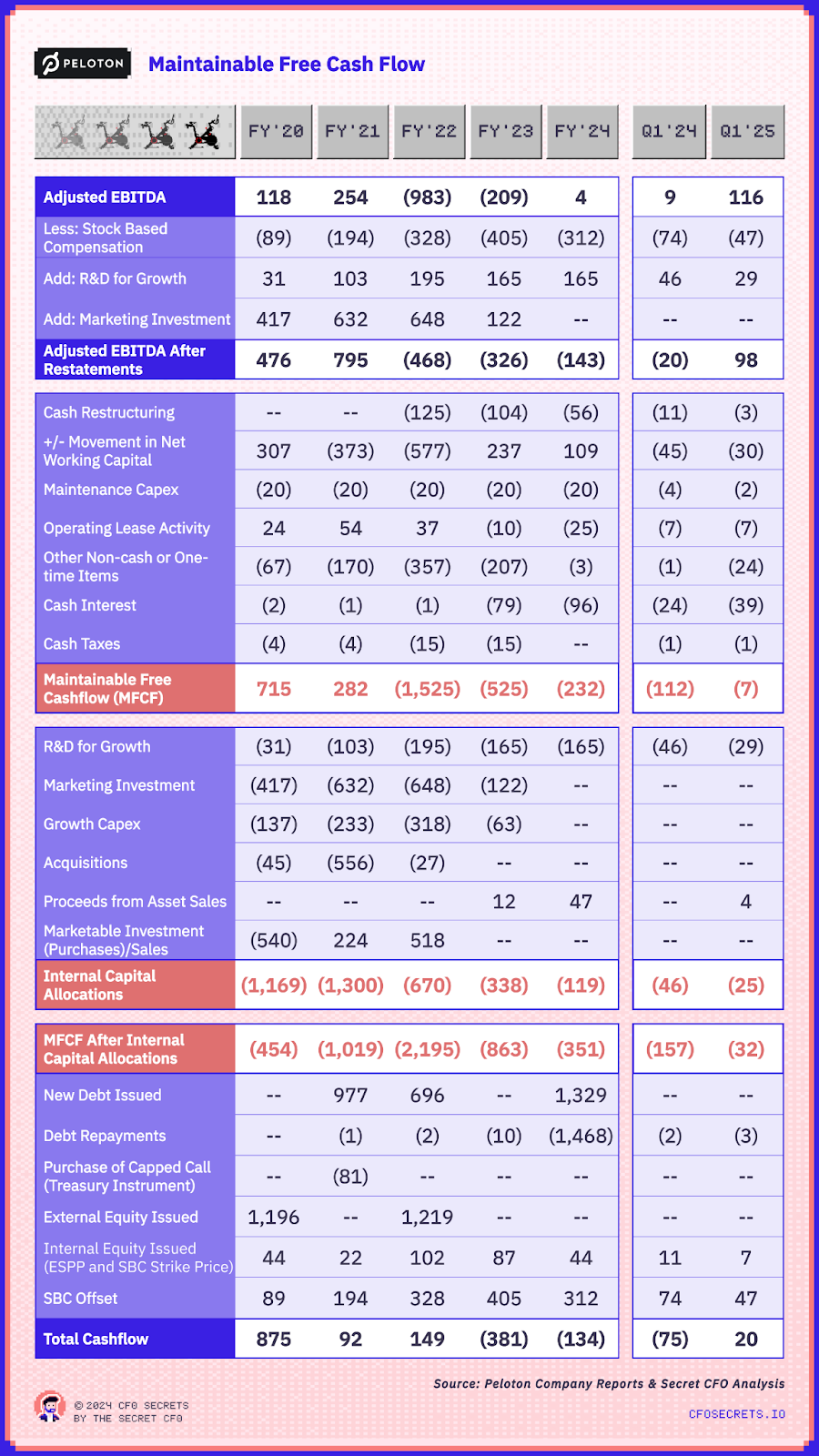

Maintainable Free Cash Flow (MFCF)

I’m not going to recap the principles of MFCF, or why I love it. That’s extensively documented here. If you want to follow the logic for calculating MFCF, I strongly suggest you read that piece before continuing.

Ready?

Ok, we’ll just dive in and see what it tells us about Peloton, and how it is managing cashflow.

Brief notes on preparation:

We’re using the management presentation of Adjusted EBITDA here. Just for ease of explanation. But our learnings from the earlier dive into the bridge will inform some of the treatments further down the cashflow.

Assumed a 70:30 split of R&D costs between growth and maintenance (based on benchmarking with competitors like iFit). The excess (as a % of sales) vs the market is assumed to be growth. As we said last week there is a wider question about whether R&D really is R&D in the case of Peloton, but we’ll put that to one side for the time being.

Maintenance marketing expenses were estimated as the total customer acquisition cost needed to replace churning subscribers. Any excess of sales and marketing expenses were assumed to be investments in growth.

We expect a low level of maintenance capex for this business (now it has exited from manufacturing and much of the retail estate). So we have assumed maintenance capex in line with the FY’24 capex spend throughout the period. (The rest being growth)

The table above tells the story of Peloton in the last five years in a nutshell.

It shows an interesting profile with MFCF being positive in FY20 & 21 ($715m & $282m respectively). A function of strong unit economics at that time.

But they over-allocated that generated cashflow into growth (capex, R&D, marketing), funded by the IPO and new convertible debt. It was a choice by management at the time. And had they executed well, the story might have been different. But they didn't…

They then choked on that growth, destroyed the unit economics and burned over $2bn of MFCF over the next three years.

That didn’t stop the spending. In fact, it gathered pace - with R&D, growth capex, and marketing investment all growing into FY’22.

But credit to them in recent times. They have both reduced the MFCF burn significantly and brought the internal re-investments under better control. From a 39% MFCF margin in FY’20, down to (42)% in FY’22, recovering to (9)% in FY24.

Over the last two years, they have benefited from the unwind of the extraordinary levels of inventory. It’s not easy to plug the holes in a culture that has lost control of spending.

They are also benefiting from the exits from the capex-heavy retail and manufacturing. Annual capex has fallen by 90% in the last two years.

And in the FY’25 Q1 recently reported, they are basically MFCF breakeven. That’s a start. They’ve stopped the burn.

The next step is to grow MFCF’s margin on sales, so they can self-fund their growth initiatives. I don’t think they’ll reach the dizzying heights of the 39% MFCF margin (on sales) they had in FY’20 again. But they can still build a cashflow-positive business off a much more modest level of MFCF margin.

To achieve that there is going to need to be a shift in unit economics, as we discussed last week. Plus balancing cost savings with the need for growth and gross margin improvements. Doing all three of those together is seriously hard.

And they need to get a move on, as they have ~$190m of convertible notes maturing in 2026.

Next week we will dive into that juicy recapitalization of the balance sheet, and understand how the business is funded today. I’m particularly interested in how much it will cost them in cashflow to grow, and how much funding they have available.

It looks lean to me…

See you next week when we dive into the Peloton capital structure.

Adjusted EBITDA is an important part of the toolkit. Understand how to use it.

Help investors and make your disclosures clear. Especially when you need their faith the most.

Don’t spend Maintainable Free Cash Flow you don’t have

And Finally

No Q&A or anecdote this week … the email size was too big! Don’t worry they’ll be back in two weeks time.

If you’re looking to sponsor CFO Secrets Newsletter fill out this form and we’ll be in touch.

Get your side hustle on. We're launching a platform to help match you with SMBs looking for exceptional fractional advisory talent. Apply now

Find amazing accounting talent in places like the Philippines and Latin America in partnership with OnlyExperts (20% off for CFO Secrets readers)

Thank you to today’s sponsor, Brex…

Find the right corporate card for your business in this guide from Brex.

Next week we’ll finish up with a deep dive into Peloton’s capital structure. If you follow the Peloton business, or read the 10-K, and have any thoughts, I’d love to hear them. You can send them straight to me by just hitting reply…

Stay crispy,

The Secret CFO

Was this email forwarded to you? You can subscribe by clicking the button below:

Disclaimer: I am not your accountant, investment advisor, tax advisor, lawyer, CFO, director, or friend. Well, maybe I’m your friend, but I am not any of those other things. Everything I publish represents my opinions only, not advice. And certainly is not investment advice. Running the finances for a company is serious business, and you should take the proper advice you need.

What did you think of this week’s edition?