AI ROI secrets: What top CFOs know

More than 4 in 5 finance leaders report positive ROI on their AI investments, and you can too with the CFO’s guide to building an AI strategy. Get their insider playbook for what’s working, what to avoid, and how to accelerate the automation benefits in your own organization.

Capital punishment

This is the final week of a 4-week series sharing how a CFO interrogates financial statements. As a reminder, we are using Peloton as a case study.

In this final week, we will take a look at the capital structure, and the recent refinancing.

But before we do …

This is not investment advice. I may have investments in Peloton or other companies that are discussed in this post. And you might too if you own index funds! This post is for information and entertainment purposes only. Any assumptions made are my own.

The Peloton Refinance

Let’s leap straight to the big story in the balance sheet:

Extract from Peloton FY’24 10-K

A refinancing in May-24.

The timing here is interesting. You’d think they’d wait to see whether expected rate cuts in 2024 help them or not. So let’s dive in deeper to understand the thinking.

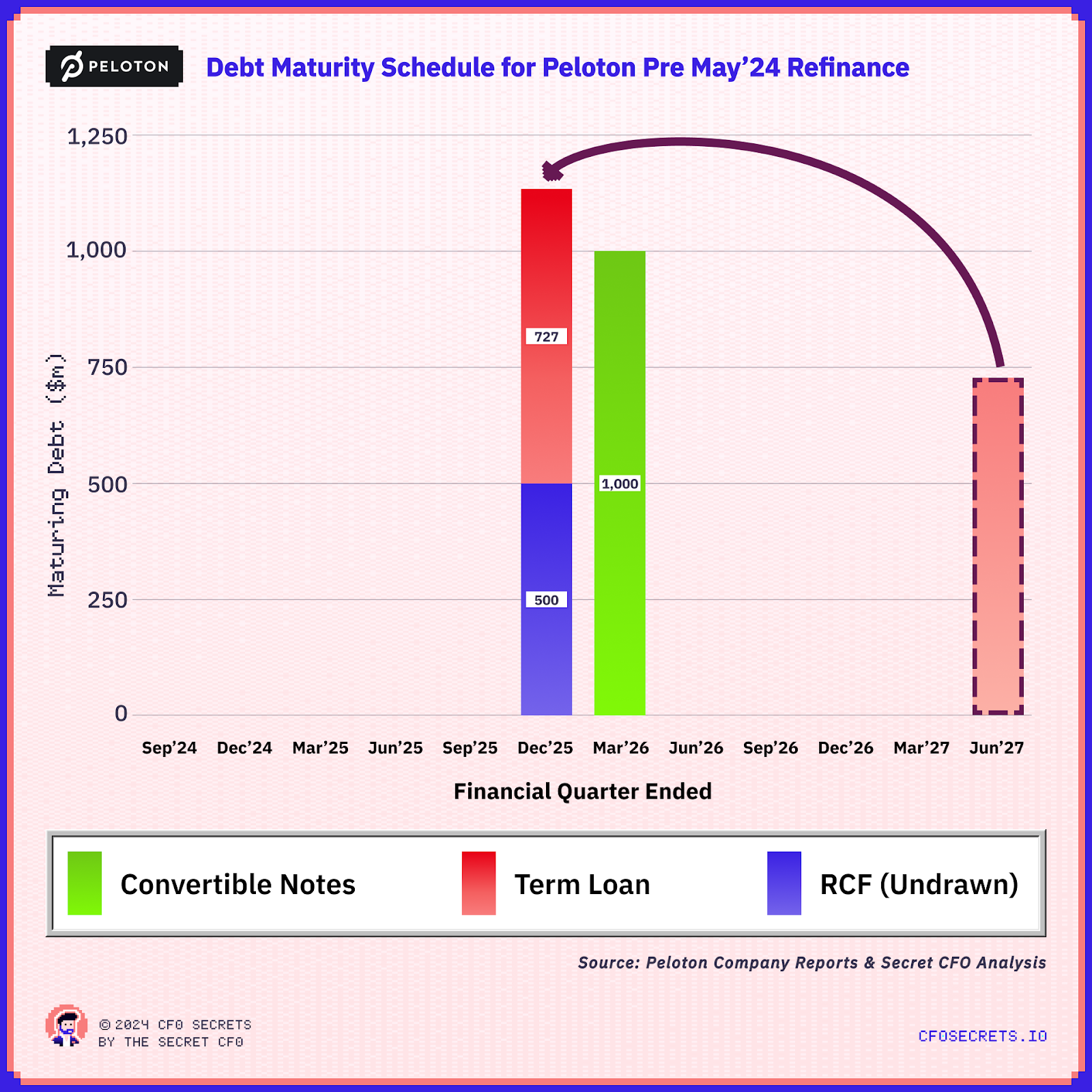

The ‘Before’ Capital Structure

The best way to understand a refinance is to start with the ‘before’ picture, to build a snapshot of the ‘as-is’ capital structure and the issues a refinance would (hopefully) solve:

There is a $1.7bn lump of debt, all due to mature over the next couple of years. And the convertible notes are far out of the money. How far? The stock price in May was ~70x lower than the strike price!

So Peloton won’t want to settle those notes in stock as it would p*ss off shareholders. And they don’t have the cash to pay the notes down, so a full debt refinance becomes the logical option.

But why now? Why did they refi in May-24?

Credit markets are warmer than they were 18 months ago, but with rates expected to fall, you’d think Peloton would keep their options open for a while longer. Especially with their cashflow performance (and therefore credit worthiness) improving quarter after quarter.

Springing Maturities

The answer is in the term loan. There is a clause in their $1bn term loan that if there are more than $200m convertible notes still outstanding at Nov-25, then the maturity of the term loan ‘springs’ forward, becoming immediately due for redemption (in Nov-25.)

This is called springing maturity.

It’s a clever mechanism the term loan lenders use to say ‘Hey, if you end up in a sticky patch on your convertible notes, we want to be able to force a refinance sooner, so we don’t get stranded and stuck behind the convertibles.’

This point brings much more urgency to a refi. Peloton does not have the cash to pay down 80% of the convertible notes before November-25. And converting to equity would have created a riot amongst shareholders given the stock price was around $3.50 vs. the strike price of $239.32! So, that springing maturity on the term loan is as good as sprung…

Going Concern Disclosures

And by the time the 10-K for FY’24 would be signed in August ’24 the term loan maturity of $737m would only be 15 months away.

This level of maturing debt would have created a going concern disclosure challenge for the FY’24 10-K. Even if they could squeeze through the ‘24 10-K clean, for sure they would need to disclose by Q1 of FY’25 (October-24).

You can imagine the headlines if Peloton had to wear ugly disclosures in their audit report speculating on the company’s ability to refinance. So my guess is that this is what drove the timing of the refi, even if it wasn’t ideal considering the improving business performance and lower interest rates expected in the near future.

The Peloton board would want to get in front of this problem. And I’ll bet refinancing was the last thing on Barry McCarthy’s (CEO until May-24 and previous CFO at Spotify and Netflix) pre-retirement to-do list.

Refinancing

So, now we have a picture of the debt they need to solve for. But how did they do it?

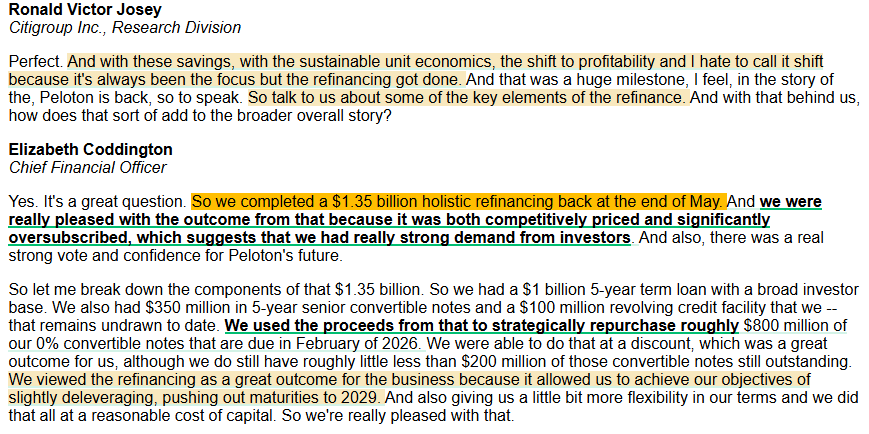

Well, let’s hear CFO Elizabeth Coddington describe the outcome in her own words:

From a recent earnings call transcript

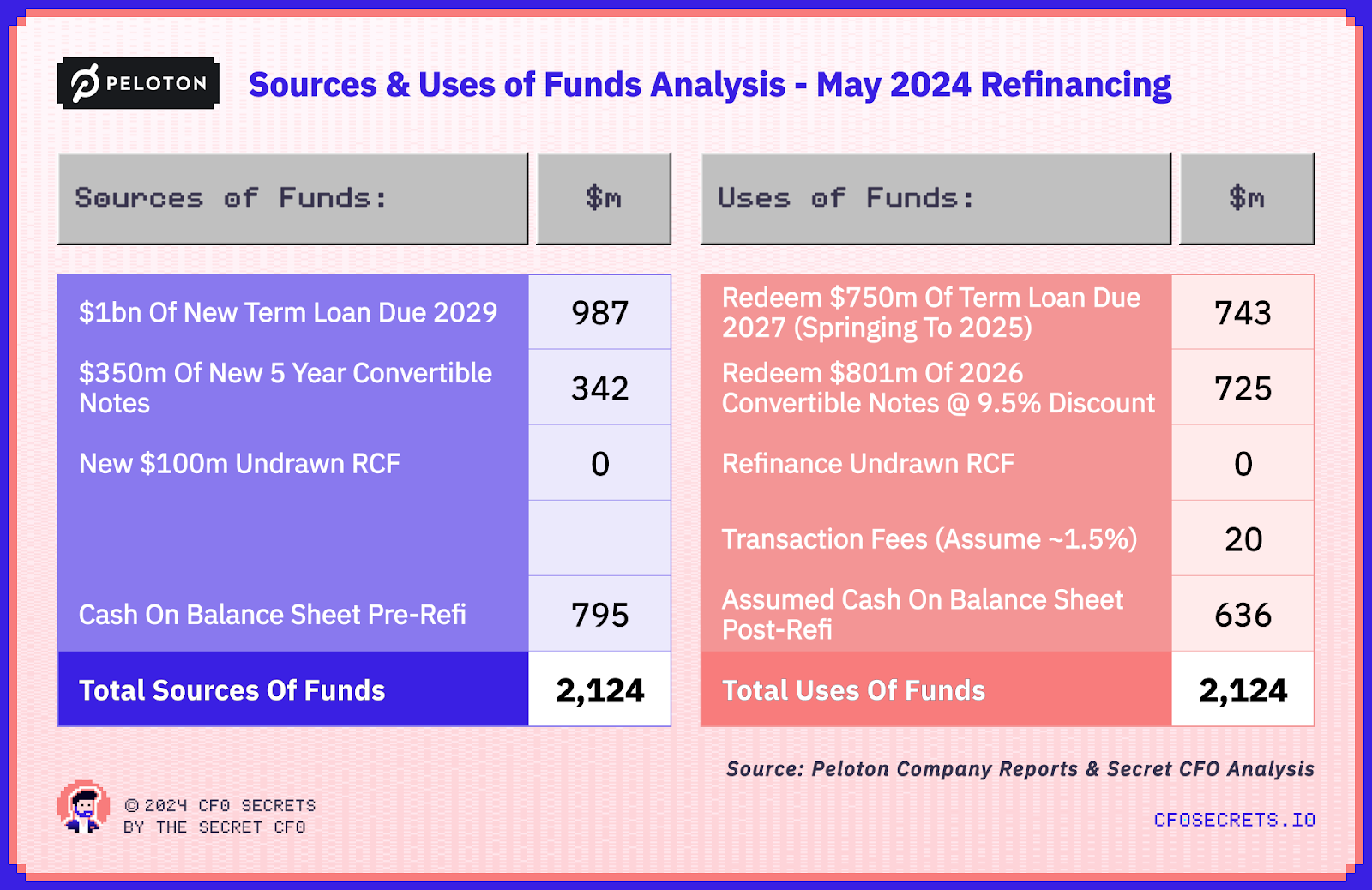

So what did this refinance look like?

I like using a ‘sources and uses of funds’ analysis to understand what is going on in a refinancing. It shows what money is being raised (on the left), and how it is being used (on the right):

Note: this includes an educated guess on transaction fees. Goldman Sachs and J.P. Morgan ran this transaction. You can bet they were working on 1-2% of the total raise. And then there are lawyers fees, etc.

Peloton was able to successfully refinance the revolving credit facility (overdraft), term loan, and $801m of the total $1bn convertible notes. Leaving $199m of the ‘26 convertible notes outstanding.

They did this by issuing new 5-year convertible notes, and a $1bn term loan (as well as using some cash on the balance sheet).

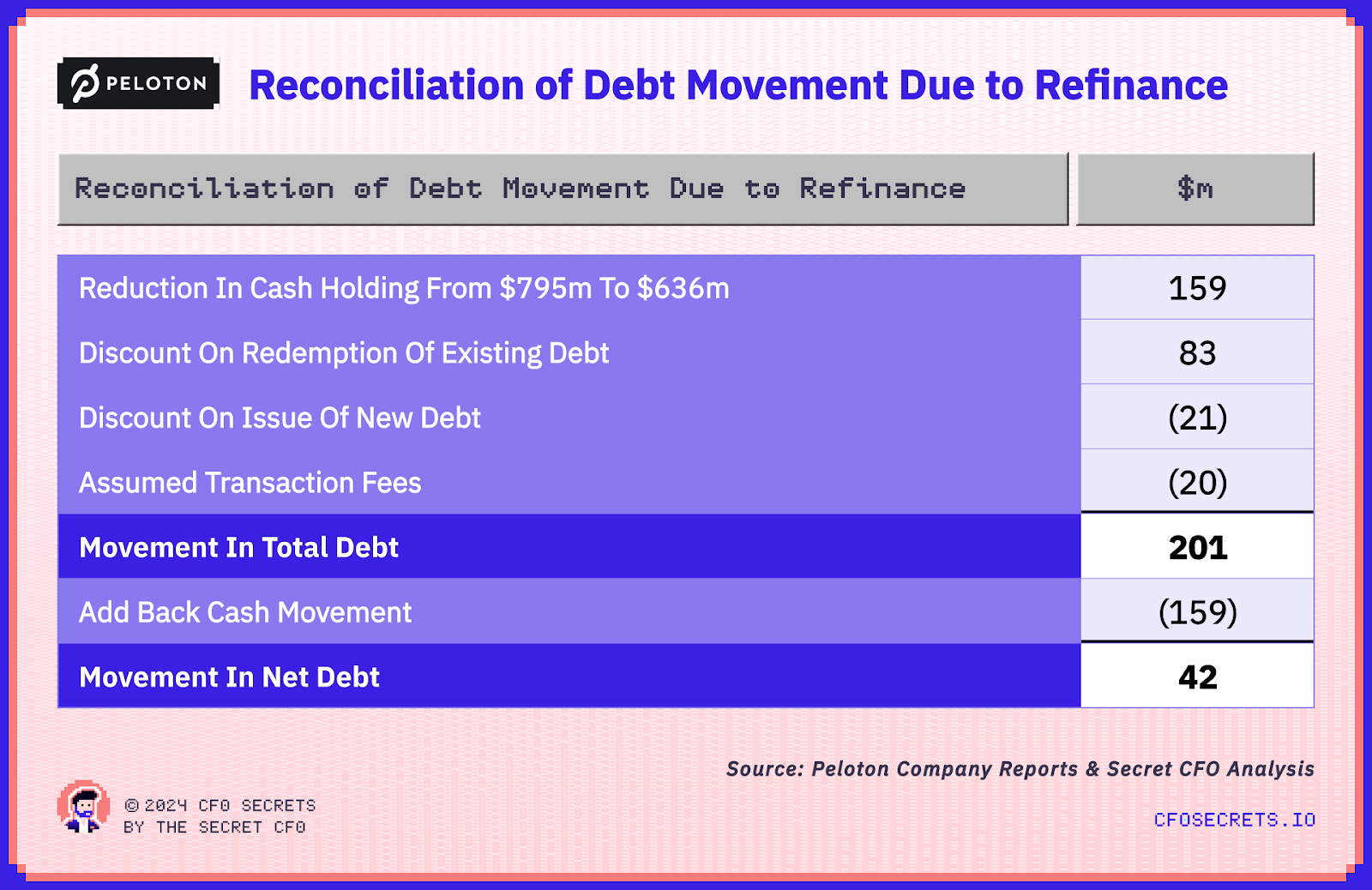

The net effect was a reduction in total debt burden of $201m and a reduction in net debt of $42m:

Let’s have a deeper look at those ‘discounts’ on the debt.

A discount on redeeming debt is a good thing for the business. In this case, Peloton owed 2026 convertible note holders $801m but was able to agree with those holders that they would repurchase that debt for $725m ( a 9.5% discount).

Discounts on new debt issuances work the other way. They are a cost to the business. Think of it like an arrangement fee. Banks call it an ‘On-Issue Discount’ or OID.

So if you borrow $100 with an OID of 2% it means you receive $98, but still have to pay back $100.

This is a friendly reminder that lenders will f*ck you any way they can. Especially if you are at the wrong end of the credit spectrum. The OID is just another tool in their armory.

It looks like the new convertible notes were issued with a 2% OID and the term loan with a 1.25% OID. Nothing out of the ordinary.

Wargaming the convertible debt

This would have been an interesting negotiation with plenty of variables. A game of 3D chess.

Let’s wargame how this played out a little…

Put yourself in the shoes of the 2026 convertible noteholders for a moment (immediately before the refi).

In 2021, you lent $1bn to Peloton at a zero percent interest rate, but with an option to convert into shares at a strike price of $239.32 at the end.

What has happened in the three years since:

The business has tanked, and burned a couple of billion of cash, making your credit position more precarious. There was at one point a real risk you’d lose your entire investment.

The business has started to recover, but the stock price (in May) was still only $3.50 vs. the strike price on your convertible note which is 70x higher. No, not 70%...70x. You are so far out of the money you forgot what the money looks like.

Interest rates have shot back up, and you could have earned a 5% yield for sitting in treasury bonds the whole time.

You, my bag-holding buddy, are the proud owner of one of the sh*ttiest pieces of paper in the history of convertible debt.

So you want out. You want your money back, and you are prepared to take a bit of a haircut to end this nightmare.

Now let’s flip to Peloton’s side. You’ve got capital to raise. A lot of capital. Too much for the equity markets (especially with the stock price where it is), and likely too much for the term debt markets. That means you need to issue some level of new convertible notes.

But the market knows how that went last time around. So finding new investors will be hard. You’ve got to go back to your old buddies… the 2026 convertible noteholders.

Peloton and their noteholders…

So the pitch goes something like this:

“Hey, we can repurchase 80% of the notes you hold. But we need a 9.5% discount. But, for this to work, you need to agree to roll roughly half of the redeemed notes into a new 2029 convertible note. But this one will be sexy. We’ll pay interest, and the strike price will be rebased to something sensible. The rest you’ll get in cash. Real money!”

This is known in the credit trade as ‘self-help’.

So for someone holding $10m of 2026 convertible notes, they will have something like this post-finance:

$2m of 2026 notes

$3.5m of new 2029 convertible notes (with a coupon and ‘in the money’ options)

$3.6m of cash (to reinvest somewhere else)

Total of $9.1m. The other $0.9m has given to Peloton as a redemption discount, to oil the wheels of the deal.

And remember… alongside this, Peloton will also need to find the banks to raise the term loan and RCF.

I’ve been through processes like this before.

It’s fun as hell, there are so many variables and different stakeholders with different interests. You have to work out the steps that get the best results for the company. It’s all about having a carrot and a stick with each stakeholder. And having the very best investment bankers alongside you to make it happen.

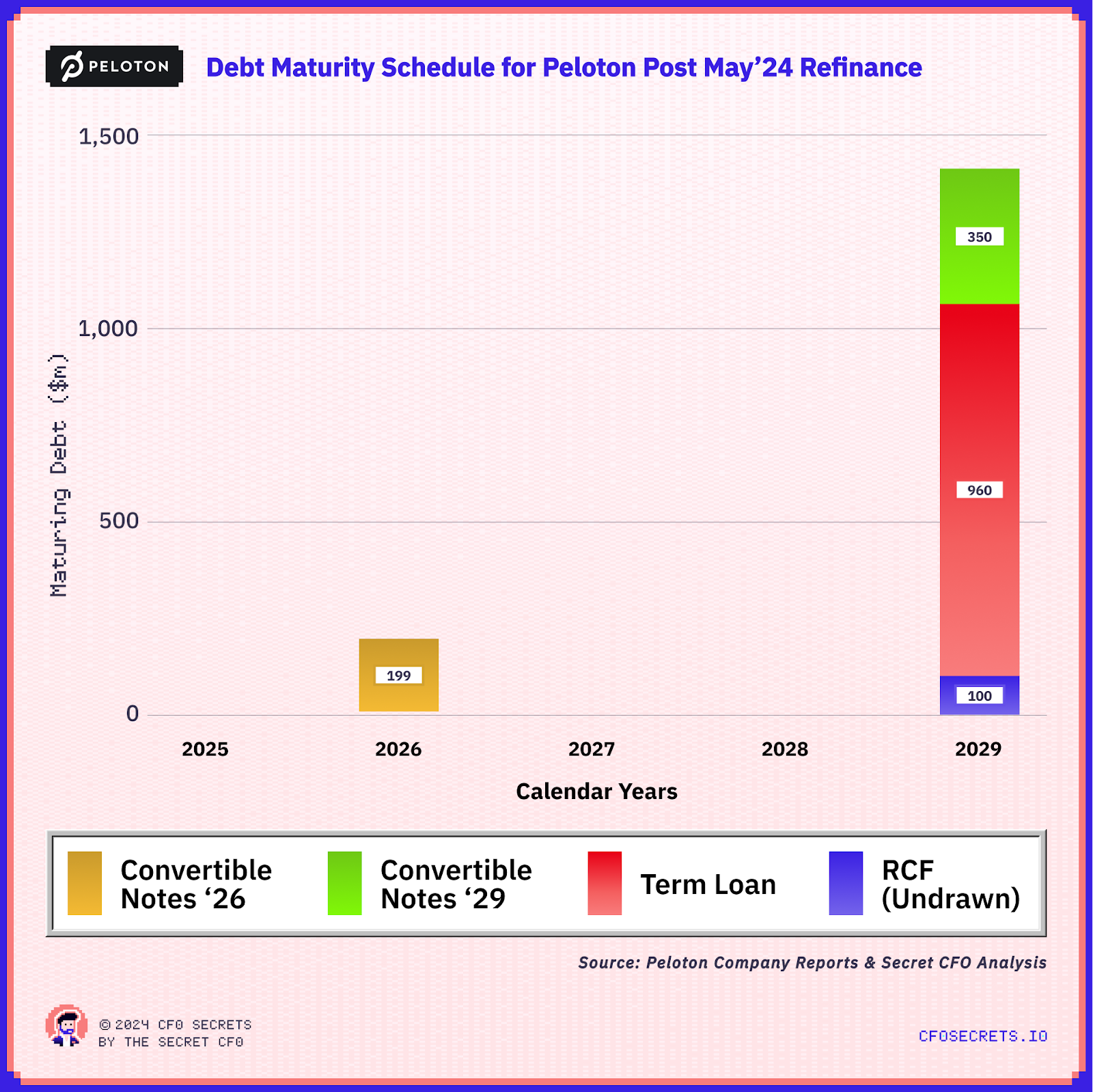

The New Capital Structure

Let’s see what the capital structure looks like immediately after the refinance:

To tease those convertible holders into the new notes, they offered them a 5.5% coupon plus a conversion at a strike price of $4.58. Roll forward six months, the stock closed yesterday at $9.54, so this is off to a roaring start. Looks like that faith could be justified.

But the thing that caught my eye most in this structure is the change in terms in the RCF interest (margin over SOFR) has moved from 2.25% to 5%.

To quote Borat: “Wa-wa-wee-wa.” That is huge given it’s secured and (I presume) top of the security stack.

But more surprising are the covenants. A $250m minimum liquidity covenant (2.5x the size of the RCF itself), and tested WEEKLY. I’ve never seen that before.

It means that at the end of every week, Peloton has to ensure they have $250m of liquidity available (including the $100m of undrawn RCF).

That is as good as a restriction on $250m of cash (or $150m with an unusable RCF).

That is not a reasonable request by a lender. It’s the sort of covenant you sign up to if you have no choice.

So when you look at the interest rate change, and this covenant, it looks like the lenders had them over a barrel.

The Banking Syndicate

And who are those lenders? The same investment banks that ran the bigger refinance for them; Goldman Sachs and J.P. Morgan.

So not only are JPM and GS enjoying a juicy fat fee on the whole $1.45bn debt raise, they have also nailed Peloton to the floor on the terms of the RCF as their lender.

JPM and GS tend only to participate in an RCF as a gesture to win the mandate for a bigger capital raise. It’s not core business for them, kind of like a loss leader.

But what is surprising here, is that Peloton weren’t able to negotiate better terms, given the 8 figure fee pot that was up for grabs

Citibank and Barclays had been part of the old RCF syndicate (alongside JPM and GS). It’s interesting that they weren’t part of this one.

The 6.0% margin on the term loan is notable too. These lenders aren’t disclosed, but with the size of that margin, I’d assume it came from a non-conventional source. Likely private credit.

Mission Accomplished

The terms are pretty ugly in a few places, but let’s be real…

The objective of this refinance was not to get to a stellar cost of capital. The business had a wall of maturing debt and several years of volatile performance. The turnaround is progressing but is far from complete (as we’ve seen in the rest of this series).

Peloton was refinancing from a place of weakness. One that McCarthy and Coddington inherited.

The goal of this refi was to ‘kick the can down the road.’ To extend maturity and give the business more runway to execute its turnaround plan. And do so at the lowest cost possible.

Mission accomplished:

Note: The maturity schedule is now measured in years rather than quarters. The term loan also has $10m per year of amortization (but too small for the chart!)

In my humble opinion, Elizabeth and the Peloton team have done a good job of buying the business the time needed to complete the turnaround. Sure, it’s costly, but it was always going to be costly.

Funding to Grow

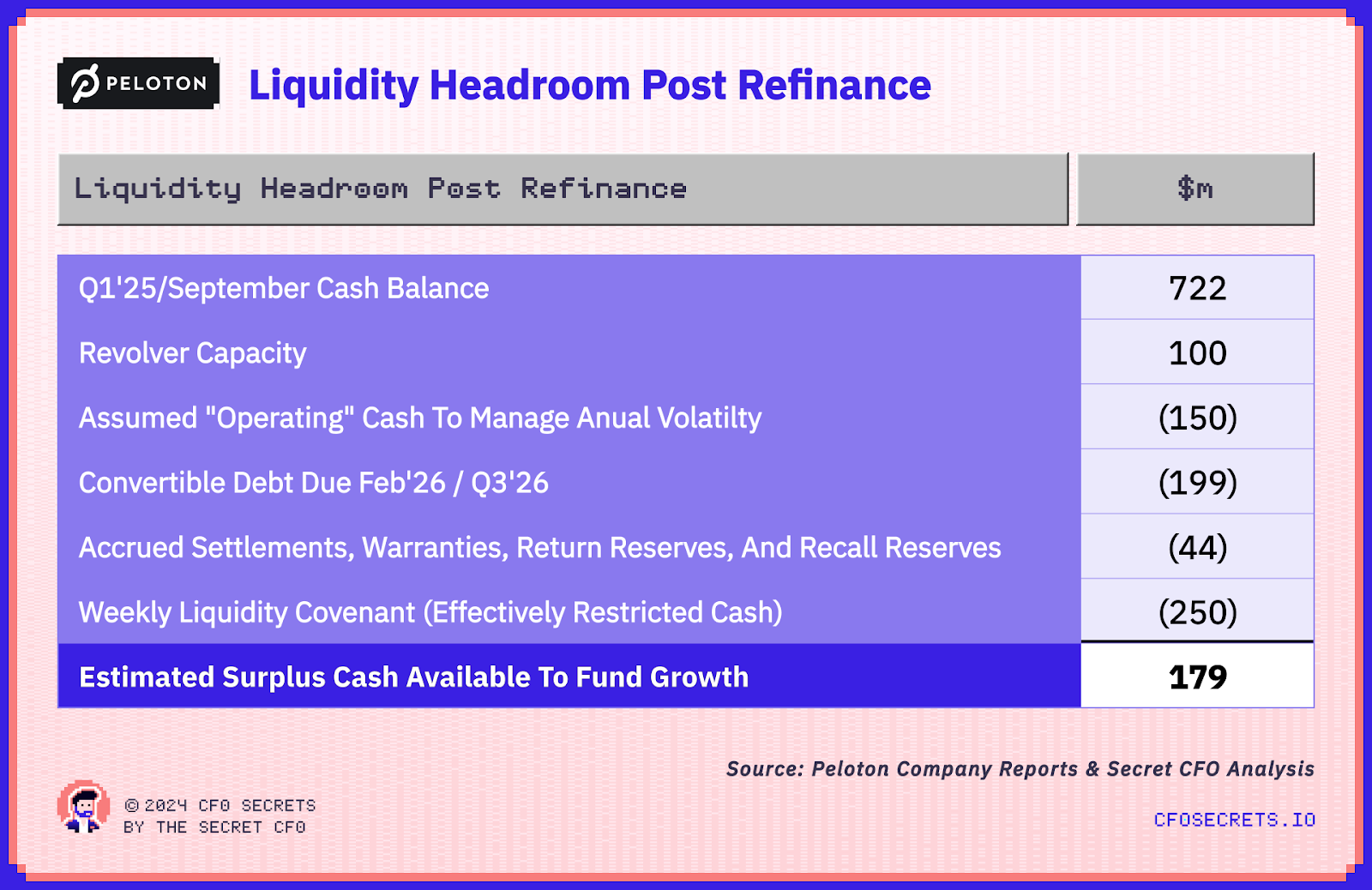

The last question I have on the new capital structure is, how much firepower does it leave them with to grow?

When you refinance you get to reset the cash level you hold in light of your most recent forecasts. I think this is interesting to look at in the context of Peloton, as it informs how much fuel they have for growth

By my back-of-envelope calculation, they have somewhere around $150m-$200m as a pot to grow…

Working back from the Q1’25 cash balance:

This assumes Peloton is currently cash breakeven and will be for the immediate future (consistent with what we discovered last week). So if they can start to generate free cashflow, this will increase the size of their pot.

New CEO Peter Stern will be in soon. And he’ll be charged with finding a way to grow the business.

You can imagine him fired up for day 1. Peloton undershirt under his suit and tie.

“Hey Elizabeth, how much do I have to spend to grow this thing?”

Elizabeth: “We’ve got about $150m-$200m we can allocate to growth investments above our current run rate.”

Peter: “Great… what does that get me?”

Elizabeth: “Well, at an average net acquisition cost per new subscriber of $926. That’d be somewhere between 160k and 220k new subscribers. It will buy more if that investment is stretched over time.”

Peter: “OK… that’s a start.”

Elizabeth: “Or it would be enough to fund about 20% of our total litigation, product recalls, and supplier settlements over the last five years.”

Peter: “Oh…”

Here’s hoping those sins of the past stay in the past.

Joking aside, if I were CFO of Peloton, I would not want this business to be awasah with capital. Last time that happened, bad things happened. Very bad.

I would want just enough to execute on our plans plus a safety margin, and that’s where they have ended up.

Wrapping Up

Peloton is certainly not out of the woods. There remain fundamental issues with the unit economics of the business.

But with a new CEO, the debt maturities addressed, and a decent bull run on the stock, the investor noise around the business is suddenly a little quieter. That gives Peter and the team some well-earned space and time to get to work.

I’ll be rooting for them.

And that is the end of our series on interrogating financial statements like a CFO.

This series was a bit of an experiment. But if you enjoyed it (or didn’t), let me know! It will help me shape future content decisions. Just hit reply and thanks in advance!

Finally, I’d like to say thank you to Daniel Moudy who supported the analysis for this series. His deep dive into the Peloton financials has been outstanding. It’s rare to find someone with the deep technical skills of a CPA, real natural commerciality, and the forensic know-how you’d find in a hedge fund. He’s also been a pleasure to work with.

Daniel happens to be looking for a new role. Check out his LinkedIn profile. If you’d like an intro either reach out to Daniel via LinkedIn, or reply to this and I will introduce you.

Complex refinancings are like 3D chess. Get the right investment bank in your corner.

Know what variable you are optimizing for in a refinance. Cost of capital, flexibility, downside protection, tenor, etc?

Timing is everything in a capital raise… EVERYTHING

And Finally

Q&A and anecdotes will be back next week.

If you’re looking to sponsor CFO Secrets Newsletter fill out this form and we’ll be in touch.

Get your side hustle on. We're launching a platform to help match you with SMBs looking for exceptional fractional advisory talent. Apply now

Find amazing accounting talent in places like the Philippines and Latin America in partnership with OnlyExperts (20% off for CFO Secrets readers)

Thank you to today’s sponsor, Brex…

Pay fewer FX markups and simplify international tax compliance with the global CFO playbook from Brex.

Next week we’ve got a special edition on CFO Mindset.

Stay crispy,

The Secret CFO

Was this email forwarded to you? You can subscribe by clicking the button below:

Disclaimer: I am not your accountant, investment advisor, tax advisor, lawyer, CFO, director, or friend. Well, maybe I’m your friend, but I am not any of those other things. Everything I publish represents my opinions only, not advice. And certainly is not investment advice. Running the finances for a company is serious business, and you should take the proper advice you need.

What did you think of this week’s edition?